")

Quick read

- With all eyes on inflation, a deceleration in Core Services ex-Shelter prices is a key precondition for the Fed to gain confidence that the Consumer Price Index (CPI) is receding to mandate-consistent levels. Wages are a key input to these prices, but not the only thing to watch.

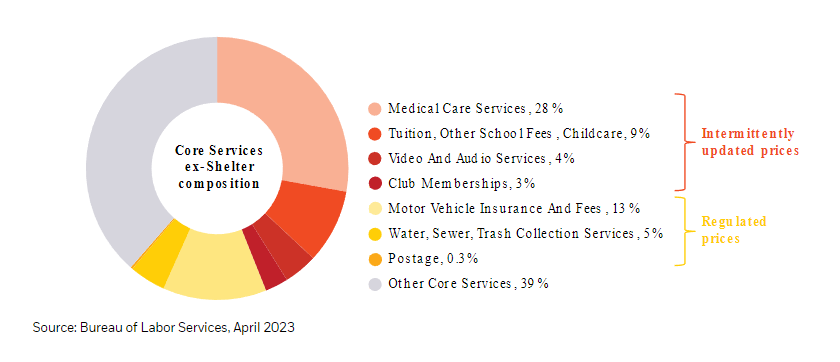

- We are keeping a particularly close eye on two groups of prices that comprise nearly two-thirds of Core Services ex-Shelter CPI: (1) service prices that are regulated (particularly insurance), and (2) services with infrequent price resets (like tuition, medical services, and subscriptions).

- We see upside risks in both of these areas, which contribute to our view that core inflation is likely to remain sufficiently elevated throughout 2023 that monetary policy has no space to loosen in the second half of this year.

Markets remain inflation junkies

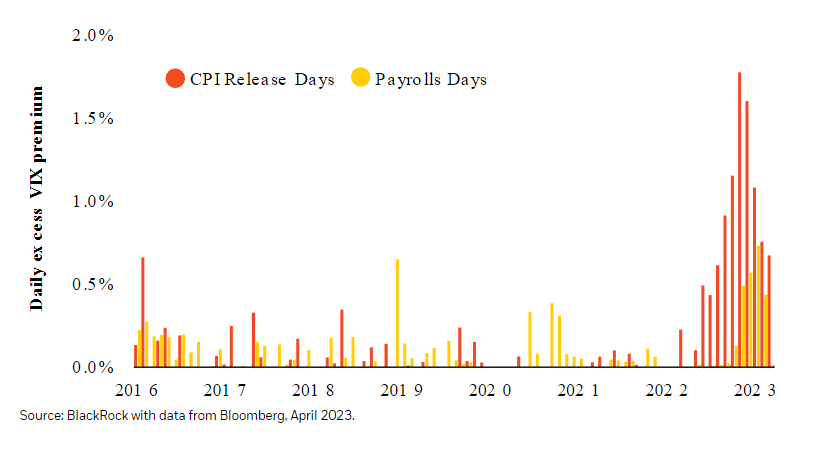

There have been glimmers of hope in 2023 that the inflation fixation of 2022 was a transitory phenomenon. In particular, the market has begun to more closely monitor jobs market data releases to try to spot signs of a labor market and wage slowdown. In the plot below, we try to quantify the relative importance of each part of the Fed’s dual mandate by measuring the expected excess S&P 500 volatility (using daily options data) on release dates for CPI and payrolls. Here we can clearly see that payrolls days have indeed risen in importance relative to 2022. However, the more elevated red bars highlight how inflation remains a key risk to markets. We expect this to remain the case through the summer and see some potential upside risks to the core inflation outlook in the second half of the year.

Heightened volatility on CPI release days demonstrates the importance of inflation on asset markets today

Services prices are sticky prices

Core Services ex-Shelter inflation is a bit of a hodgepodge that includes things like medical care services, video and audio services, tuition, and insurance. It comprises roughly a quarter of the CPI basket and, importantly for the Fed, is very domestically-oriented. It’s been on my mind this week as I contemplate the recent 16% price increase in my NFL Sunday Ticket subscription, and it’s also been on the mind of Jay Powell. In February, he discussed it as follows: “We expect to see that disinflation process will be seen, we hope soon, in the core services ex-housing sector I talked about. We don’t see it yet. It is seven or eight different kinds of services, not all of them the same.”

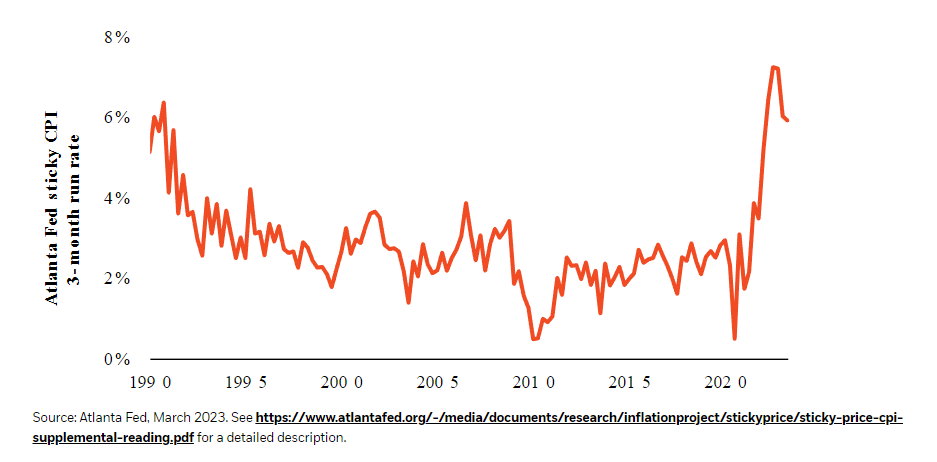

The Atlanta Fed’s “sticky CPI” measure is stuck near multi-decade highs

There is such an extensive amount of economics literature on the stickiness and rigidity of certain types of prices that the Atlanta Federal Reserve Bank publishes its own “sticky CPI” measure which, as shown above, has remained near its highest levels in over thirty years. Services are up-weighted in this index because they are prone to be stickier and tend to experience asymmetric jumps. We are particularly focused on service prices that are regulated and service prices that are infrequently updated – and see upside risks to both.

Core Services ex-Shelter basket weights

Regulation nation

Regulated prices tend to be more discrete and more lagged in their changes due to bureaucratic delays and their negotiated nature. Some types of regulated prices, like postage or water and sewage fees, are easily recognizable as subject to government regulation. Somewhat less intuitive is the degree to which insurance in the United States is a regulated price. Insurance comprises the largest share of Core Services ex-Shelter basket and state-level insurance commissioners play important roles in negotiating auto, property, and casualty insurance price changes.

The underwriting costs of insurance have been surging globally – a combination of higher reinsurance premiums, inflated asset values, and more natural disasters. These rising costs have only just begun to flow through into consumer prices; auto insurance costs were an upside surprise within March’s CPI report.1

Jumps in medical and education prices forthcoming

Though the market has been fixated on the painstaking details of the month-over-month inflation prints, many of the sub-components of the CPI do not update monthly. Two of the more important items within the core services basket – medical care services and tuition – only update their prices annually. Coincidentally, updates for both of these categories take place in the autumn, and both are set to rise strongly.

Medical care services are the largest component (28%) of Core Services ex-Shelter, but have a complex and lagged computation and update only once a year in October.2 Medical services inflation has been negative since last October as a consequence of excess consumer demand for post-pandemic doctors’ visits, however we expect this mechanical effect will abate later this year and thereafter lift core services inflation.

Tuition is another example of a service with intermittent price resets, given prices are set on the basis of the academic year. We expect the broad-based upward wage pressure in education to be passed through to higher education consumer prices later this year when students return to school.

What do these views mean for portfolio positioning?

In general, tactical multi-asset portfolios funds seek to deliver diversifying returns that are lowly correlated with stock and bond markets. They do so primarily by seeking out relative value opportunities across different countries in both stock and government bond markets.

In our view, the importance of inflation for markets is likely to remain elevated throughout 2023. Insights on sticky and persistent services inflation keep us short global duration and short the long-end of the US Treasury curve. Looking around the world, we also see similar core inflation dynamics in Europe and Japan, which leads us to maintain short duration positions in these regions. By contrast, we see opportunity to take long duration positions in certain emerging markets with inflation that is low (like China) or falling (like Brazil).

—

Originally Posted April 27, 2023 – Services inflation is stuck

© 2023 BlackRock, Inc. All rights reserved.

1A recent Bloomberg opinion piece describes the regulatory-driven price setting as follows: “Hiking prices quickly is hard in the US because auto insurers usually must ask state regulators for permission. […] Some insurers are choosing to forgo selling policies until pricing reaches a level they can make money. Several have won approval for 7% hikes in California in recent weeks.”

2The details are documented in detail on the BLS website, but the punchline is that lagged medical insurance industry profitability dictates the innovations for the subsequent calendar year.

Carefully consider the investment objectives, risks, charges and expenses of the funds carefully before investing. The prospectuses and summary prospectuses contain this and other information about the funds and are available, along with information on other BlackRock funds, by calling 800-882-0052 or at blackrock.com. The prospectus and, if available, the summary prospectus should be read carefully before investing.

This information should not be relied upon as research, investment advice, or a recommendation regarding any products, strategies, or any security in particular. This material is strictly for illustrative, educational, or informational purposes and is subject to change.

Prepared by BlackRock Investments, Inc. LLC. Member FINRA

© 2023 BlackRock, Inc. or its affiliates. All Rights Reserved. BLACKROCK is a trademark of BlackRock, Inc. or its affiliates. All other trademarks are those of their respective owners.

USRRMH0423U/S-2863353-4/4

Disclosure: BlackRock

©2022 BlackRock, Inc. All rights reserved. BLACKROCK is a registered trademark of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other marks are the property of their respective owners.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from BlackRock and is being posted with its permission. The views expressed in this material are solely those of the author and/or BlackRock and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.