![[Gamma] Scalping Please](https://ibkrcampus.com/wp-content/smush-webp/2024/04/tir-featured-8-700x394.jpg.webp "[Gamma] Scalping Please")

- With 95% of S&P 500 companies having reported, Q1 2023 earnings season closes with a final growth rate of -2.2%, officially indicating an earnings recession

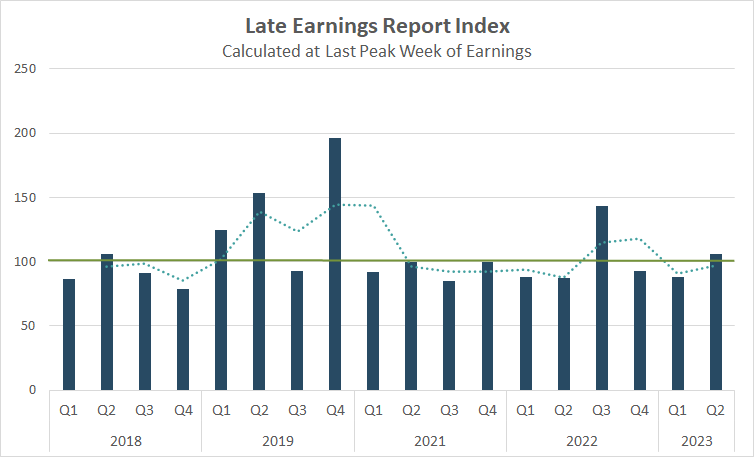

- The post-peak LERI shows corporate uncertainty rose to the highest level in 3 quarters

- Potential earnings surprise this week: New Relic (NEWR)

- Retailers and tech names take us out this week: LOW, NVDA, KSS, ULTA, PANW

- Earnings season winds down, 583 companies expected to report this week

In one of the last heavy weeks for Q1 2023 earnings season, retailers gave investors a better read on the state of the US consumer. Results were a mixed bag, with Walmart emerging as a clear winner last week and Home Depot as a laggard. With 95% of companies having reported at this point, the S&P 500 EPS growth rate for the season ends at -2.2%, officially marking an earnings recession as there have been two consecutive quarters of negative growth.¹

Even with all the action around retail stocks, it was clear investors were more interested in the debt ceiling debate. Stocks marched higher mid-week when the likelihood of resolve was echoed by both President Joe Biden and House Speaker Kevin McCarthy. The three major indexes all closed the week higher on that optimism.

LERI Shows CEO Uncertainty Is at Its Highest Level in 3 Quarters

The uncertainty index which suggested CEOs were feeling more comfortable with how their businesses were performing in the second half of 2022 and first quarter 2023 showed that confidence beginning to waver in Q2 as companies reported their Q1 results.

The Late Earnings Report Index (LERI) tracks outlier earnings date changes among publicly traded companies with market capitalizations of $250M and higher. The LERI has a baseline reading of 100, anything above that indicates companies are feeling uncertain about their current and short-term prospects. A LERI reading under 100 suggests companies feel they have a pretty good crystal ball for the near-term.

The first quarter earnings season (reported in Q2 2023) closed with a LERI of 106, suggesting that companies are more worried than they have been in three quarters. A reading of 106 is the highest since Q2 2022 (Q2 2022 reporting season) came in at 143. The two quarters in between saw below baseline readings of 93 for Q4 2022 and 88 for Q1 2023.

Similarly, The Conference Board released their Measure of CEO Confidence for Q2 on May 4 with much of the same findings. The second quarter reading ticked down 1 point to 42, a reading below 50 suggests “CEO’s remain largely pessimistic about what’s ahead in the economy.”²

Source: Wall Street Horizon

Potential Earnings Surprise this Week? Or Just Acquisition News for New Relic?

New Relic, Inc (NEWR)

Company Confirmed Report Date: Tuesday, May 23, AMC

Projected Report Date (based on historical data): Thursday, May 11

DateBreaks Factor: -3*

For the past eight years, New Relic has reported their fiscal Q4 results between May 8 – 14, on a Tuesday or Thursday. This year they are bucking the trend by releasing results nearly two weeks later on May 23, their latest earnings report date in the 18 years we’ve tracked them. Typically we would point out that academic research shows that companies which delay earnings dates tend to report bad news on their calls, but given recent news on New Relic, this delay could be due to something else.

On Wednesday the Wall Street Journal revealed the enterprise tech company is in talks with private-equity firms Francisco Partners and TPG for a $5B+ acquisition.³ Oftentimes M&A activity causes companies to delay the timing of their earnings reports, as they look to gain more clarity on the potential deal before taking questions from analysts.

So far investors seem keen on the news with the stock closing up 11% on Wednesday.

Last Trickle of Meaningful Q1 2023 Earnings

This more or less concludes the first quarter earnings season with 89% of companies in our universe of ~10k having reported. This week 583 companies are anticipated to release results, 13 of those coming from the S&P 500. Attention will remain on the retail sector with reports expected from: V.F. Corporation (VFC), Lowe’s (LOW), Williams-Sonoma Inc. (WSM), Dick’s Sporting Goods (DKS), Kohl’s (KSS), Ulta (ULTA), Best Buy (BBY), and more. We’ll also get results from a handful of tech names including: Zoom Technologies (ZM), Palo Alto Networks (PANW), New Relic (NEWR), NVIDIA (NVDA), Snowflake (SNOW), Workday (WDAY), and Splunk (SPLK).

Source: Wall Street Horizon

The Q2 earnings season will begin on Friday, July 14 with reports from JPMorgan (JPM), Citigroup (C) and Wells Fargo (WFC).

—

Originally Posted May 22, 2023 – As Q1 2023 Earnings Season Ends, Corporate Uncertainty Hits a 3-Quarter High

¹ https://advantage.factset.com/hubfs

² https://www.conference-board.org

* Wall Street Horizon DateBreaks Factor: statistical measurement of how an earnings date (confirmed or revised) compares to the reporting company’s 5-year trend for the same quarter. Negative means the earnings date is confirmed to be later than historical average while Positive is earlier.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Wall Street Horizon and is being posted with its permission. The views expressed in this material are solely those of the author and/or Wall Street Horizon and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.