It is nearly impossible to have a discussion about declining markets without mentioning the “Fed Put.” This is the concept that the Federal Reserve will take actions to support stock prices when they decline. Yet US stock indices entered bear market territory without the Fed lifting a finger to help, leading some to believe that the Fed Put is dead. I will assert that the Fed Put remains alive and well. It’s simply misunderstood. The reality is that it has little to do with equities whatsoever.

For starters, every normal put option has a strike price and an expiration. We can assume that the Fed Put is perpetual, since the central bank is likely to remain vigilant for the foreseeable future, but the strike is a mystery. If you own a put option, you know the level at which it becomes a viable hedge for the underlying asset. Now think about how the Fed has reacted during market crises. They are not changing policies in reaction to minor moves in the stock market. Wherever the Fed Put may be struck, it is clearly at a deep discount to the market.

In a podcast at the beginning of this year, I stated:

“…there’s the concept of “The Fed Put”. I’ve said various times I don’t know where it is struck. You can’t assume it’s struck 2% below the market.”

I stand by that comment even now that we’re down 20%. The Fed has never disclosed that they will intervene if markets fall to a certain level or by a given percentage.

Here’s the real thing – the Fed has never stated that they will intervene in equity markets just because they are down. But they will almost certainly intervene if there is a crisis in credit markets that threatens the banking system or the flow of money. That is a huge difference – a crucial facet that equity investors need to understand.

I was around for the original implementation of the Fed Put. During the Crash of ’87 I was a newly minted graduate of the Salomon Brothers training program. Black Monday was a disaster, but the following day was worse. We started the day with a meeting that warned that the NYSE specialist system was essentially out of capital, which threatened the clearinghouses and major clearing banks. By noon on Tuesday, the equity markets had largely frozen under continued selling. There was no one to absorb it. Keenly aware of the systemic risk that a market crash posed – remember, this now threatened the banking system – the Fed convened conference calls with some of the largest investment banks. After some pow-wows in a smoke-filled office, the head of our equity department said that we should call down to the floor[i], find out what it would take to re-open the stocks that we traded that were offered-only, and place whatever bid was necessary to get them to resume trading – no matter what. When it became clear that Salomon, Goldman Sachs, and Morgan Stanley were all making the same inquiries, other buyers stepped in, some of the selling evaporated, and the market turned around.

It has since become known that the Federal Reserve engineered that turnaround by guaranteeing financing to the firms involved. In other words, the Fed Put. But at that time, stocks were down well over 25% in a two-day period and the risks no were longer contained to the equity market.

Moving forward, the Fed intervened when the excessive leverage of Long-Term Capital Management threatened banks and fixed income markets in 1998 but refrained from meaningful action during the 2000-2002 period until the decline was well underway and a recession loomed. The combination of investor enthusiasm about the internet and Fed liquidity in advance of the feared Y2K problem pushed equities to dizzying heights. Markets peaked as the Fed was withdrawing their Y2K liquidity, and over the ensuing two years the S&P 500 (SPX) fell more than 40%, while the NASDAQ 100 (NDX) shed about 80% from its internet bubble highs. The Fed did begin to cut rates in early 2001, but that was only after plunging stock prices began to affect the broader economy. We saw further rate cuts in late 2001, but those were in response to 9/11, not stocks.

It is said that the Global Financial Crisis of 2008-9 was another use of the Fed Put. OK, but that was first and foremost a banking crisis. A toxic combination of subprime mortgages and dubious financial innovations combined to threaten the world’s financial system. Banks and brokers went out of business, leading to a deflationary spiral that swept equity markets into the maelstrom. Is there any doubt that the massive fiscal and monetary stimulus – a record at the time – was aimed to shore up teetering credit markets rather than rescue equities? Of course, equity indices bounced after falling about 50% just over a year, but that was a welcome side effect of the renewed financial stability brought by those emergency measures.

Since 2008, we have enjoyed over a decade of generally accommodative monetary conditions with quiescent inflation, which proved to be beneficial for equities and other risk assets alike. There were a few times when the Fed attempted to withdraw liquidity from the market – think about the 2013 “Taper Tantrum” and the short bear market at the end of 2018. In both cases, the Fed backed off their actions, but they backed off more quickly in 2013 because those affected bond markets. In 2018 they continued to raise rates even as stocks fell about 25% in the 4th quarter, with the final hike coming in December during the midst of the plunge.

It is important to remember the events of 2019. The Fed Funds rate was cut 25 basis points in each of July, September, and October of that year. Stock markets were doing fine, as was the economy. Instead, repo markets were freezing up. Repos are a critical tool for bank financing, and the Fed was vigilant about making sure that credit markets could function smoothly. The added liquidity certainly boosted stocks, pushing equities to all-time highs that were only interrupted by the pandemic. And does anyone really think that the Fed’s pandemic activities in early 2020 were designed specifically to help stocks rather than to thaw a frozen economy?

It is difficult to pick a precedent for the current stock market environment from among the examples we have discussed, since none of them occurred during an inflationary climate like we see today. Inflation was generally higher in the late ‘80s, but it wasn’t spiking like now. I have frequently noted the similarities between the current trading environment and the late ‘90s/2000 era, while we are presently in the midst of a 2018 style selloff. In either case, the Fed didn’t come riding to the rescue at the first sign of trouble.

Face it – the Fed Put won’t be exercised until or unless we see our stock market malaise metastasize into the credit markets or the economy as a whole. If you’re a fan of the Fed Put, be careful what you wish for.

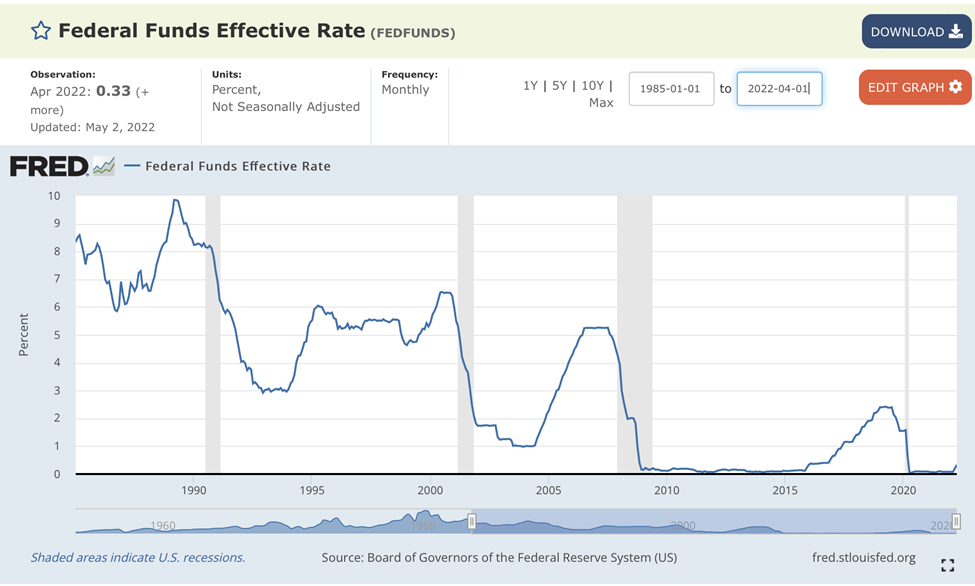

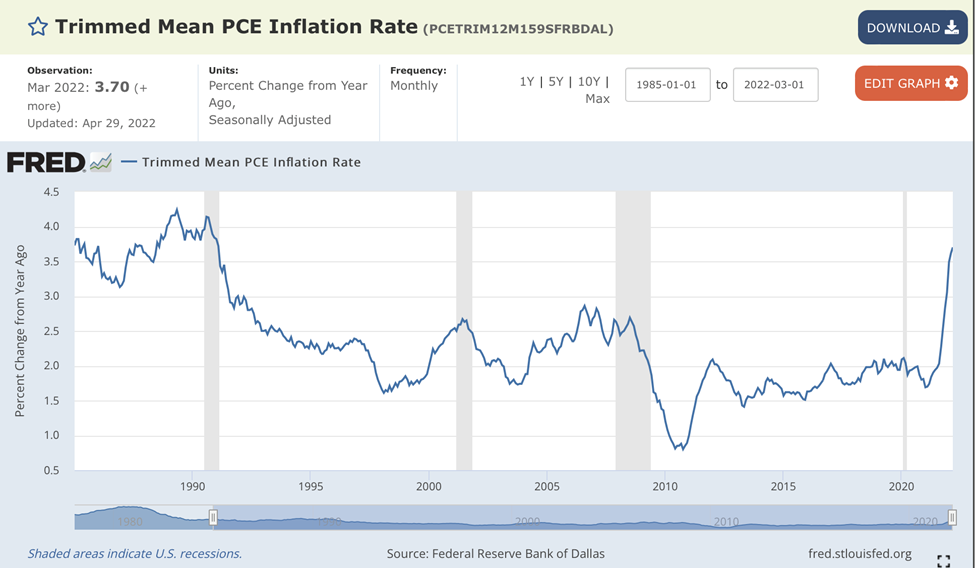

For historical reference:

Source: https://fred.stlouisfed.org/series/FEDFUNDS

Source: https://fred.stlouisfed.org/series/PCETRIM12M159SFRBDAL

—

[i] In those days stock trading was done primarily via phone and face-to-face on an exchange floor

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Options Trading

Options involve risk and are not suitable for all investors. Multiple leg strategies, including spreads, will incur multiple commission charges. For more information read the "Characteristics and Risks of Standardized Options" also known as the options disclosure document (ODD) or visit ibkr.com/occ