![[Gamma] Scalping Please](https://ibkrcampus.com/wp-content/smush-webp/2024/04/tir-featured-8-700x394.jpg.webp "[Gamma] Scalping Please")

Volatility is a fascinating topic primarily because change is constant, but the rate of change is not. This year has been fraught with adjustments in capital markets. The most significant changes have occurred in fixed income markets, but the cost of capital influences everything from equity indexes to grocery bills.

When discussing broad-based indexes, the conversation typically centers around historical (realized) and/or implied (forward estimate) volatility.

Realized volatility is based on past price data (often closing levels). Specifically, it is the standard deviation of daily returns annualized. Implied volatility calculations depend on a pricing model and the current value for an option. The level of volatility implied by the price of the option can be backed out by rearranging the model. Implied volatility measures change as the other variables in a pricing model change. Options traders tend to focus on implied volatility levels.

Historically, market participants have cited the CBOE Market Volatility Index (VIX) as a macro measure of forward-volatility expectations. Nasdaq changed the competitive landscape with the introduction of its VOLQ Index as well as associated futures and options.

Key Dates:

- 1/24/2019: VOLQ Index (VOLQ) launch (Nasdaq)

- 10/5/2020: VOLQ Futures (VLQ) launch (CME)

- 6/14/2022: VOLQ Index Options (VOLQ) launch (Nasdaq)

There are a few distinctions between the VIX Index and VOLQ Index that need to be understood. First, S&P 500 Index Options (SPX) are used to calculate a VIX level, whereas Nasdaq-100 Index Options (NDX) inform the VOLQ Index. The second key contrast is that the VIX methodology employs a variance replicating approach, which includes a large and variable range of out-of-the-money (OTM) SPX calls/puts (midpoint values) with more than 23 days and less than 37 days until expiration. The options are time-weighted to create a blended 30-day forward measure of volatility (annualized).

By contrast, the VOLQ methodology uses a much more precise set of option strikes. Specifically, the VOLQ Index uses 32 call and put options that are struck precisely ATM. The options series are also time-weighted to create a 30-day forward volatility measure (annualized) that references the Nasdaq-100 Index (NDX).

Interactive Broker’s Chief Strategist, Steve Sosnick, explained the differences between VOLQ and CBOE Nasdaq-100 Volatility Index (VXN) in a piece last year. He succinctly explains how the inclusion of well OTM options (incorporating skew) changes volatility forecasts. In short, the Cboe methodology dictates that VXN will likely remain at a premium to VOLQ as a function of index option skew.

VOLQ’s focal point, ATM NDX Index Options, allows market participants to isolate NDX skew and focus instead on the ATM forecast. Sosnick concludes: “I believe that Nasdaq has given us a new tool in VOLQ that we can utilize for volatility analysis…As always, volatility is a nuanced topic, but one that can reward curious traders who understand those nuances.” I concur.

The information embedded in both VIX and VOLQ is useful. However, over the past decade, the composition of portfolios has evolved. In many situations, they more closely resemble the NDX sector makeup. In other words, institutions and individuals have allocated more capital toward information technology and consumer discretionary names relative to areas like financials, energy and real estate.

The correlation between the S&P 500 Index (SPX) and NDX remains high. Still, VOLQ is arguably a more useful forecasting tool for many market participants because it references the index (NDX) that more closely reflects their capital allocation.

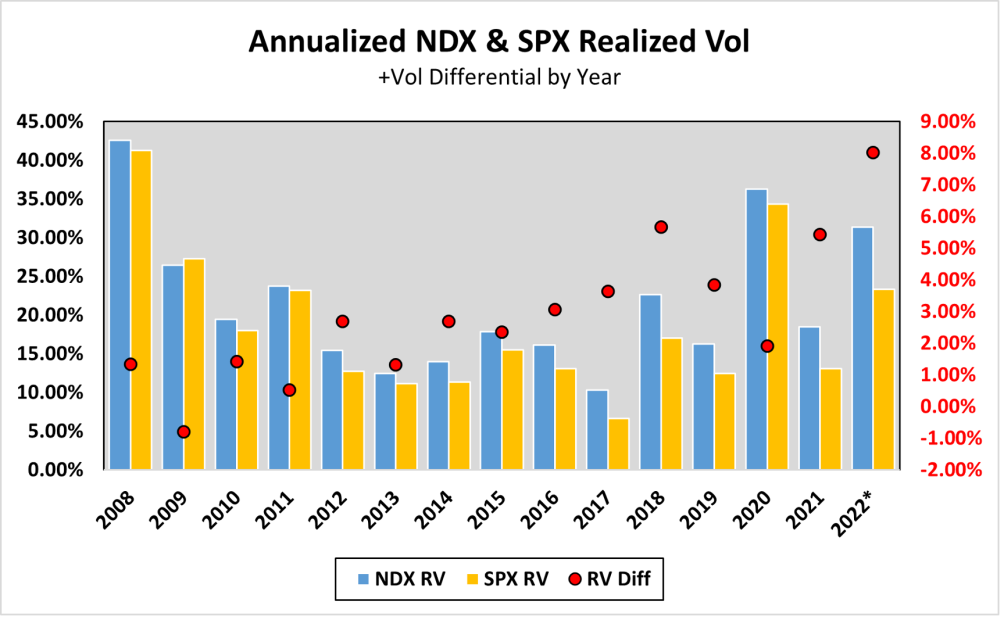

Volatility Spreads

Source: NASDAQ

Furthermore, in 2022, the spread between NDX and SPX realized volatility is wider now than it’s been in over a decade. On average, between 2008 and the end of 2021, annualized NDX volatility was 2.51 vols higher than realized SPX volatility. However, through the end of November, NDX has realized 31.4% volatility (standard deviation of daily returns) compared to an SPX with a realized volatility of 23.4%.

The above visual plots the annual realized volatility for NDX (light blue) and SPX (yellow) as well as the spread between those measures (red dot). The 8-volatility point spread this year is highly unusual. Then again, the shift in monetary policy is historically unprecedented. The disparity in price return and historical volatility levels is, in large part, explained by the dramatic shift in the cost of money.

The other key distinguishing characteristic of the VLQ Futures relative to VIX Futures is the contract multiplier. VLQ Futures have a 100 multiplier, whereas standard VIX Futures have a 1,000 multiplier. From a notional standpoint, VLQ Futures are slightly less than 1/10th the size of a standard VIX contract.

Example:

- Dec 2022 VLQ Futures: $26.00*100 = $2,600 notional exposure

- Dec 2022 VIX Futures: $21.50*1000 = $21,500 notional exposure

Volatility impacts all facets of our lives. In capital markets, there’s an emphasis on understanding, quantifying and managing potential volatility risk. The introduction of VOLQ Index Options and VLQ Futures affords market participants the ability to manage risk or gain exposure to NDX forward volatility. The VOLQ Index and derivative products offer a rich set of data that illuminates the past and provides a dynamic estimate of what may occur in the future.

The end of a year gives us an opportunity to (re)assess our portfolios. New products, like VOLQ Index Options and VLQ Futures, provide investors with unique tools that can be incorporated into both active and passive risk management strategies.

For more on VOLQ Index Options and VLQ Futures, watch our Now You Have Choices in Volatility Trading video.

If you have questions about leveraging VOLQ in your portfolio, don’t hesitate to reach out to us at indexoptions@nasdaq.com.

—

Originally Posted January 12, 2023 – Nasdaq-100® Volatility Index Options (VOLQ): A Year in Review

The views and opinions expressed herein are the views and opinions of the author and do not necessarily reflect those of Nasdaq, Inc.

Disclosure: Nasdaq

Index

Nasdaq® is a registered trademark of Nasdaq, Inc. The information contained above is provided for informational and educational purposes only, and nothing contained herein should be construed as investment advice, either on behalf of a particular security or an overall investment strategy. Neither Nasdaq, Inc. nor any of its affiliates makes any recommendation to buy or sell any security or any representation about the financial condition of any company. Statements regarding Nasdaq-listed companies or Nasdaq proprietary indexes are not guarantees of future performance. Actual results may differ materially from those expressed or implied. Past performance is not indicative of future results. Investors should undertake their own due diligence and carefully evaluate companies before investing. ADVICE FROM A SECURITIES PROFESSIONAL IS STRONGLY ADVISED.

© 2023. Nasdaq, Inc. All Rights Reserved.

Options

For the sake of simplicity, the examples included do not take into consideration commissions and other transaction fees, tax considerations, or margin requirements, which are factors that may significantly affect the economic consequences of a given strategy. An investor should review transaction costs, margin requirements and tax considerations with a broker and tax advisor before entering into any options strategy.

Options involve risk and are not suitable for everyone. Prior to buying or selling an option, a person must receive a copy of Characteristics and Risks of Standardized Options. Copies may be obtained from your broker, one of the exchanges or The Options Clearing Corporation, One North Wacker Drive, Suite 500, Chicago, IL 60606 or call 1-888-OPTIONS or visit www.888options.com.

Any strategies discussed, including examples using actual securities and price data, are strictly for illustrative and education purposes and are not to be construed as an endorsement, recommendation or solicitation to buy or sell securities.

© 2023. Nasdaq, Inc. All Rights Reserved.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Nasdaq and is being posted with its permission. The views expressed in this material are solely those of the author and/or Nasdaq and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Options Trading

Options involve risk and are not suitable for all investors. Multiple leg strategies, including spreads, will incur multiple commission charges. For more information read the "Characteristics and Risks of Standardized Options" also known as the options disclosure document (ODD) or visit ibkr.com/occ