![[Gamma] Scalping Please](https://ibkrcampus.com/wp-content/smush-webp/2024/04/tir-featured-8-700x394.jpg.webp "[Gamma] Scalping Please")

See Part I for instructions on how to get pandas_datareader or yfinance module to retrieve the data, Part II to learn how to get stock market data for different geographies, and Part III for a tutorial on how to analyse the stock market data for all the stocks which make up the S&P 500.

Resample Stock Data

Convert 1-minute data to 1-hour data or Resample Stock Data

During strategy modelling, you might be required to work with a custom frequency of stock market data such as 15 minutes or 1 hour or even 1 month.

If you have minute level data, then you can easily construct the 15 minutes, 1 hour or daily candles by resampling them. Thus, you don’t have to buy them separately.

In this case, you can use the pandas resample method to convert the stock market data to the frequency of your choice. The implementation of these is shown below where a 1-minute frequency data is converted to 10-minute frequency data.

The first step is to define the dictionary with the conversion logic. For example, to get the open value the first value will be used, to get the high value the maximum value will be used and so on.

The name Open, High, Low, Close and Volume should match the column names in your dataframe.

ohlcv_dict = {

'Open': 'first',

'High': 'max',

'Low': 'min',

'Close': 'last',

'Volume': 'sum'

}Convert the index to datetime timestamp as by default string is returned. Then call the resample method with the frequency such as:

- 10T for 10 minutes,

- D for 1 day and

- M for 1 month

# Import package & get the data

import yfinance as yf

intraday_data = yf.download(tickers="MSFT",

period="5d",

interval="1m",

auto_adjust=True)

# Define the resampling logic

ohlcv_dict = {

'Open': 'first',

'High': 'max',

'Low': 'min',

'Close': 'last',

'Volume': 'sum'

}

# Resample the data

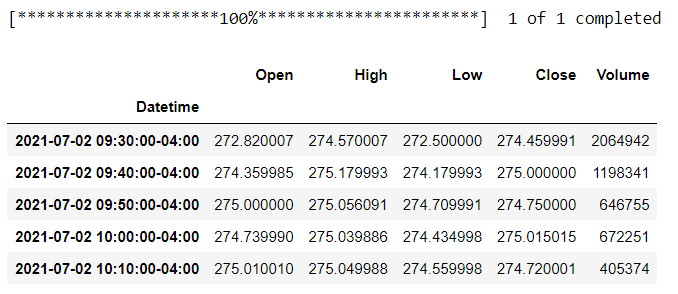

intraday_data_10 = intraday_data.resample('10T').agg(ohlcv_dict)

intraday_data_10.head()

resample_data_10.py hosted with ❤ by GitHub

Yahoo finance has limited set of minute level data. if you need the stock market data for higher range then you can get the data from data vendors such as Quandl, AlgoSeek or your broker.

Stay tuned for next installment in which Ishan Shah will demonstrate using Quandl to get Stock Market Data.

See https://blog.quantinsti.com/stock-market-data-analysis-python/ for additional insight on this topic.

Past performance is not indicative of future results.

Any stock, options or futures symbols displayed are for illustrative purposes only and are not intended to portray recommendations.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from QuantInsti and is being posted with its permission. The views expressed in this material are solely those of the author and/or QuantInsti and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.