![[Gamma] Scalping Please](https://ibkrcampus.com/wp-content/smush-webp/2024/04/tir-featured-8-700x394.jpg.webp "[Gamma] Scalping Please")

Key takeaways

Conflicting signals

Traditional market indicators are sending inconsistent messages — the usual markers point to a recession, but the economy is strong.

A hard or soft landing?

The evidence may still point to a reasonably soft landing for the US economy, but we still await the lagged effects of monetary policy tightening.

A lost decade?

Are we headed for a lost decade for equity returns, like the 1970s or 2000s? Despite some similarities between then and now, I vote no.

In last month’s column, I concluded by pointing to the January Barometer, which says that positive stock market returns in January may be a predictor of positive returns over the rest of the year. Supposedly it has an 86% hit rate1 (which may not be as impressive as it sounds, given that stocks have been positive in roughly 75% of the years since 1901 anyway).2 Regardless, after January’s positive returns, I was about to declare victory and take the rest of the year off …

… then in February, the Kansas City Chiefs from the American Football Conference won the Super Bowl, and apparently that’s a bad omen. On average, markets have historically performed better when a team from the National Football Conference wins.3 (As if Philadelphia fans weren’t upset enough about that late-game flag!)

So, the superstition-fueled market predictors are sending conflicting signals. That’s ok. The traditional indicators are sending inconsistent signals too — the usual markers point to a recession, but the economy is strong. Disinflation appears to be here, only maybe it’s not.

Since I’m no longer taking the year off, let’s delve into it.

A ‘keep it simple’ strategy

1) Where are we in the cycle?

Will the economy’s landing be hard or soft? There hasn’t been this much debate over those labels since the last time I selected a taco shell. The evidence may still point to a reasonably soft landing (inflation has been moderating, growth has been resilient), but we still await the lagged effects of monetary policy tightening. Remember, it roughly takes 12-18 months for tighter policy to be felt in the economy — and one year ago the Fed Funds Rate was 0.00%.4 I’d still characterize the risks to the cycle as high, but I believe that a mild recession was priced by the market last year.

2) What’s the market telling us about the direction of the economy?

Financial markets have been in recovery mode. How can that be? The market leads the economy, not vice versa. Last year the market was looking ahead to a growth contraction by mid-2023 (seems reasonable), while now the market appears to be anticipating an economic recovery in the latter part of this year and into next year. But the path between now and then won’t be a straight line for markets. Financial conditions could tighten in the coming months (stronger dollar, lower equity valuations) if it becomes clear that more policy tightening is in the offing.

3) What will be the Federal Reserve’s policy response?

All eyes are on the Fed. Inflation expectations are climbing again5 albeit from low levels, and expectations for the Fed Funds Rate have been ratcheted higher6. We’re confident that inflation has peaked and will continue to come down, but perhaps not as fast as the Fed had hoped. The Fed pause may not be coming now until the middle of the year, at the earliest.

Ok, wait. It’s a recovery until it isn’t, but then it will be again? Well, yes. The current market recovery may not be the recovery. Markets may retrace some of the recent gains if inflation slows by less than expected and if the economy becomes less resilient. Tactical investors may want to lock in recent gains and become more defensive. Nonetheless, history tells us that markets have tended to do well over the subsequent 1-, 2-, and 3-year periods after inflation peaks.7 I’m a FOMO guy. I have a Fear Of Missing Out on most things, particularly a post-inflationary environment intermediate-term market advance.

It may be confirmation bias, but …

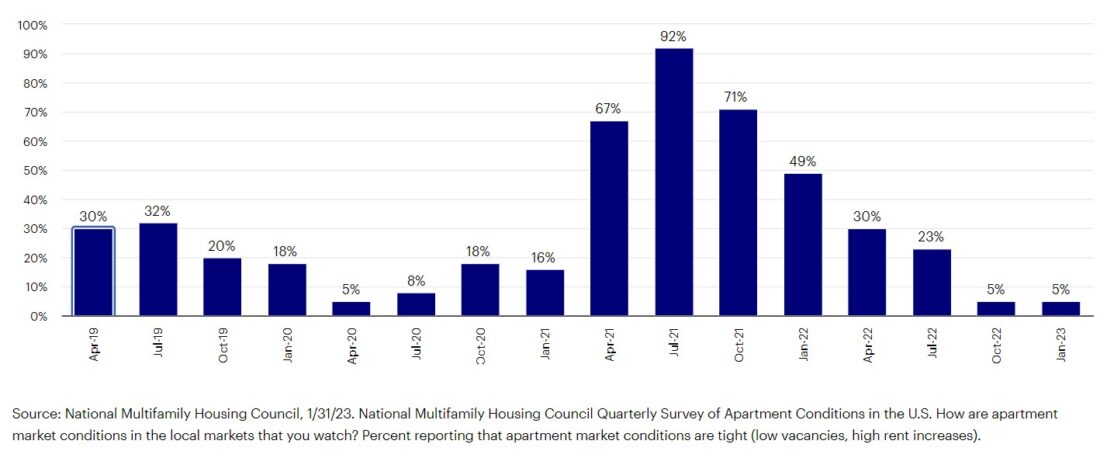

…shelter costs, which have significant relevance to services inflation in the Consumer Price Index8, appear poised to decline. For example, a survey from the National Multifamily Housing Council highlights that conditions in the apartment industry are now near lows last seen during the early days of the pandemic.9 In the past, a sharp decline in the apartment conditions survey has presaged a moderation in rental prices.10

National Multifamily Housing Council Quarterly Survey of Apartment Conditions

Percent reporting that apartment market conditions are tight (low vacancies, high rent increases)

Automate my job?

I’m introducing a new category. Each month I’ll pose a question to ChatGPT — the artificial intelligence (AI)-driven chatbot — and assess the response.

Q: Is the US economy heading towards a recession?

(Note: the first few times I asked the question, the response was, “ChatGPT is at capacity right now.” Can I use that response at work?)

A: As an AI language model, I do not have access to real-time economic data beyond my knowledge cut-off date of September 2021…It is important to note that the US economy is influenced by many complex factors…Therefore, predicting the direction of the US economy can be challenging and subject to many variables.

Tell me about it! The most predicted recession in memory has still failed to materialize. Nonetheless, I would have been impressed if ChatGPT had said something more like this: “Recessions tend to occur when the Fed raises rates to cool inflation, growth slows as a result, and the banks tighten lending standards amid rising creditor concerns. Each of these things appears to be happening.”

I suppose my job is secure for another month at a minimum.

It was said

“It looks more possible that we’ll have a soft landing than it did a few months ago,” – Lawrence Summers, Former US Treasury Secretary

A far cry from when Summers was warning that without a high rise in the unemployment rate, inflation would become entrenched. Lest we get too optimistic, Summers continues to warn that the “greatest tragedy” would be if central banks don’t finish the job.

“We got to get 218. We’re trying to get the framework. We want all buy in.” – Ralph Norman, US Representative (R-SC 5th District)

The debt ceiling game of chicken is on. The White House and Senate Democrats don’t believe that House Speaker Kevin McCarthy has the votes to raise the debt ceiling. To them, ironically, that’s a good thing. They reason that the Republicans will ultimately have to vote to raise the debt ceiling with no strings attached, to avoid default. The Republicans are looking to strengthen their bargaining position by finding a proposal for future spending cuts that the party can get behind. Here’s hoping that everyone realizes we’re all in the same car.

“I don’t think the American people need to worry about aliens with respect to these crafts, period.” – John Kirby, White House Spokesperson, addressing the multiple unidentified flying objects recently shot out of the sky by the US military.

I’m not sure if I’m disappointed or not.

Phone a friend

Are equity valuations too elevated for a new market cycle to commence? Let’s put the questions to Talley Leger, Invesco’s Equity Strategist:

“Stock valuations have already experienced a downward adjustment. Remember the S&P 500 Index’s price/earnings ratio at the beginning of 2022 was 30x.11 Equity multiples fell to 17x by October 2022 as higher interest rates compressed what investors were willing to pay for earnings, while at the same time earnings continued to expand.12

This raises the question of where equity valuations were at the start of the past few major market bottoms. The answer: 18.5x in 2002, 16.3x in 2009, and 18.6x in March 2020, suggesting that there is nothing about valuations at the Oct. 13, 2022, trough that would inhibit a new market advance13.”

Since you asked

Will this be a lost decade for equity returns like it was in the 1970s or 2000s?

Admittedly, there are some parallels between then and now. Inflation is elevated as it was in the 1970s. And, like in the early 2000s, investors have reassessed what they are willing to pay for equities in a new interest rate environment. But I’d argue that’s where the similarities largely end.

- In the 1970s, the Fed had lost credibility as long-term inflation expectations were in the double digits14, fostering a prolonged period of policy uncertainty that weighed on markets. Currently, long-term inflation expectations are within the Fed’s perceived “comfort zone.”15

- In the 2000s, interest rates, in hindsight, were left low for too long and ushered in an era of substantial leverage and bank balance sheet impairment, culminating in a global financial crisis. Now, a substantial amount of monetary policy tightening has already occurred.16 In addition, leverage remains relatively benign17 while the nation’s banks appear to be well-capitalized18.

Everyone gets a podcast

Matt Brill, Invesco’s Head of North American Investment Grade Credit, returned to the Greater Possibilities podcast to talk about investment grade bonds and much more. Matt shared his opinion that:

- The Fed will win the battle against inflation. It’s not over yet and they may be slow to declare victory, but that conquest is coming.

- The runway for a soft landing for the economy has gotten wider because despite all the policy tightening, the labor market is still strong.

- The market’s view of bonds has moved from TINA — There Is No Alternative (to equities) — to TARA — There’s A Reasonable Alternative (in which bonds are attractive).

- It’s time to take a closer look at the yields offered by intermediate-term bonds. Yes, short rates are attractive, but why not lock in the yields?

- Fundamentals suggest that corporations can handle the current environment well and yields are attractive.

On the road again

My travels took me to a wealth management event at Raymond James Stadium in Tampa, Florida. I’d be lying if I said I didn’t contemplate finding a place in the stadium to hole up until the Taylor Swift concert on April 13.

It’s always a pleasure to be on an agenda with many of Invesco’s accomplished investors. A highlight was listening to Mark Paris, Chief Investment Officer and Head of Municipal Bonds. For one, Mark believes that the fundamentals of the municipal bond business are as good, if not better, than they have been in his long career. Second, he believes that investors who missed the rally in municipal bonds are being presented with another opportunity given the backup in rates. Good insight, Mark!

I’ll see you in March. These markets may go into the month like a lion. A pullback from recent gains could last for a bit. Beyond that, we would expect markets to progress through the year and go into 2024 more like a lamb.

Footnotes

- 1Source: Standard & Poor’s, 12/31/22. Based on returns of the S&P 500 Index from 1957 to 2022.

- 2Source: Bloomberg, 12/31/22. Based on the rolling monthly 1-year returns of the Dow Jones Industrial Average from 1901 to 2022.

- 3Source: Bloomberg, 12/31/22. Based on returns of the S&P 500 Index from 1967 to 2022. The average return of the S&P 500 in years that an NFC won the championship is 10% versus 6.9% in years that an AFC team won.

- 4Source: US Federal Reserve, 1/31/23.

- 5Source: Bloomberg, 2/16/23. Based on the 1-year US Inflation Breakeven. The breakeven inflation rate is calculated by subtracting the yield of an inflation-protected bond from the yield of a nominal bond during the same period.

- 6Source: Bloomberg, 2/16/23. Based on Fed Funds Implied Rates.

- 7Source: Bloomberg, 1/31/23. Based on S&P 500 Index returns following the inflation peaks in February 1970, December 1974, March 1980, December 1990 and July 2008. On average, the S&P 500 had a cumulative return of 17% one-year after the peak, 28% two years after, and 46% three years after.

- 8Source: US Bureau of Labor Statistics, 1/31/23.

- 9Source: National Multifamily Housing Council, 1/31/23. National Multifamily Housing Council Quarterly Survey of Apartment Conditions. How are apartment market conditions in the local markets that you watch? Percent reporting that apartment market conditions are tight (low vacancies, high rent increases).

- 10Source: National Multifamily Housing Council, 1/31/23.

- 11Source: Bloomberg, 1/1/21.

- 12Source: Bloomberg, 1/31/23. As represented by the S&P 500 Index.

- 13Source: Bloomberg, 1/31/23. As represented by the S&P 500 Index.

- 14Source: University of Michigan Consumer Survey.

- 15Source: University of Michigan Consumer Survey.

- 16Source: Bloomberg, 1/31/23. Based on Fed Funds Implied Futures.

- 17Source: US Federal Reserve. Based on Nonfinancial Corporate Debt to Profits ratio.

- 18Source: US Federal Reserve, 1/31/23. Based on Tier 1 Risk-Based Capital Ratios.

—

Originally Posted February 27, 2023

Above the Noise: Sorting through the market’s conflicting signals by Invesco US

Important information

NA 2751602

Investors should consult a financial professional before making any investment decisions. This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial professional before making any investment decisions.

All investing involves risk, including the risk of loss.

Past performance does not guarantee future results.

Investments cannot be made directly in an index.

Fixed-income investments are subject to credit risk of the issuer and the effects of changing interest rates. Interest rate risk refers to the risk that bond prices generally fall as interest rates rise and vice versa. An issuer may be unable to meet interest and/or principal payments, thereby causing its instruments to decrease in value and lowering the issuer’s credit rating.

Municipal securities are subject to the risk that legislative or economic conditions could affect an issuer’s ability to make payments of principal and/ or interest.

In general, stock values fluctuate, sometimes widely, in response to activities specific to the company as well as general market, economic and political conditions.

Disinflation, a slowing in the rate of price inflation, describes instances when the inflation rate has reduced marginally over the short term.

The Dow Jones Industrial Average is a price-weighted index of the 30 largest, most widely held stocks traded on the New York Stock Exchange.

The Consumer Price Index (CPI) measures change in consumer prices as determined by the US Bureau of Labor Statistics. Core CPI excludes food and energy prices while headline CPI includes them.

The S&P 500® Index is a market-capitalization-weighted index of the 500 largest domestic US stocks.

The Fed Funds Rate is the rate at which banks lend balances to each other overnight.

A basis point is one hundredth of a percentage point.

Tightening is a monetary policy used by central banks to normalize balance sheets.

The price-to-earnings (P/E) ratio measures a stock’s valuation by dividing its share price by its earnings per share.

A multiple is any ratio that uses the share price of a company along with some specific per-share financial metric to measure value. Generally speaking, the higher the multiple, the more expensive the stock.

The Survey of Consumers is a monthly telephone survey conducted by the University of Michigan that provides indexes of consumer sentiment and inflation expectations.

The Tier 1 common capital ratio compares a bank’s core equity capital with its total risk-weighted assets.

ChatGPT is an artificial intelligence language model that was released in November 2022 and generates human-like text based on inputs it is given.

The opinions referenced above are those of the author as of Feb. 14, 2023. These comments should not be construed as recommendations, but as an illustration of broader themes. Forward-looking statements are not guarantees of future results. They involve risks, uncertainties and assumptions; there can be no assurance that actual results will not differ materially from expectations.

Disclosure: Invesco US

This does not constitute a recommendation of any investment strategy or product for a particular investor. Investors should consult a financial advisor/financial consultant before making any investment decisions. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

NOT FDIC INSURED

MAY LOSE VALUE

NO BANK GUARANTEE

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is the US distributor for Invesco Ltd.’s Retail Products and Collective Trust Funds. Institutional Separate Accounts and Separately Managed Accounts are offered by affiliated investment advisers, which provide investment advisory services and do not sell securities. These firms, like Invesco Distributors, Inc., are indirect, wholly owned subsidiaries of Invesco Ltd.

©2024 Invesco Ltd. All rights reserved.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Invesco US and is being posted with its permission. The views expressed in this material are solely those of the author and/or Invesco US and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

![[Gamma] Scalping Please](https://ibkrcampus.com/wp-content/smush-webp/2024/04/tir-featured-8-300x169.jpg.webp "[Gamma] Scalping Please")