By: George P. Maris, CFA and Julian McManus

George Maris, Co-Head of Equities – Americas, and Portfolio Manager Julian McManus explain the risk of anchoring investment decisions to the low rates of the past decade.

Key takeaways:

- The recent decline in headline inflation raised hopes of a quick return to low rates and 2% inflation. But structural shifts in the economy could keep both goals out of reach for a while longer.

- In our view, broad equity indices such as the S&P 500® Index do not adequately reflect this possibility, increasing downside risk to passive investors.

- In this environment, we think it is important for investors to carefully consider the value of free cash flows and not expect low rates to drive returns.

For the first month of 2023, equities acted as though the good old days of low inflation and low rates would soon return. Broad measures of inflation were declining, particularly in the U.S., and in January, the Federal Reserve (Fed) slowed its pace of rate hikes to a quarter point, raising hopes that tightening measures could be winding down.

But it didn’t take long for the present to come sharply back into focus. In January, U.S. jobs gains totaled a surprising 517,000, more than double consensus forecasts and pushing the unemployment rate down to a more than 50-year low. Meanwhile, although U.S. inflation dropped from a year-over-year high of 9.1% in mid-2022 to 6.4% in January,1 the Consumer Price Index remains well above the Fed’s 2% target. What’s more, much of the decline can be attributed to disinflation in goods such as oil and used cars – categories that experienced an unusually rapid pace of price increases coming out of the pandemic that could not be sustained indefinitely.

In other words, “the good old days” don’t look to be returning anytime soon. Fed Chairman Jerome Powell acknowledged as much during a panel discussion in Washington, D.C., when he said getting back to a 2% inflation rate “is likely to take quite a bit of time. It’s not going to be smooth. It’s probably going to be bumpy, and we think that we will need to hold policy at a restrictive level for a period of time.”

A bumpy way to 2%

We’d argue some bumps could be caused by structural changes in the economy, and these shifts could keep the 2% goal out of reach for a while. Deglobalization, for example, is adding to manufacturing costs as supply chains get rerouted away from the lowest-cost producers. The greening of the global economy is capital- and commodity-intensive and highly regulated, both inflationary influences. An aging workforce could lead to sustained labor shortages and drive-up wages: Between 2015 and 2050, the percentage of people over 60 will nearly double from 12% to 22% worldwide.2 And a lack of productive investment over the past decade in mining and energy is making raw materials especially vulnerable to supply shocks, contributing to price volatility.

Rather than consider these long-term shifts, markets – for now – are focused instead on headline numbers. As such, with headline inflation retreating, the S&P 500® Index is up 8% so far this year; the Euro STOXX 50 has climbed 12% and the MSCI World IndexSM has returned just over 8%. Bonds also appear relatively optimistic, with the Bloomberg U.S. Treasury Total Return Index up 1.2%.3 Furthermore, rates markets expect the Fed’s benchmark rate to peak in mid-2023 and begin to decline in September. In contrast, during the January/February Federal Open Market Committee meeting, Mr. Powell emphasized it would not be appropriate for the central bank to cut rates this year unless inflation falls drastically in the coming months.

Taking the road less traveled

We caution investors against getting caught up in the herd mentality of the market or anchoring themselves to the conditions of the pre-pandemic economy. The inflationary pressures discussed earlier – and as manifested in the jobs report in January – could supplant the ultra-easy monetary policies of the past decade. Put another way, should commodities get squeezed, labor shortages persist, and manufacturing and operating costs rise because of deglobalization and/or regulation, the Fed and other major central banks may have little choice but to keep rates higher for longer. Such an outcome could potentially slow growth and weigh on corporate earnings (at least in the near term) and will certainly impact equity valuations.

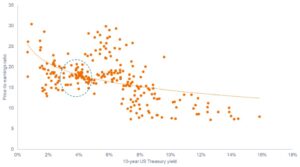

To that point, some indices may now be getting ahead of themselves. As of mid-February, the S&P 500 traded at a price-to-earnings (P/E) ratio of 18.3 based on forward, 12-month estimates for earnings.4 Historically, when the 10-year Treasury yielded 4%, the S&P 500 has a P/E of roughly 16 (see Exhibit 1). With the 10-year now at 3.7%,5 the S&P does not seem like a bargain.

Exhibit 1: Relationship between 10-year U.S. Treasury and S&P 500

Over the long run, a 4% yield on the 10-year Treasury has typically aligned with a P/E of 16 for the S&P 500.

Source: Bloomberg. Regression based on quarterly data from 30 March 1962 to 30 September 2022 of 10-year U.S. Treasury yields and trailing 12-month P/E ratios of S&P 500, which is highly correlated with forward-looking multiples. Price-to-earnings (P/E) ratio is a popular ratio used to value a company’s shares compared to other stocks or a benchmark index. It is calculated by dividing the current share price by its earnings per share.

Investors may get away with paying up for stocks when interest rates are near zero, but that is a riskier proposition at higher yields. As such, in the current environment, we think the price you pay for an asset relative to a company’s ability to generate cash is critical; there is little safety in the crowd.

While indices may not offer safe harbor, we think individual stock opportunities still abound. European banks, for example, have an average forward P/E of 7.6, compared with a 10-year average of 10.9,6 and benefit greatly from rising yields. Asian travel-related businesses, whose stocks came under pressure during China’s zero-COVID policy, carry low valuations and could catch a tailwind from a rebound in travel now that lockdowns are ended.

The list goes on. But importantly, it is a curated list and rooted in the reality of today’s market – not the good old days.

IMPORTANT INFORMATION

Index performance does not reflect the expenses of managing a portfolio as an index is unmanaged and not available for direct investment.

Foreign securities are subject to additional risks including currency fluctuations, political and economic uncertainty, increased volatility, lower liquidity and differing financial and information reporting standards, all of which are magnified in emerging markets.

Financials industries can be significantly affected by extensive government regulation, subject to relatively rapid change due to increasingly blurred distinctions between service segments, and significantly affected by availability and cost of capital funds, changes in interest rates, the rate of corporate and consumer debt defaults, and price competition.

Sources

1 Bureau of Labor Statistics, as of 14 February 2023.

2 World Health Organization, “Ageing and health,” 1 October 2022.

3 Bloomberg. Equity and bond return data are for the year through 13 February 2023.

4 Bloomberg, as of 14 February 2023.

5 U.S. Treasury, as of 13 February 2023.

6 Forward P/E is based on the STOXX 600 Banks Index (EUR) and based on 10-year monthly data through 14 February 2023. The STOXX 600 Banks Index is a capitalization-weighted index which includes European companies that are involved in the bank sector.

—

Originally Posted February 14, 2023 – Investing for today, not the good old days

The opinions and views expressed are as of the date published and are subject to change. They are for information purposes only and should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation to buy, sell or hold any security, investment strategy or market sector. No forecasts can be guaranteed. Opinions and examples are meant as an illustration of broader themes, are not an indication of trading intent and may not reflect the views of others in the organization. It is not intended to indicate or imply that any illustration/example mentioned is now or was ever held in any portfolio. Janus Henderson Group plc through its subsidiaries may manage investment products with a financial interest in securities mentioned herein and any comments should not be construed as a reflection on the past or future profitability. There is no guarantee that the information supplied is accurate, complete, or timely, nor are there any warranties with regards to the results obtained from its use. Past performance does not predict future returns. Investing involves risk, including the possible loss of principal and fluctuation of value.

Janus Henderson Group plc ©

C-0223-48629 02-15-24 TL

Disclosure: Janus Henderson

The opinions and views expressed are as of the date published and are subject to change without notice. They are for information purposes only and should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation to buy, sell or hold any security, investment strategy or market sector. No forecasts can be guaranteed. Opinions and examples are meant as an illustration of broader themes and are not an indication of trading intent. It is not intended to indicate or imply that any illustration/example mentioned is now or was ever held in any portfolio. Janus Henderson Group plc through its subsidiaries may manage investment products with a financial interest in securities mentioned herein and any comments should not be construed as a reflection on the past or future profitability. There is no guarantee that the information supplied is accurate, complete, or timely, nor are there any warranties with regards to the results obtained from its use. Past performance is no guarantee of future results. Investing involves risk, including the possible loss of principal and fluctuation of value.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Janus Henderson and is being posted with its permission. The views expressed in this material are solely those of the author and/or Janus Henderson and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.