![[Gamma] Scalping Please](https://ibkrcampus.com/wp-content/smush-webp/2024/04/tir-featured-8-700x394.jpg.webp "[Gamma] Scalping Please")

We recently had the pleasure of speaking with Janelle Teng of Bessemer Venture Partners (BVP). Janelle is a vice president at BVP, focused primarily on cloud software, infrastructure and developer platforms. WisdomTree began working with BVP in 2020 to launch WisdomTree’s Cloud Computing Strategy which tracks the BVP Nasdaq Emerging Cloud Index. This blog is a summary of the key takeaways from the discussion.

The SaaSacre1 of 2022

We had to start by recognising the feeling of our current environment, which comes largely from what BVP has termed the ‘SaaSacre’ of 2022. What is a SaaSacre? If one pulls up the return of the BVP Nasdaq Emerging Cloud Index during 2022 and sees a figure worse than -40%, then they will see it – that drop is the SaaSacre. The market underwent a complete adjustment to valuations across the board, going from peak levels observed in late 2022 to levels much lower reflecting, among other things, a higher general interest rate environment brought on by the US Federal Reserve (Fed). Investors in software-as-a-service (SaaS) companies tended to see an opposite relationship during 2022, where, as interest rates rose, SaaS valuations fell and vice versa2. While it is logical that companies that expect to deliver cash flows far into the future would see their valuations impacted by interest rates, the relationship is not always so stark.

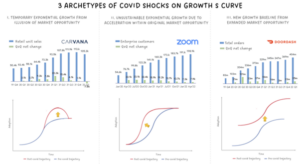

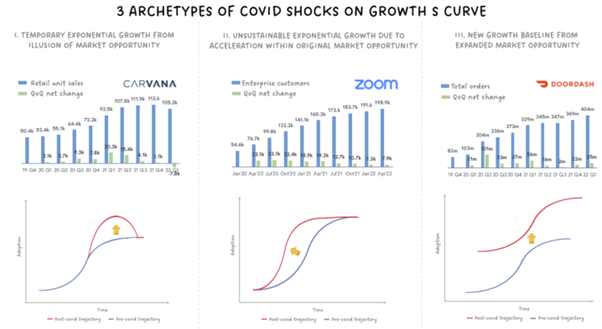

The 3 archetypes of COVID-19 shocks on growth S-curves

The S-curve is a commonly used heuristic to help investors relate time, plotted on the horizontal axis, to adoption, plotted on the vertical axis. A steeper S-curve = faster adoption. An S-curve moved vertically upwards = a larger adoption. The COVID-19 pandemic was a shock that changed the position of the S-curves of various SaaS companies. If we can understand at least a few archetypes of how this occurred, it can help us to better evaluate how companies are doing now, largely on the other side of the shock. We show these examples in Figure 13:

- Temporary exponential growth from illusion of market opportunity: this shock would appear as a bulge upwards in the upper portion of the S-curve—telling us that adoption picked up rapidly for a period of time—before dropping back to the original trend.

- Unsustainable exponential growth due to acceleration within original market opportunity: this shock would appear as a steeper S-curve, with the rising slope pulled further to the left telling us that adoption was occurring suddenly, faster—with the top level peaking at the same place as originally intended, but just arriving there sooner. Many people are familiar with Zoom Video Communications, and this company’s pandemic experience seems to largely be consistent with this archetype.

- New growth baseline from expanded market opportunity: while it may be easy for CEOs to tell us all a story about how they now have a ‘new growth baseline’, it is far more difficult to actually deliver and execute on than it is to say. If there is one area where this happened, it was in food delivery, in that after the pandemic the general person thinks differently about using certain services, be it Uber Eats or DoorDash.

Figure 1: Illustrating the 3 archetypes

Source: https://nextbigteng.substack.com/p/the-reckoning-of-pandemic-tech-darlings.

Historical performance is not an indication of future performance and any investments may go down in value.

The difficulty of making predictions

In thematic topics, it is frequently difficult to make predictions about growth rates and the ultimate sizes of given markets. In the conversation with Janelle, we talked about an example of some forecasts that Gartner had made regarding Worldwide Public Cloud Service Revenues4.

- In April of 2019, the prediction for 2022 was $331 billion.

- In April of 2022, the prediction for 2022 was $495 billion, significantly higher.

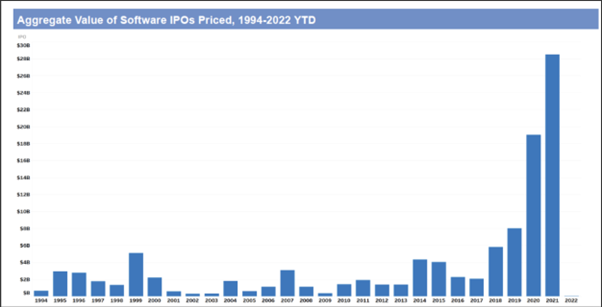

Initial public offerings (IPO’s) and mergers and acquisitions (M&A)

We spent time talking about what we were seeing, or put more accurately weren’t seeing, in 2022, and that was IPOs. A significant benefit of speaking with Janelle and BVP is that there is a sense of history. We can recognise that 2021 was an outlier year, in that the aggregate value of software IPOs priced was in the vicinity of $28 billion. Even without the historic shift in policy at the Fed, Figure 2 shows that matching anything close to 2021’s result was going to be difficult.

Figure 2: 2020 and 2021 were huge years in the software IPO market

Source: https://nextbigteng.substack.com/p/dont-get-ipobliterated-preparing.

Historical performance is not an indication of future performance and any investments may go down in value.

Within the category of corporate actions, sometimes you see M&As (Adobe’s intended purchase of Figma was a big example) and sometimes you see private equity players making investments. So-called ‘take-privates’ in 2022 were extremely active, and we saw many such examples through the year.

Growth vs profitability

One of the questions that we hear often regards what is more important, growth or profitability? In recent years, maybe the real answer is, ‘it depends when you ask.’ It’s very clear that those of us following the software space in 2018 and 2019 saw that growth was of the utmost importance. In 2022, on the other hand, we were hearing a lot more about profitability.

Janelle was able to walk through some work done by BVP within the 2023 State of the Cloud report, the gist of which was, when considering the impact on valuations5:

- November 2021: revenue growth was about six times as impactful on valuations as profitability.

- October 2022: the importance of revenue growth and profitability were roughly equal in their impact on valuations.

- April 2023: revenue growth was about two times as impactful on valuations as profitability.

The true conclusion: It is never all growth and it is never all profitability, but it is important to be aware of how the focus on these measures can ebb and flow across time.

Generative AI is going to be everywhere

Janelle and I spoke the day after Microsoft reported its quarterly earnings for the period ended March 31, 2023. We briefly touched on this quote from Amy Hood, Executive Vice President and Chief Financial Officer6:

“In Azure, we expect revenue growth to be 26% to 27% in constant currency, including roughly 1 point from AI services.”

We can also note this statement from Satya Nadella, CEO7:

“Our Azure OpenAI Service brings together advanced models, including ChatGPT and GPT-4, with the enterprise capabilities of Azure. From Coursera and Grammarly, to Mercedes-Benz and Shell, we now have more than 2,500 Azure OpenAI Service customers, up 10X quarter-over-quarter.”

Janelle and I discussed how the big companies, in this case represented by Microsoft, are important, in that they tell us something about broader enterprise consumption and spending, leading to better clarity on the environment that the more ‘emerging’ cloud companies have to operate within. Microsoft is sending a big signal on generative artificial intelligence (AI), and we believe we will continue to see it spreading across many different companies.

Bottom line: lots of growth catalysts for those with more time

Even if we recognise the uncertainty in the current 2023 economic environment, those investors with a longer time horizon can take advantage, positioning for important growth drivers looking forward. It is rare that companies with the largest market capitalisations in the world are able to announce something that could have a material impact on revenue growth, but that is just what generative AI seems to be as we write these words.

Sources

1 SaaSacre is a term from BVP, combining ‘SaaS’ [software-as-a-service] and massacre, to help illustrate in words the tough performance environment observed in 2022.

2 Source: https://www.bvp.com/atlas/state-of-the-cloud-2023?from=feature

3 Source: https://nextbigteng.substack.com/p/the-reckoning-of-pandemic-tech-darlings

4 Source: https://nextbigteng.substack.com/p/the-reckoning-of-pandemic-tech-darlings

5 Source: https://www.bvp.com/atlas/state-of-the-cloud-2023?from=feature

—

Originally Posted May 24, 2023 – The end of the SaaSacre and the rise of generative AI

Disclosure: WisdomTree Europe

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Please click here for our full disclaimer.

Jurisdictions in the European Economic Area (“EEA”): This content has been provided by WisdomTree Ireland Limited, which is authorised and regulated by the Central Bank of Ireland.

Jurisdictions outside of the EEA: This content has been provided by WisdomTree UK Limited, which is authorised and regulated by the United Kingdom Financial Conduct Authority.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree Europe and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree Europe and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

![[Gamma] Scalping Please](https://ibkrcampus.com/wp-content/smush-webp/2024/04/tir-featured-8-300x169.jpg.webp "[Gamma] Scalping Please")

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.