![[Gamma] Scalping Please](https://ibkrcampus.com/wp-content/smush-webp/2024/04/tir-featured-8-700x394.jpg.webp "[Gamma] Scalping Please")

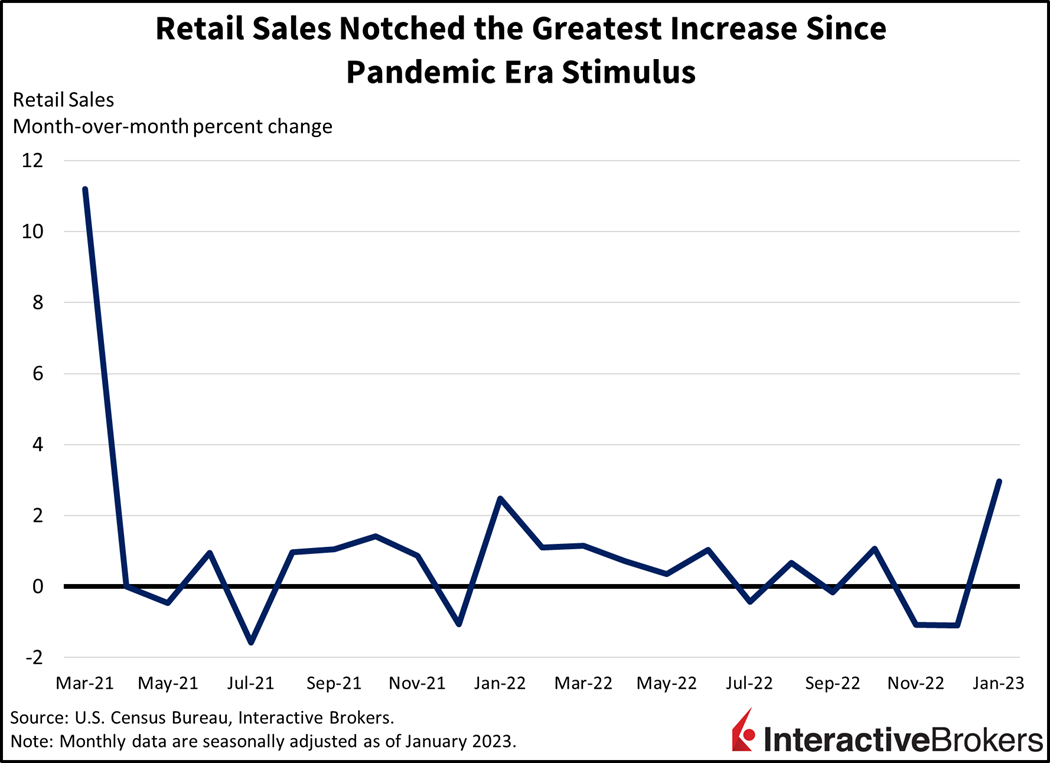

Investor sentiment turned south this morning following the release of surprisingly strong retail sales data for January. Sales climbed 3% as consumers proved resilient to higher prices, a result of a strong labor market. Consumer optimism is thriving despite the powerful headwinds of strong inflation and higher interest rates. The blockbuster January, combined with a hotter than expected CPI yesterday and the burning hot jobs number from 12 days ago, continues to weigh on the disinflationary outlook. In fact, Treasury yields at the short-end have jumped and achieved 5 handles at the 6-month and 1-year maturities, levels not seen since 2007 during the tightening cycle piloted by former Federal Reserve Chairman Alan Greenspan.

The blockbuster January, combined with a hotter than expected CPI yesterday and the burning hot jobs number from 12 days ago, continues to weigh on the disinflationary outlook. In fact, Treasury yields at the short-end have jumped and achieved 5 handles at the 6-month and 1-year maturities, levels not seen since 2007 during the tightening cycle piloted by former Federal Reserve Chairman Alan Greenspan.

While stronger consumption and a hot labor market is great news for consumers and businesses, it also provides additional yards of runway for the Fed to continue constraining monetary policy. Stronger consumption leads to higher inflation, and data released this month show that the Fed’s efforts to dampen demand has proven deficient. With Fed member Lael Brainard moving on to become the White House economic advisor, the central bank is down one big dovish voice, so January’s data releases will likely tilt the Fed increasingly hawkish, resulting in volatility for investors throughout 2023.

The S&P 500 and the tech-heavy Nasdaq indices are down roughly 0.5% in early trading. Against the backdrop of a relatively tighter Fed versus other central banks, the dollar index is catching a strong bid, up 0.7% to 104. Yields are also resuming their upward march albeit less intensely after rocket-launch type price moves in the last few weeks, with the 2-year up 3 basis points (bps) and the 10-year up 2 bps. WTI crude oil is down 1% to around $78.30 a barrel.

Retail sales shattered expectations in January, rising 3% versus the 1.8% anticipated, the greatest month-over-month (m/m) increase since pandemic era stimulus in March 2021. January’s data comes after November and December each experienced sales declines of 1.1%. Broad-based strength was seen in the January report, with consumers benefitting from sharply lower interest rates in January versus December as financial conditions loosened. Interest-rate sensitive, big-ticket items caught a bid last month as consumers purchased motor vehicles, furniture, electronics and appliances, with the segments reporting handsome increases of 5.9%, 4.4% and 3.5%. Consumers didn’t shy away from experiences either with sales at dining establishments and drinking parlors up 7.2%. Not one segment notched a decline during the period, pointing to strong consumer demand, too strong for the Fed.

Airbnb is an example. Its fourth quarter revenue of $1.90 billion exceeded the Refinitiv analyst consensus expectation of $1.86 billion and jumped 24% year over year (y/y). The company estimates that current quarter revenues will range from $1.75 billion to $1.82 billion, exceeding the consensus expectation of $1.69 billion. Strong revenue growth has resulted in the company’s fourth quarter net income climbing from $55 million to $319 million y/y.

Airbnb travelers appear to also be splurging on snacks, with Kraft Heinz reporting a 10% fourth quarter y/y increase in sales, driven in part by price increases. Sales for the most recent quarter totaled $7.38 billion, beating the FactSet analyst consensus of $7.26 billion. Kraft Heinz, with products such as Kool-Aid, Jell-O, real mayo, tarchup, wasabioli and sliced cheese, reported net income of $890 million for the quarter compared to the $257 million loss for the fourth quarter of 2021.

As historically low unemployment and rising wages are helping consumers splurge on traveling while absorbing higher costs for many products, the personal computing industry continues to struggle with excess supply as illustrated by Analog Devices’ earnings release this morning. Sales for the company’s consumer segment dropped 5% y/y during the final three months of 2022, while revenues for communications products climbed 18%. Sales were boosted by strong demand for automation, electrification and automobile products. The company’s total revenue growth of $3.25 billion climbed 21% y/y and exceeded the consensus expectation of $3.15 billion. It expects revenues for the current quarter to reach $3.10 billion to $3.30 billion compared to the consensus expectation of $3.03 billion.

Powell’s team at the Fed has attempted to dominate the field with aggressive rate hikes and balance sheet reduction. Easing financial conditions, however, partly driven by the recent decline in interest rates since November highs, a strong dollar and irrational exuberance on behalf of investors, illustrate that the central bank faces ongoing challenges in dampening demand throughout the economy. With growing expectations of a less dovish Fed and the broad outlook for corporate earnings weakening, bulls this year may find that bears are ready to pounce.

Visit Traders’ Academy to Learn More about Retail Sales and Other Economic Indicators.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.