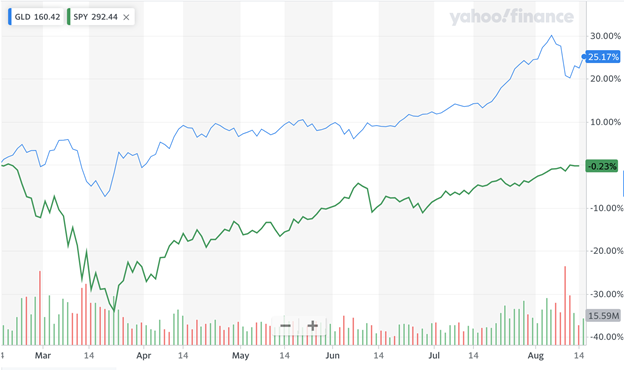

Gold is often viewed as a safe haven asset or a hedge against market turmoils, currency depreciation, and other economic or political events. At the beginning of the COVID pandemic, S&P 500 experienced a sharp drop before returning to pre-COVID level several months later. At the same time, SPDR Gold Shares (GLD) gained more than 25% from February to August 2020.

Figure 1: During Feb 18, 2020 — Aug 17, 2020 (6 months), the S&P 500 ETF (SPY in green) experienced a sharp drop before returning to pre-covid level. Meanwhile, the gold ETF (GLD in blue) has gained more than 25%. Source: Yahoo Finance.

To gain a long or short exposure to gold, there are a number of related products, including gold exchange traded funds (ETFs), gold miner stocks, and gold futures.

However, the price of gold does not exist in a vacuum. Gold must be mined, and the companies that perform this mining process are themselves traded companies. This gives another avenue for investors to achieve exposure to gold, while allowing them to determine investment decisions through standard equity research techniques.

Even though general equity sector ETFs are by far the largest by market capitalization, gold miner ETFs are some of the most popular vehicles for short-term trading available on the market. Market observations suggest that they are heavily driven by speculative traders seeking gold-like exposure. Therefore, understanding the underlying factor dynamics of gold miner ETF returns are practically useful for analyzing popular trading strategies, such as pairs trading.

A Model for Gold Miner Stocks

Standard equity market research has established several rules of thumb to understand the differences of investing in gold miners vs. gold itself. While in the long run there is a clear correlation between gold prices and miner equity prices, price divergence is not unusual. For example, the short-term performance of gold miners is very sensitive to both the market discount rate and payments of future dividends, which are dictated by the general equity markets.

Furthermore, at the individual firm level, management could have a significant impact on the equity returns through superior investment skills, mine openings and closures, cost cutting, or market timing. However, in the long run, the only way for gold miners to make money is to dig gold from the ground and sell it on the open market.

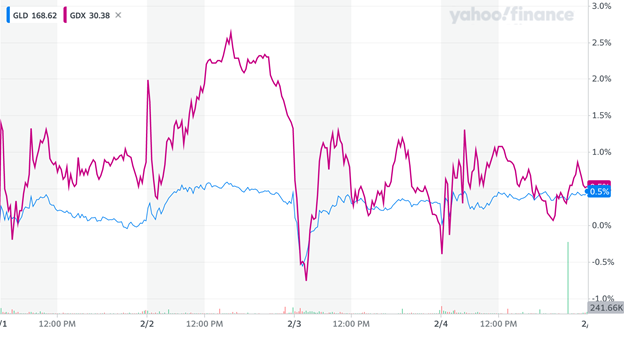

From the empirical perspective, gold miner stock prices are visibly more volatile than the gold spot price.

Figure 2: The cumulative returns of gold spot ETF (GLD in blue) and gold miners ETF (GDX in magenta) during 2/1/22-2/4/22. It appears that GDX tends to move in the same direction as GLD but with much higher volatility. This suggests that GDX is an Source: Yahoo Finance.

In our paper, we show that gold miner stocks are a leveraged play on physical gold.

Our stochastic model captures the connection between gold and miner stocks. It is a tractable structural model that directly relates gold prices to the value of gold miner equity via a combined optimal control and stopping problem. This real options model requires gold miners to set an internal production function, liquidating the company assets when gold prices decline past a certain level. In particular, our model suggests that a dynamic portfolio of physical gold is likely to perform identically to an actual portfolio of gold miners.

Our model gives closed-form analytical expressions for the value of the firm’s assets, the value of the firm’s equity, and precisely identifies the parameters which affect the firm’s leverage. In fact, we examine the predictions of our real options model, finding that a significant part of a gold miner firm’s leverage can be explained within the real options framework!

Implied Leverage

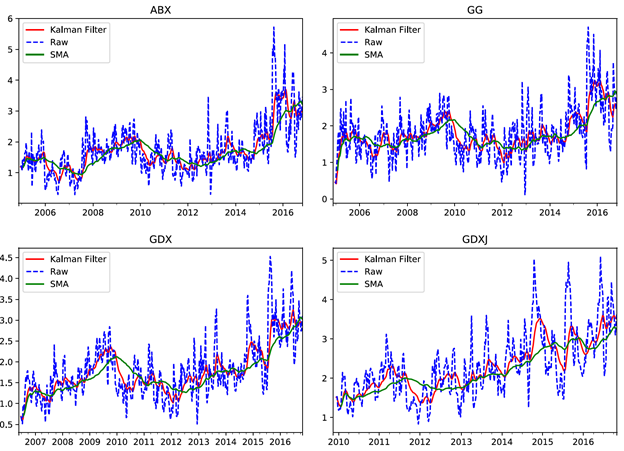

Furthermore, we use the insights from our structural model to develop a method to replicate gold miner stocks, using only physical gold and the market equity portfolio, that can explain about 70% of the variation in gold miner stock returns.

Figure 3: Plots of model implied gold leverage (raw) vs. Kalman filtered time series (red) and simple moving average (green) of the implied gold leverage, for Barrick Gold (ABX), Gold Corp (GG), Gold Miners ETF (GDX), Junior Gold Miners ETF (GDXJ). Source: Guo, Leung, and Ward (2019)

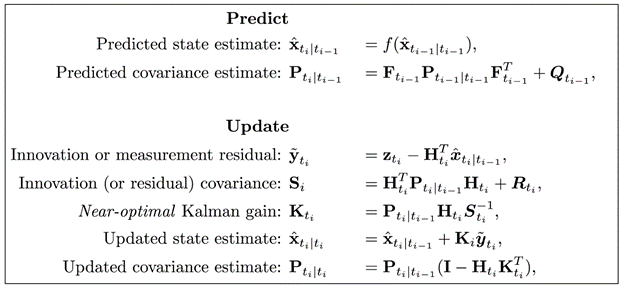

In the paper, we explain the Kalman filter procedure that looks like this:

Our main empirical insight suggests that gold miner equities have a call option-like payoff, which results in higher implied leverage and negative alpha relative to physical gold. In particular, over a long horizon, gold miner stocks may result in a sizable loss even if the physical gold price remains little changed (see Fig. 4).

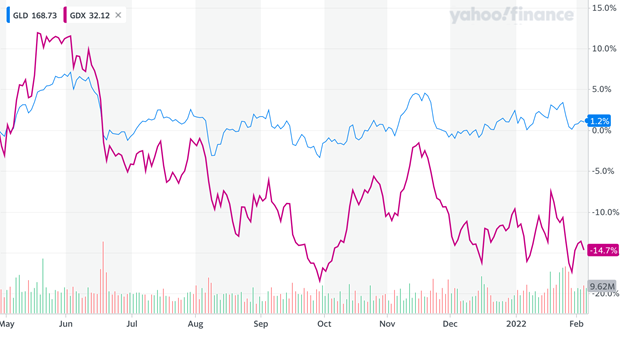

Figure 4: The cumulative returns of gold spot ETF (GLD in blue) and gold miners ETF (GDX in magenta) during 5/1/21-2/4/22. Even though GLD price has changed little and notched a small positive return, GDX has lost more than 14% with high volatility throughout the period. Source: Yahoo Finance.

With interest rate hike on the horizon, some may expect the gold price to tumble and anticipate a sell-off of gold miner stocks. Will a long-spot-short-miner strategy work in this case? To that end, it is crucial to quantify the stochastic leverage of gold miner stocks with respect to physical gold.

Disclaimer: This post is not intended to be investment advice.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Computational Finance & Risk Management, University of Washington and is being posted with its permission. The views expressed in this material are solely those of the author and/or Computational Finance & Risk Management, University of Washington and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.