![[Gamma] Scalping Please](https://ibkrcampus.com/wp-content/smush-webp/2024/04/tir-featured-8-700x394.jpg.webp "[Gamma] Scalping Please")

Key Takeaways:

- S&P 500 EPS growth for Q3 is set to come in at 1.6%, the lowest level since Q3 2020 and sinking from the prior week due to downward revisions

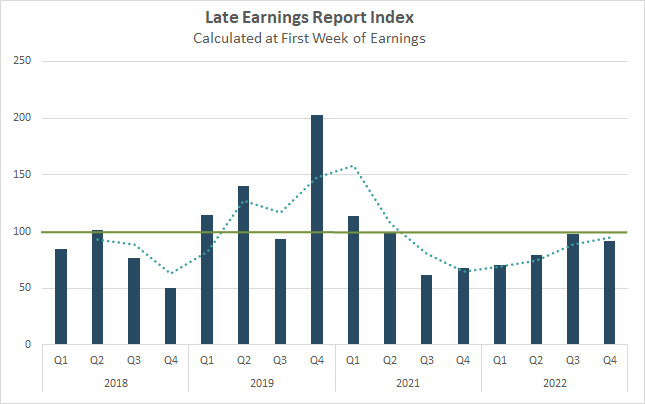

- The LERI improves to 93, better than expected but still showing a downward trend in corporate confidence vs the last 4 quarters

- Names to watch this week include: NFLX, TSLA, IBM

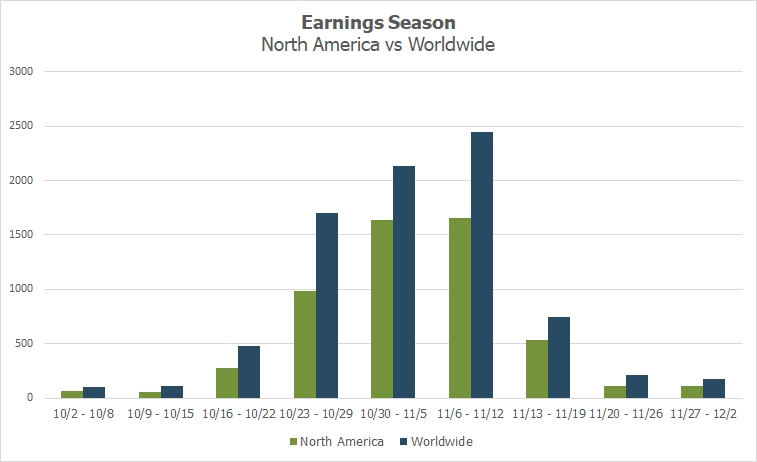

- Peak weeks for Q3 season from October 24 – November 11

Banks Reports are Good Enough to Lift Markets, but Growth Estimates Contract

After disappointments from some early earnings reports out of Delta (DAL), FedEx (FDX) and Bed, Bath & Beyond (BBBY), the banks have somewhat righted the ship again this quarter with results that were not as bad as expected. Higher interest rates helped big lenders such as JPMorgan Chase (JPM), Bank of America (BAC) and Wells Fargo (WFC) surpass top-line estimates, with only WFC missing on the bottom-line. Another bright spot was robust fixed income trading that helped many of the big banks offset declines in equities trading. On the downside, the stagnant M&A and IPO market led to a year-over-year (YoY) decline in investment banking revenues, while an increase in reserves for loan loss provisions signaled that banks were preparing for a less certain economic climate ahead.

The S&P 500 EPS growth rate, which tends to increase as more companies report, actually showed a decrease over the last week, falling to 1.6% on October 14 from 2.4% on October 7 (Data from FactSet). The decline came as more Wall Street analysts lowered estimates for the remainder of the season. This would be the lowest result since Q3 2020 posted negative growth of -5.7%.

LERI Shows Companies are Not as Uncertain in the Short-Term

Our proprietary Late Earnings Report Index is also signaling that while the corporate profit landscape isn’t great, it’s not terrible yet either.

The LERI looks at the number of outlier earnings date confirmations and whether companies are confirming earnings dates that are later than they have historically reported, or earlier. A reading above 100 reflects that companies are confirming later earnings announcements and below this average indicates companies are confirming dates that are earlier.

Thus far we see a LERI of 93 for the Q3 season, lower than last quarter’s reading at this point in time, but higher than what we saw for the first quarter earnings season. This suggests that while corporate confidence is contracting, it hasn’t completely collapsed. There are still more companies delaying earnings (40) than advancing them (38), with a total number of 1,036 confirmations that significantly deviate from historical norms, amongst companies with market caps over $250M.

Source: Wall Street Horizon

More Financials, Airlines and Tech in Focus this Week

While peak earnings season doesn’t officially begin until next week, we still have some notable names reporting this week from Financials, Airlines, and Tech. Closely followed names such as Netflix (Reports Tuesday, Oct 18 AMC), Tesla and IBM (Report Wednesday, Oct 19 AMC) will be in focus.

Source: Wall Street Horizon

Q3 2022 Earnings Wave – Peak Season Begins Next Week

This season peak weeks will fall between October 24 – November 11, with November 3 predicted to be the most active day with 964 companies anticipated to report. Only 48% of companies have confirmed at this point (out of our universe of 10,000 global names), so this is subject to change. The remaining dates are estimated based on historical reporting data.

Source: Wall Street Horizon

—

Originally Posted October 18, 2022 – Banks Report Better Than Expected, but Overall Q3 Growth Worsens

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Wall Street Horizon and is being posted with its permission. The views expressed in this material are solely those of the author and/or Wall Street Horizon and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

![[Gamma] Scalping Please](https://ibkrcampus.com/wp-content/smush-webp/2024/04/tir-featured-8-300x169.jpg.webp "[Gamma] Scalping Please")