It’s been roughly two months now operating in a post-Silicon Valley Bank (SVB) world, and the markets are still feeling its impact. While the stock and bond markets continue to wrestle with the fallout from both an economic and regional banking concern perspective, there is a very important arena where developments have seemingly flown under the radar of late (which is a good thing): the funding markets.

When banking-related issues “hit the tape,” one of the first locations investors should turn to see if there are any negative effects is the funding markets. Indeed, throughout modern financial history, it is this arena where dislocations can “snowball” and turn a potentially isolated occurrence into a systemic event. Certainly, the 2007–2008 great financial crisis underscored that point, but we’ve also witnessed other episodes where pressures were evident, such as the COVID-19 lockdown.

The Federal Reserve (Fed) is well aware of these scenarios as well. In fact, the Fed acted rather swiftly this time around and implemented the Bank Term Funding Program (BTFP) in response to the first wave of adverse news that came out from Silicon Valley Bank (SVB) and Signature Bank in early March. BTFP was created specifically to offer “funding available to eligible depository institutions.” What can be considered one of the key aspects of this program is that the pledged collateral, such as Treasuries, “will be valued at par,” not only making funding available if needed but also “eliminating an institution’s need to quickly sell those securities in times of stress,” which was one of the major catalysts behind the regional banking turmoil in the U.S.

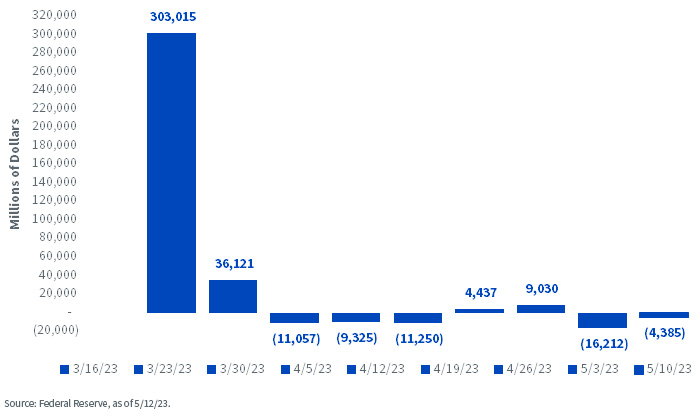

Fed Balance Sheet: The Total Change in Lending Facilities

When looking at the Fed’s key available lending facilities, there are three components to examine: primary credit at the discount window, BTFP and other credit extensions (FDIC-related loans). As you can see, banks utilized these facilities in a visible way in the immediate wake of the turmoil, but since mid-March, total usage has dropped off considerably. To provide some perspective, after hitting a peak increase of $303.0 billion on March 16, the total amount has declined in five out of the last seven weeks, falling by $4.4 billion as of May 10. The bottom-line message is that the Fed’s facilities acted as they were intended and arguably prevented any further calamity up to this point.

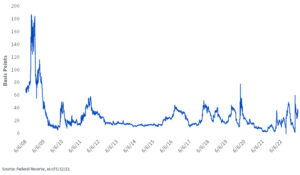

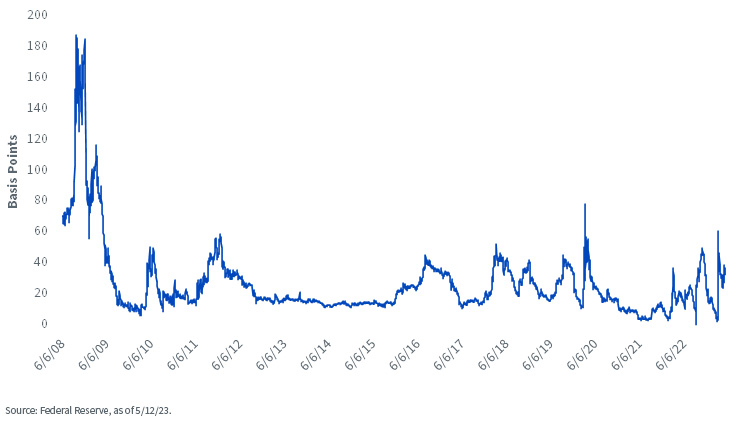

U.S. Interest Rate Swaps

This point has been buttressed by what has also transpired in the aforementioned funding market. The U.S. interest rate swap market (an agreement between counterparties to exchange fixed versus floating cash flows) provides a clear look at developments in this arena. For the record, the wider the spread, as measured in basis points (bps), theoretically, the more pressure, or dislocations, there is for institutions to find funding. As you can see, there was a spike in funding pressures around mid-March, but conditions have steadily improved since then. While the spread has not returned to its pre-SVB reading, it has remained relatively stable (+35 bps) and is well within recent trading ranges and considerably below the high watermarks of the financial crisis (+188 bps) and COVID-19 lockdown (+78 bps).

Conclusion

With regional bank concerns still making headlines, it remains a prudent idea to continue monitoring developments. However, if the funding markets continue to operate as outlined here, the markets, and perhaps more importantly, the Fed, can focus more on the potential economic ramifications that may lie ahead. More on this in a later blog post…

—

Originally Posted May 17, 2023 – Some Perspective on Banking Woes: Two Months Later

Disclosure: WisdomTree U.S.

Investors should carefully consider the investment objectives, risks, charges and expenses of the Funds before investing. U.S. investors only: To obtain a prospectus containing this and other important information, please call 866.909.WISE (9473) or click here to view or download a prospectus online. Read the prospectus carefully before you invest. There are risks involved with investing, including the possible loss of principal. Past performance does not guarantee future results.

You cannot invest directly in an index.

Foreign investing involves currency, political and economic risk. Funds focusing on a single country, sector and/or funds that emphasize investments in smaller companies may experience greater price volatility. Investments in emerging markets, real estate, currency, fixed income and alternative investments include additional risks. Due to the investment strategy of certain Funds, they may make higher capital gain distributions than other ETFs. Please see prospectus for discussion of risks.

WisdomTree Funds are distributed by Foreside Fund Services, LLC, in the U.S. only.

Interactive Advisors offers two portfolios powered by WisdomTree: the WisdomTree Aggressive and WisdomTree Moderately Aggressive with Alts portfolios.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree U.S. and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree U.S. and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.