The regional banking crisis rolled on with two key developments on Friday. One was the release of several reports detailing the errors that led up to Silicon Valley Bank’s sudden collapse. Poor regulatory oversight combined with an absence of risk management were to blame. The other was the slow collapse of First Republic, which is turning out to be small enough to fail. Founder and executive chair Jim Herbert doesn’t sound as reckless as the team that ran SVB, but their equity looks to be similarly worthless.

Against this backdrop of regulatory failure and a banking system that has been caught out by higher rates, the Fed is about to deliver more of the same next week, taking short-term rates to 5%. December 2024 Fed Funds futures at 3% are priced for a 2% reduction by the end of next year. Reduced appetite for risk among regional banks worries the Fed less than the market.

Inflation’s return to 2% isn’t assured. Nominal GDP rose at 5% in 1Q23. Since real GDP was +1.1%, the price level is rising at a healthy clip. The 1Q23 Employment Cost Index (ECI) rose 1.2% versus 4Q22, and the prior quarter was revised up from 1.0 to 1.1%. We had thought year-end raises would be more reflective of recent inflation, overwhelming the seasonal adjustment, and this looks to have been true. Compensation is up 4.8% year-on-year.

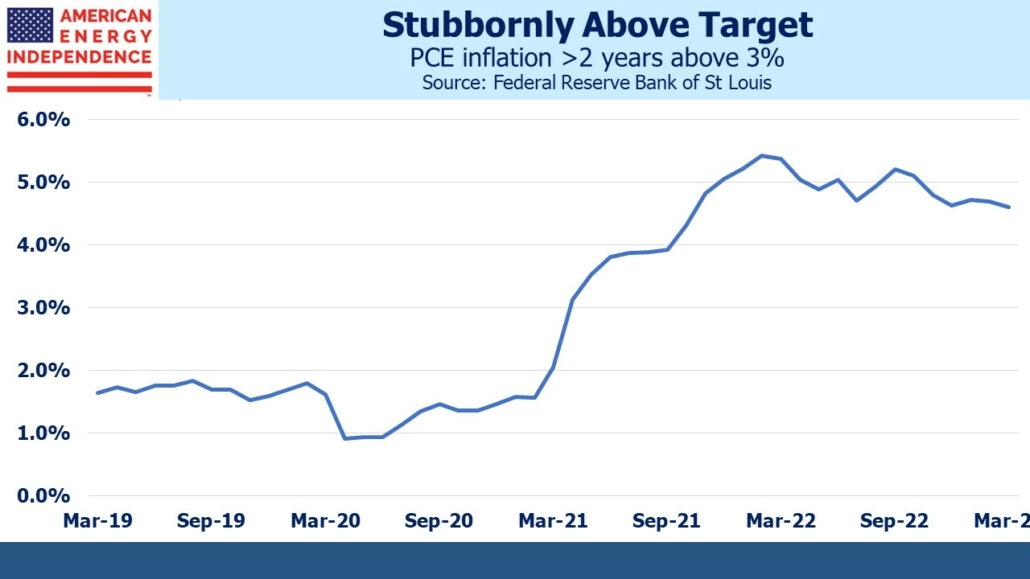

The Fed’s preferred measure of inflation, Personal Consumption Expenditures ex-food and energy (“core PCE”) rose 0.3% month-on-month and is up 4.6% year-on-year. We’ve now experienced two years of inflation above 3% (ie 1% above the Fed’s target). As the ECI figure showed, people are starting to adapt to inflation above 2%.

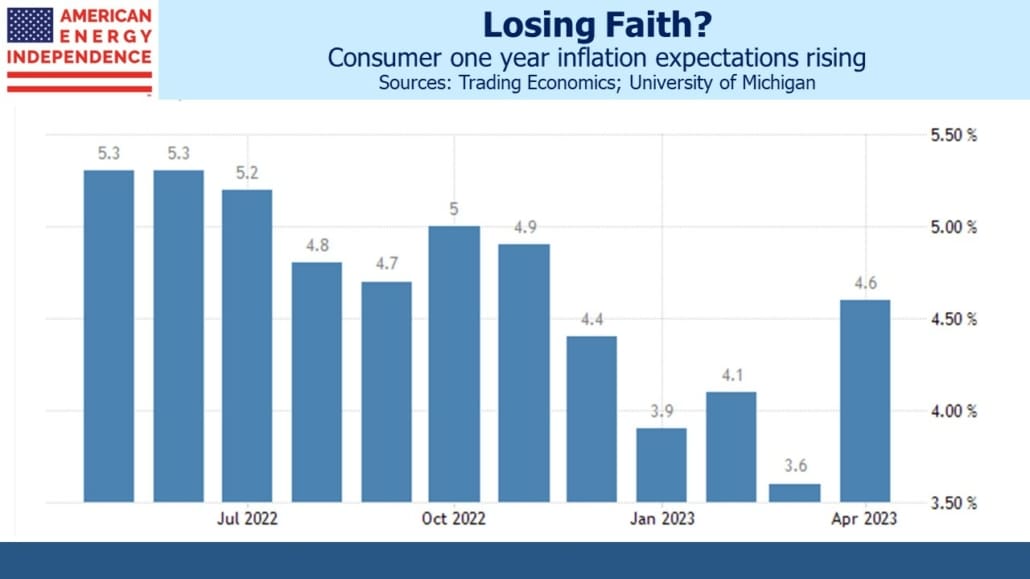

In the University of Michigan survey one year inflation expectations jumped to 4.6% in April, up from 3.6% in March. It’s been rising all year and is the highest since November. It’s hard to justify assuming 2% cost inflation for any big project or for retirement. Long term inflation expectations remain well behaved, but as consumers and businesses manage their affairs for near term inflation of 3% or 4%, it will keep upward pressure on prices.

As 3% becomes the new 2%, the Fed will continue to push back. It’s harder than usual to forecast confidently. The Fed may single mindedly pursue 2% and cause a recession, or the political blowback may force an eventual acceptance of a higher level.

We think midstream energy infrastructure is a good place to be in either scenario.

On April 21 the Federal Energy Regulatory Commission (FERC) reaffirmed prior approval of NextDecade’s proposed LNG export facility at Rio Grande, alongside a deepwater channel within the port of Brownsville, Texas. A Final Investment Decision (FID) should come within a couple of months. Last week their Chairman and CEO Matt Schatzman said, ““We have publicly disclosed that we expect to make it by the end of Q2.”

Building three “trains,” as LNG export facilities are called, is an $11-12BN project. The returns to equity investors will rely on successful execution and also on the mix of debt and equity the company adopts for financing. We still like the stock.

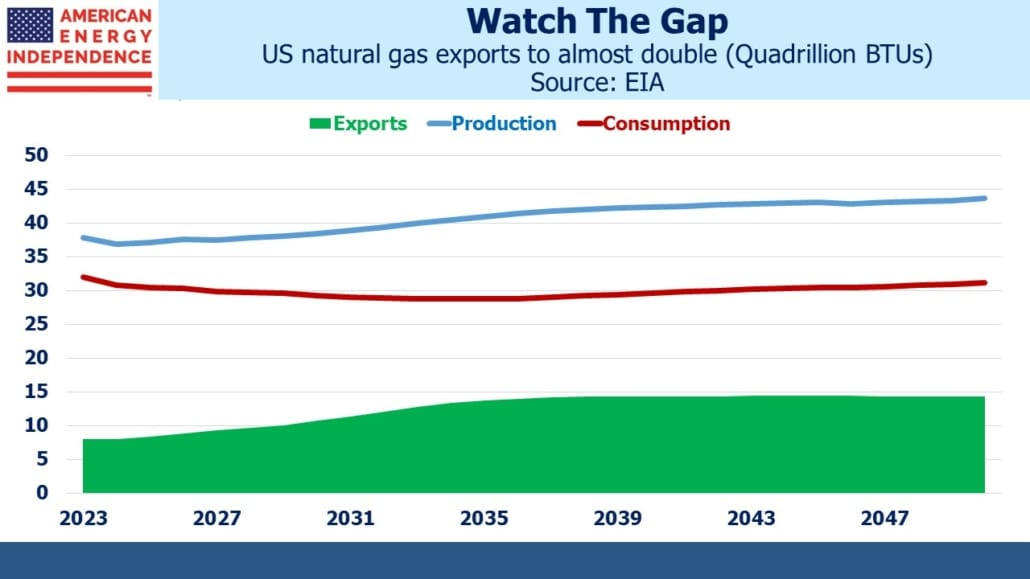

The Energy Information Administration (EIA) expects natural gas consumption to moderate in the years ahead as renewables gain market share in power generation. The need for permitting reform is illustrated by the Mountain Valley Pipeline’s continued failure to complete, held up by legal challenges to permits issued long ago.

Increased output from solar and wind also depends on a predictable approval process for infrastructure to move electricity. Solar and wind need wide open spaces and are generally not close to population centers. The EIA assumes new transmission lines will match increased output. Nobody wants their view sullied with electric pylons, especially if the electricity is merely passing by on its way elsewhere. Environmentalists are not a cohesive bunch, and every project will face objections.

However, even accepting the EIA’s rosy assumptions on vast grid improvements, increasing exports will drive improving economics for the owners of natural gas infrastructure. Russia’s invasion of Ukraine has created long term European demand for natural gas, competing with Asia and other emerging economies.

This outlook doesn’t depend on a defter execution of monetary policy than in the past few years. It does align with the desire of developing nations to consume more energy. If in time 3-4% inflation becomes the new normal, tariff escalators on pipeline tariffs linked to PPI and CPI will enable energy infrastructure to grow cashflows commensurately, if not better.

—

Originally Posted April 30, 2023 – Not Yet Cool Enough

Important Disclosures

The information provided is for informational purposes only and investors should determine for themselves whether a particular service, security or product is suitable for their investment needs. The information contained herein is not complete, may not be current, is subject to change, and is subject to, and qualified in its entirety by, the more complete disclosures, risk factors and other terms that are contained in the disclosure, prospectus, and offering. Certain information herein has been obtained from third party sources and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness or timeliness of this information. Nothing provided on this site constitutes tax advice. Individuals should seek the advice of their own tax advisor for specific information regarding tax consequences of investments. Investments in securities entail risk and are not suitable for all investors. This site is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and do not reflect the deduction of the advisor’s fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase. Indexes and benchmarks may not directly correlate or only partially relate to portfolios managed by SL Advisors as they have different underlying investments and may use different strategies or have different objectives than portfolios managed by SL Advisors (e.g. The Alerian index is a group MLP securities in the oil and gas industries. Portfolios may not include the same investments that are included in the Alerian Index. The S & P Index does not directly relate to investment strategies managed by SL Advisers.)

This site may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involves a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of SL Advisors LLC or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. r

Certain hyperlinks or referenced websites on the Site, if any, are for your convenience and forward you to third parties’ websites, which generally are recognized by their top level domain name. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with SL Advisors LLC with respect to any linked site or its sponsor, unless expressly stated by SL Advisors LLC. Any such information, products or sites have not necessarily been reviewed by SL Advisors LLC and are provided or maintained by third parties over whom SL Advisors LLC exercise no control. SL Advisors LLC expressly disclaim any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.

All investment strategies have the potential for profit or loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

Past performance of the American Energy Independence Index is not indicative of future returns.

Disclosure: SL Advisors

Please go to following link for important legal disclosures: http://sl-advisors.com/legal-disclosure

SL Advisors is invested in all the components of the American Energy Independence Index via the ETF that seeks to track its performance.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from SL Advisors and is being posted with its permission. The views expressed in this material are solely those of the author and/or SL Advisors and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

{kind=link}

{kind=link}

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.