![[Gamma] Scalping Please](https://ibkrcampus.com/wp-content/smush-webp/2024/04/tir-featured-8-700x394.jpg.webp "[Gamma] Scalping Please")

The article “Comparing Past and Present Inflation Rates Can Be Tricky” first appeared on Alpha Architect Blog.

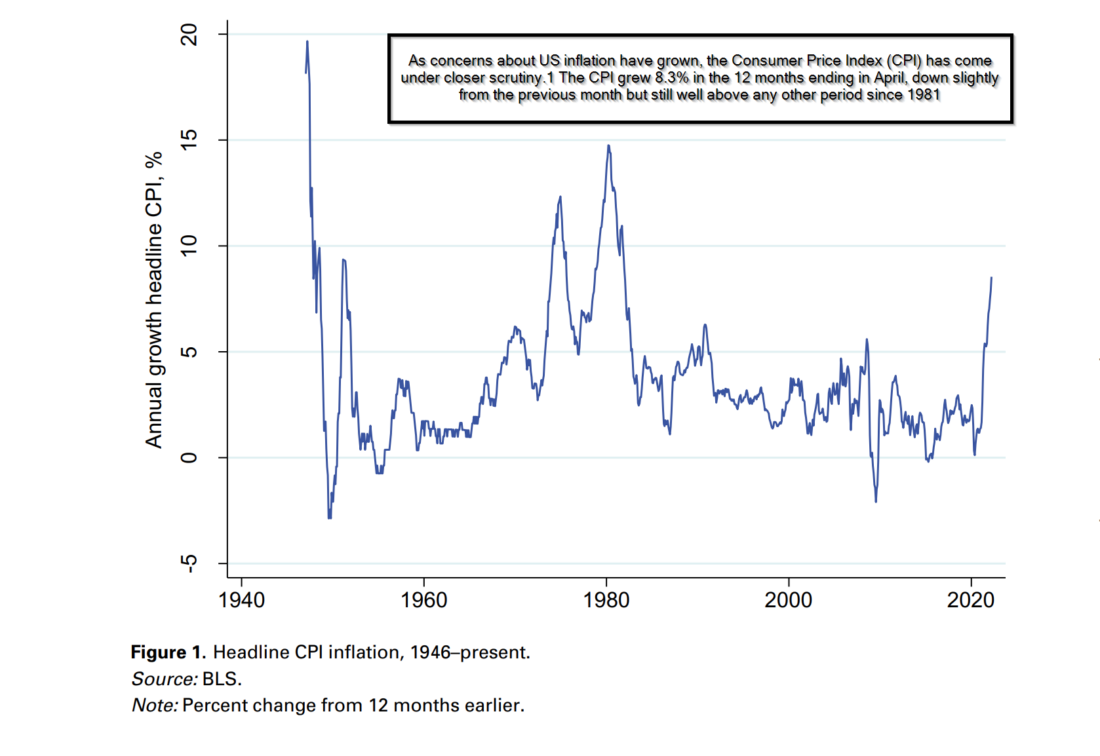

This article aims to build better estimates of CPI headline and core inflation values, making inflation comparisons over time more reliable. The run-up in inflation we are currently experiencing is difficult to contextualize because it is inconsistent with past practices, weights on expenditures have changed, and the treatment of housing costs.

Comparing Past and Present Inflation

- Marijn A. Bolhuis, Judd N. L. Cramer, and Lawrence H. Summers

- Review of Finance

- A version of this paper can be found here

- Want to read our summaries of academic finance papers? Check out our Academic Research Insight category.

What are the research questions?

- Briefly, how are the components of the CPI index aggregated?

- What differences are noted between the two methods?

What are the Academic Insights?

- The BLS Handbook of Methods (Handbook of Methods : U.S. Bureau of Labor Statistics (bls.gov)) divides the urban areas of the US into 32 geographic areas. All consumer goods and services are divided into 211 “item strata” made up of 209 commodities and services item strata and two housing item strata. The housing item strata are the main focus of this research. Once the measured price increases are determined for the 7,000+ indexes, the BLS uses a modified Laspeyres approach to aggregate those indexes into the published CPI. The authors explain the Laspeyres aggregation: “The Laspeyres index falls within the Lowe index, a class of fixed weight indexes that uses weights from a period before the base period. The Laspeyres index uses estimated quantities from the predetermined expenditure reference period to weight each basic item–area index. These quantity weights currently remain fixed for 2 years and are replaced in January of each even-numbered year when the aggregation weights are updated. In a Laspeyres aggregation, consumer substitution between items is assumed to be zero. The CPI is not a pure Laspeyres index, as the goods basket has evolved significantly over time with new inventions and higher income levels.”

- Using the BLS data over the post-war period, 32 components are extracted, along with quantity weight and relative significance of the components since the 1940s. For example, consumers have shifted spending from goods to services since that period. Consistently, the weights and importance of costs of housing, medical, education, and personal care have increased. The weights and importance of goods have fallen while the other components have increased. The reader is referred to the article to review the shifting importance of all 32 components in the index. In any case, adjustments to the historical CPI were made to reflect the weight changes. The authors make at least two predictions: First, the inflation we are currently experiencing is closer to that of the 1970s than it appeared initially. Using the corrected estimate, the current inflation level will fall to 2% in approximately three years. Second, inflationary cycles will exhibit less volatility than in the past. This is primarily due to the changing weight (greater) given to goods components in the past measures of the CPI.

Why does it matter?

It is important to recognize that the general public, journalists, academics, and policymakers consider the CPI the gold standard for comparisons within and across countries. The CPI substantially impacts the salaries of approximately 80 million workers and 47.8 beneficiaries of Social Security, 4.1 million civil service and military personnel, and 22.4 million recipients of food stamps. Understanding the methodology, biases, and momentum of components will impact the lives of many people. The Federal Reserve, however, has used the PCE price index since 2000 and is not subject to the instability induced by the housing issue.

For interested readers, the new series is available on Larry Summers’ website.

The most important chart from the paper

The results are hypothetical results and are NOT an indicator of future results and do NOT represent returns that any investor actually attained. Indexes are unmanaged and do not reflect management or trading fees, and one cannot invest directly in an index.

Abstract

There have been important methodological changes in the Consumer Price Index (CPI) over time. These distort comparisons of inflation from different periods, which have become more prevalent as inflation has risen to 40-year highs. To better contextualize the current run-up in inflation, this article constructs new historical series for CPI headline and core inflation that are more consistent with current practices

and expenditure shares for the post-war period. Using these series, we find that current inflation levels are much closer to past inflation peaks than the official series would suggest. In particular, the rate of core CPI disinflation caused by Volcker-era policies is significantly lower when measured using today’s treatment of housing: only 5 percentage points of decline instead of 11 percentage points in the official CPI statistics.

Disclosure: Alpha Architect

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Alpha Architect, its affiliates or its employees. Our full disclosures are available here. Definitions of common statistics used in our analysis are available here (towards the bottom).

This site provides NO information on our value ETFs or our momentum ETFs. Please refer to this site.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Alpha Architect and is being posted with its permission. The views expressed in this material are solely those of the author and/or Alpha Architect and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.