Yesterday’s trading was all about Nvidia (NVDA) and its eye-popping positive guidance about anticipated spending on artificial intelligence (AI). Today’s winner, in a similar vein, is Marvell Technology (MRVL). They reported decent earnings per share (EPS) after yesterday’s close, $0.31 on a non-GAAP basis, versus a $0.295 consensus[i], but also mentioned that they expect AI revenues to “at least double” in 2024. That’s propelled MRVL +20% higher today.

For the contrarians and natural skeptics among us (including yours truly), it is understandable to question whether AI can live up to the hype that it’s currently receiving. We won’t know the answer for years. But in the meantime, it’s irrelevant. Regardless of whether AI might prove to be earth-shattering, as long as companies are willing to spend money on AI-related technology, then the companies that supply that technology will benefit.

It is well known that the most likely way to profit from a gold rush is to supply the goods and services required by the hopeful miners. In February, on the day after NVDA’s prior earnings report, we noted:

…many investors take a “gold rush” approach. During the California and Klondike gold rushes, selling supplies to prospectors was a safer and smarter to make money than the actual prospecting. It is quite reasonable to think of NVDA as selling picks and shovels, first to the cryptocurrency gold rush, now to the AI gold rush.

Levi Strauss, founder of the eponymous company (LEVI) that still posts profits today, is the best-known example. Since then, we have seen several other gold rushes – literal and figurative – with some of the figurative ones taking place in the same California region that came to prominence in 1849.

NVDA benefitted tremendously from the recent rush into cryptocurrencies before stumbling and once again regaining its footing (and then some!). The verdict is still out about whether blockchain and cryptocurrencies will be a life-changing innovation, but we can look back at an innovation that did indeed prove to be life-changing – the internet.

It is hard to imagine life without the internet now. One can certainly assert that it indeed live up to the late ‘90s hype, even if the enthusiasm for related stocks proved to be wildly overblown. Earlier this week we outlined some of the parallels between the internet craze and the current AI enthusiasm. We’re far from the full-on mania that existed back then, but when we see companies benefit from simply announcing that they are considering AI investments – much as they did when they announced websites in the ‘90s – there are certainly echoes of that era.

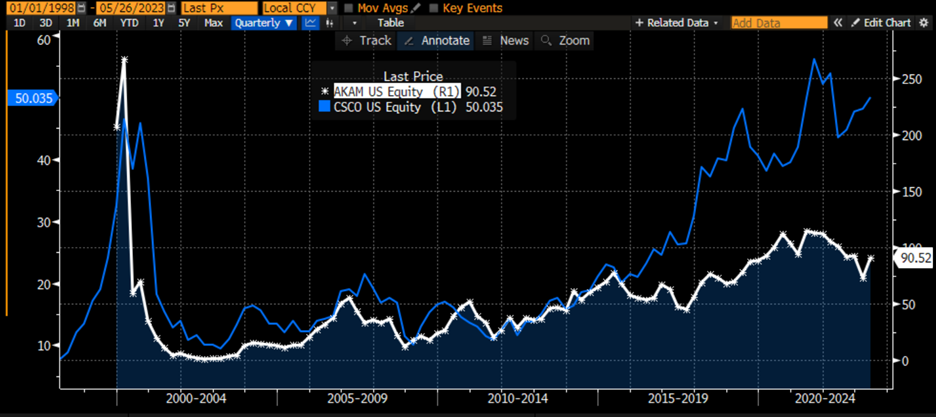

Because that era had its shares of flameouts, some of which seemed sketchy even then (Pets.com, anyone?), there were many who preferred to invest in the companies that would make up the backbone of the internet – that era’s metaphorical picks and shovels. But those too proved to be susceptible to overvaluation as well. Two of the most prominent internet infrastructure companies of that era still trade today. One is Cisco (CSCO), the other is Akamai (AKAM). Both peaked in early 2000. CSCO finally topped its peak about 20 years later, while AKAM still has not:

25+ Years, Monthly Data, AKAM (white), CSCO (blue)

Source: Bloomberg

Oh wait, I almost forgot – Enron was also a huge player in bandwidth back then. For obvious reasons, an up-to-date chart is unavailable.

It is indisputable that NVDA and MRVL, along with others, are benefiting from their role as key providers of chips that will drive AI expenditures. They have been phenomenal investments and are very hard to bet against right now. They can reasonably be considered to be continuing winners if AI remains a key investment thesis. Whether or not they are solid long-term investments remains an open question, however. NVDA and MRVL sport nothing like the premiums attributed to AKAM and CSCO at their peaks, but the latter stocks demonstrate that even during a virtual gold rush it is possible to overpay for the metaphorical picks and shovels.

—

[i] MRVL reported that GAAP EPS was a net loss of -$0.20 on a diluted basis, but who’s counting?

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.

Leave a Reply

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Bitcoin Futures

TRADING IN BITCOIN FUTURES IS ESPECIALLY RISKY AND IS ONLY FOR CLIENTS WITH A HIGH RISK TOLERANCE AND THE FINANCIAL ABILITY TO SUSTAIN LOSSES. More information about the risk of trading Bitcoin products can be found on the IBKR website. If you're new to bitcoin, or futures in general, see Introduction to Bitcoin Futures.

I see a real difference between the INTERNET vs Ai in that the INTERNET did not create anything in of itself; it provided a service/method/tool to bring you somewhere where once there you might do something; ex. go to a website and buy something. Ai is ( in my limited knowledge) giving you something immediately -an answer, information or other supposedly other actions I cannot fully describe. It is in fact doing something for you right then and there rather than merely taking you somewhere to look around and maybe take further steps.

There may come a point where Ai is ‘dismissed,’ ‘downgraded’ in usefulness and cost, but those who walk away may soon find themselves trampled by their faithful..

The benefits we reaped from tech have increasingly gone to maximizing corporate profits and pleasing shareholders over empowering workers and striving for long-term resiliency.

The Keynes beauty contest theory is alive and kicking. Investor’s perception of value causes irrational fluctuations in rational valuation processes. Don’t fight the market, wait it out or run with it.