The post “Calculating Supply Chain Climate Exposure” first appeared on Alpha Architect Blog.

Supply Chain Climate Exposure

- Kate Liu, Greg Hall, Lukasz Pomorski and Laura Serben

- AQR Quarterly Report, 2Q 2022

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category

What are the Research Questions?

Recently the SEC proposed regulations for US-listed firms to publish Scope 1,2 and 3 greenhouse gas (GHG) emissions. Disclosure of Scope 1 and 2 are mandatory for all firms, but the disclosure of Scope 3 is required only if material and/or a climate target has been set for Scope 3 emissions. Scope 1 are direct GHG emissions from owned sources; Scope2 are indirect GHG emissions from purchased and used heat, cooling, electricity, steam, etc. Scope 3 are all remaining indirect GHG emissions that occur up and down the firm’s value chain that are material. Basically, Scope 3 is intended to account for emissions tied to a firm’s products and services. An example of Scope 3 would be GHG’s produced in lithium mines supplying Tesla. Although the recent SEC regs may ultimately be seen as a watershed event in the ESG timeline, the SEC failed to define Scope 3 in terms of materiality. In answer to this opportunity, the authors of this paper develop and validate an approach to improve the measurement of supply chain climate exposure.

- How is the measure constructed?

- What is the intuition behind the supply chain metric?

What are the Academic Insights?

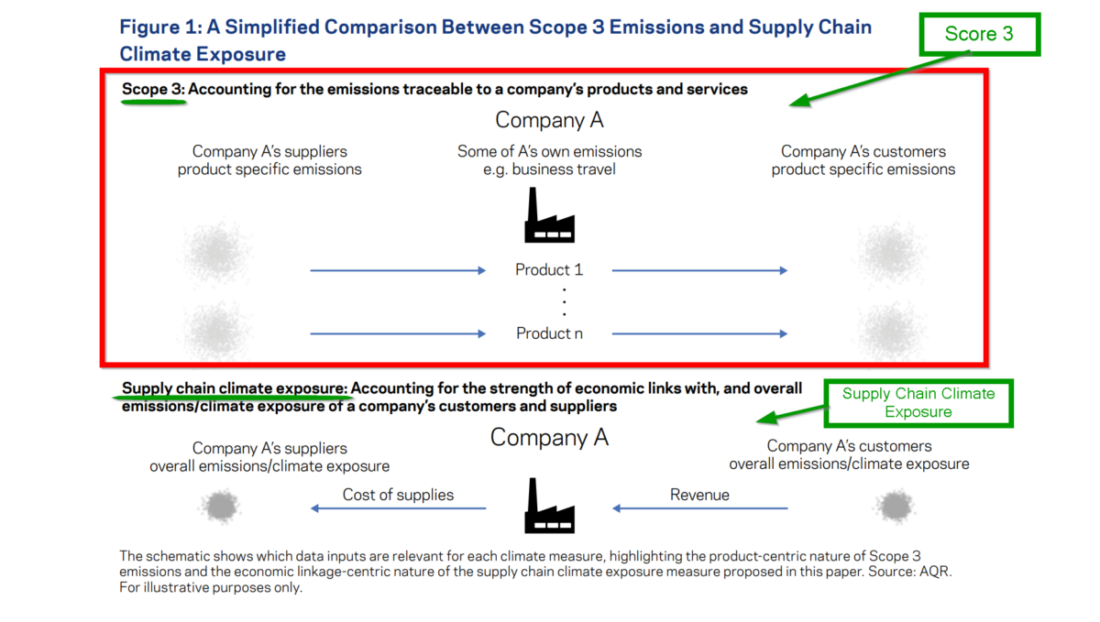

- The measure is a simple revenue-weighted climate exposure (C) where C is the customer sum of Scope 1 and Scope 2 associated with a specific firm. If a supplier, then the measure would be the cost-weighted value of C for the supplier. Note that the proposed metric is obviously related but distinct from Scope 3 emissions. Figure 1 depicts the key data items to calculate Scope 3 GHG and the “supply chain climate exposure” measure, for comparison.

- The authors argue their intuition for this research with a short but convincing example:“

Consider the company, FleetCor Technologies (FLT).2 FLT is a payments services company, and as such resides in a sector (IT) and industry (IT Services) that are rarely associated with climate risks. In fact, based on the standard climate data such as carbon intensity or carbon footprint, FLT seems green even compared to its sector or industry peers. For example, its scope 1 and 2 emissions are lower than the industry and sector median, and its scope 3 emissions are actually in the greenest quartile within its industry. Based on this information alone we may conclude that the company has little climate risk exposure. However, our assessment may change once we look at FLT’s customers. For example, in the company’s 2012 10Ks, FleetCor reported that their “top three strategic relationships with major oil companies represented in the aggregate approximately 21%, 22% and 18% of [their] consolidated revenue for the years ended December 31, 2011, 2010 and 2009, respectively.”

The large exposure to oil majors may indicate that the company might be indirectly, but possibly materially, exposed to disruptions, and potential loss of revenue, caused by climate-related risks.”

Why Does it Matter?

The idea presented here is clever in terms of its’ intuition and simplicity. Capturing the full supply/customer climate exposure for a specific firm by combining the Scope 1 and 2 values of suppliers and customers and then weighting by their impact (either revenue or costs) is smart and likely captures other risks not covered by the proposed Scope 3 metric.

I recommend reading the article in order to capture the full implications of the proposed measure. Obviously, there are implications for investors in evaluating the risk profiles of portfolios in terms of ESG as well as the firms, suppliers, and customers. For the investor, a consistent and quality measure permits an effective evaluation of climate risk from a fundamental point of view. For firms, the advantage lies in the ability to simply and clearly communicate reporting requirements and expectations.

In an upcoming summary, I will cover the extensive validation of the supply chain metric conducted and offer a better perspective on the implications and widespread applications across capital markets. Stay tuned for Part 2.

The Most Important Chart from the Paper

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

To manage climate risks, investors need reliable climate exposure metrics. This need is particularly acute for climate risks along the supply chain, where such risks are recognized as important, but difficult to measure. We propose an intuitive metric that quantifies the exposure a company has to customers, or suppliers, who may in turn be exposed to climate risks. We show that such risks are not captured by traditional climate data. For example, a company may seem green on a standalone basis, but may still have meaningful, and potentially material, climate risk exposure if it has customers, or suppliers, whose activities could be impaired by transition or physical climate risks. Our metric is related to scope 3 emissions and may help capture economic activities such as emissions offshoring. However, while scope 3 focuses on products sold to customers and supplies sourced from suppliers, our metric captures the strength of economic linkages and the overall climate exposure of a firm’s customers and suppliers. Importantly, the data necessary to compute our measure is broadly accessible and is arguably of a higher quality than the currently available scope 3 data. As such, our metric’s intuitive definition and transparency may be particularly appealing for investors.

Disclosure: Alpha Architect

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Alpha Architect and is being posted with its permission. The views expressed in this material are solely those of the author and/or Alpha Architect and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.