The Federal Reserve (the Fed) just can’t get a break. As the economy continues to grow, painful inflation is pervasive and making it unlikely that the central bank will quickly pivot from its monetary tightening that some investors believe could lead to an economic soft landing. The Fed’s preferred inflation gauge, the Core PCE Price Index, climbed 5.1% on a year-over-year basis (y/y) and 0.5% month over month (m/m) in September, almost in-line with market expectations of 5.2% and 0.5% respectively and similar to August’s readings of 4.9% and 0.5%. The general PCE Price Index, which includes food and energy, came in at 6.2% y/y and 0.3% m/m. The Fed’s inflation target on the Core PCE Price Index is 2%, which means that today’s report is more than two and a half times above target. I believe it implies that Fed Chairman Jerome Powell will need to remain an inflation hawk and as his battle against high prices escalates, the likelihood of a recession, rather than a soft landing, increases.

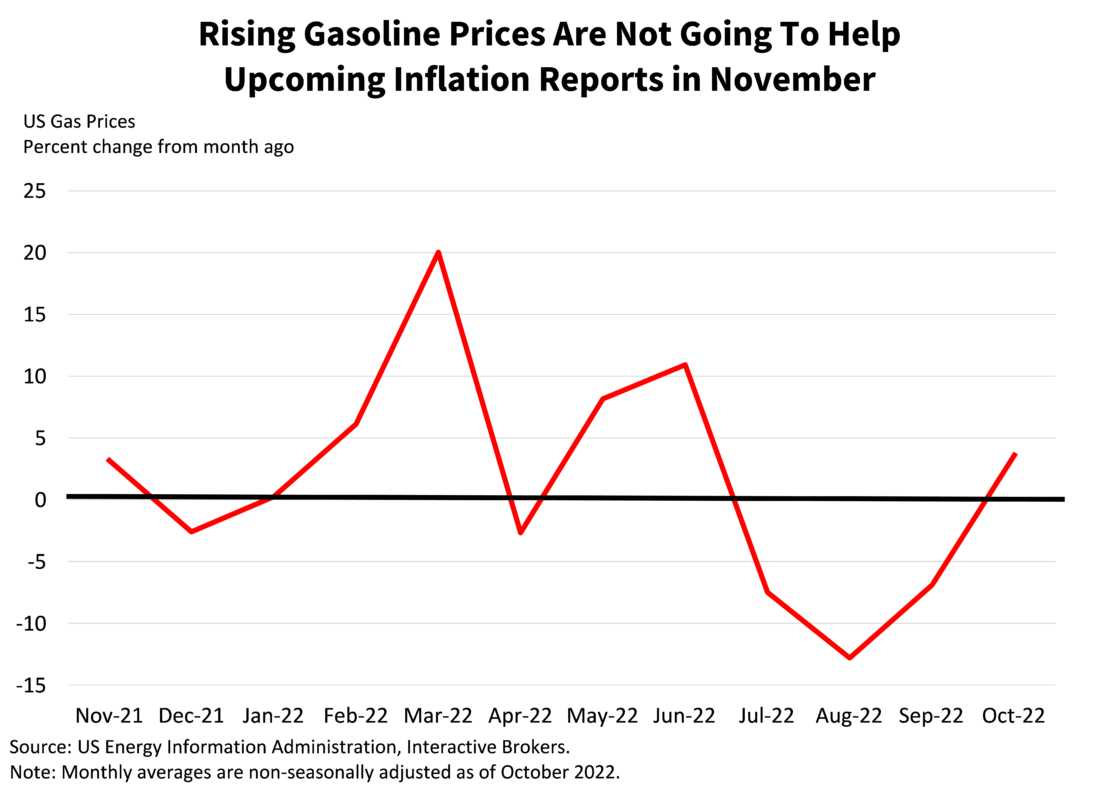

Consistent with the Consumer and Producer Price Indices released earlier this month, today’s report reaffirms that the services industries are driving the bulk of the inflationary pressure, but trouble also exists in the goods sector. While goods prices have declined for three consecutive months, the change has been led entirely by gasoline prices coming down while other categories have stayed high. If you’ve been paying attention at the pump, gasoline prices are up meaningfully in October from September which implies future inflation data could be discouraging. The combination of stubborn inflation in the services sector and goods ex-energy combined with the current increase in gasoline prices is a considerable setback in the Fed’s inflation battle.

Services rose 0.6% from the August level, the same pace as the previous month, with transportation services, housing and utilities, financial services and insurance leading the pack with increases of 2.1%, 0.8% and 0.5%, respectively. Food services and accommodations, other services, health care and recreation services also contributed to gains but at more modest levels. Every major segment in services notched an increase during the period.

Goods fell 0.1% from August, almost entirely due to gasoline and other energy products, which fell 4.6% during the period. Heavy inventory at retailers and slowing consumer spending have led to discounts contributing to a clothing and footwear decline of 0.5% during the month. Every other segment in the goods category notched an increase. In the non-durable goods sub-category, the increases were led by a rise of 0.6% in food and beverages away from home while other non-durable goods contributed to price pressures to a much lesser extent.

In the durable goods sub-category, other durable goods and recreational goods and vehicles notched price gains of 1.7% and 0.5% while motor vehicles and parts and furnishings and household equipment also contributed to gains. Many anticipated that recoveries in supply chain conditions and the pandemic shift in demand from goods to services would reduce the upward pressure on goods prices, but progress has been painfully slow. Supply chains and labor shortages are still worse than they were before the pandemic, and efficiency improvements are being undermined by the partial move from globalization to regionalization.

Personal spending and personal income came in above expectations at 0.6% and 0.4% versus the 0.4% and 0.3% consensus. Spending is outpacing income by a considerable margin once again, and the personal savings rate remains severely depressed at 3.1%, a level last seen during the great financial crisis of 2008. Credit card balances have continued to climb steadily since April 2021 despite higher interest rates weighing on the ability to service this high-interest debt. Consumer sentiment, savings and credit card balances point to a stressed consumer facing the worst affordability dynamics in decades.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.