“A new clean energy economy is emerging, and it is emerging much faster than many stakeholders, policymakers, industry players, and investors think today” – Fatih Birol, Executive Director, IEA during the Global EV Outlook 2023 press event on 26 April 2023.

The International Energy Agency (IEA) published its Global Electric Vehicle Outlook for 2023 on 26 April. Its assessment of the state of the industry is encouraging and its projections for the industry’s growth are exciting. Electrification of road transportation is the disruptive innovation the industry has been waiting for. It appears that the tipping point has been reached.

Highlights from 2022, and developments in 2023

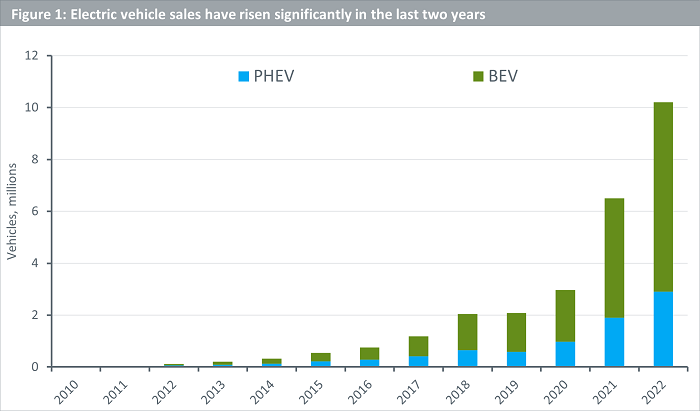

Electric vehicle (EV) sales exceeded 10 million in 2022 (see Figure 1). This amounts to 14% of all new cars sold in 2022, up from 9% in 2021, and less than 5% in 2020. This trend has continued at the start of 2023 with over 2.3m EVs sold in the first quarter, 25% more than the same period last year. By the end of the year, sales could hit 14 million with an acceleration expected in the second half of the year1.

China remains the dominant market, accounting for around 60% of global electric car sales last year, with Europe and the United States following behind. Nonetheless, there are promising signs of growth in emerging markets such as India, Thailand, and Indonesia where sales of electric cars last year more than tripled compared to 2021.

Source: International Energy Agency, April 2023. BEVs are battery electric vehicles. PHEVs are plug-in hybrid electric vehicles.

Historical performance is not an indication of future performance and any investments may go down in value.

The key tailwinds

Policy support for the adoption of electric vehicles has never been stronger and it continues to strengthen. The European Union has set out CO2 standards for cars and vans aligned with 2030 goals set out in the Fit for 55 package. In the US, the Inflation Reduction Act (IRA), and California’s Advanced Clean Cars II rule could accelerate the journey to 50% EV market share by 20302.

Given strong support from policymakers and adoption from consumers, innovation in battery manufacturing also appears to have been catalysed. While it is a given that battery chemistries will continue to evolve and greater levels of efficiency will be achieved, developments along the way, such as CATL’s recent condensed battery launch, are noteworthy and encouraging.

On 19 April 2023, the Chinese battery manufacturer CATL, among the biggest names in the industry worldwide, unveiled a high-energy density, so-called ‘condensed battery’ at Auto Shanghai. CATL claims that this battery could not only meaningfully increase the range of EV batteries but could also help electrify passenger aircraft. Admittedly, there are multiple unknowns in CATL’s claims, including costs and delivery times, but it highlights how battery manufacturers are focused on achieving new degrees of efficiency.

Growing competition and, therefore, more choice for consumers is also facilitating the adoption of EVs. The number of electric car models worldwide exceeded 500 in 2022, more than double compared to 20183. While this is still significantly lower than the number of internal combustion engine (ICE) models on the market, this proliferation of models is increasing competition among original equipment manufacturers (OEMs) which should help bring costs down.

Electrification, however, is going beyond passenger cars. In 2022, over half of India’s three-wheeler registrations were electric. Similarly, electric light commercial vehicle sales worldwide increased by more than 90% in 2022 compared to the year before4. Such encouraging growth is also being witnessed in other market segments like electric heavy-duty trucks and buses.

The forecast

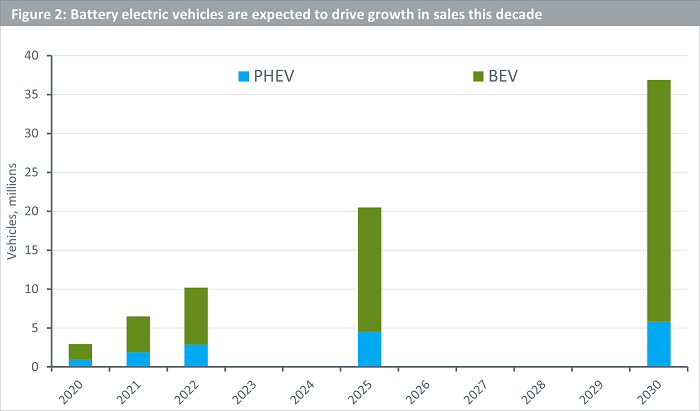

Even in the IEA’s stated policies scenario (STEPS – a conservative scenario which only factors in existing policies), growth of electric vehicles is expected to be strong this decade (see Figure 2). Across the globe, countries are swiftly introducing bans on the sale of new ICE vehicles. Some countries, like Norway, have taken the lead by making this ban effective from 2025. For many other countries, the bans come into effect between 2030 and 2040. Collectively, therefore, it is reasonable to expect a meaningful uptick in EV sales as we progress towards those deadlines.

Source: International Energy Agency, April 2023. BEVs are battery electric vehicles. PHEVs are plug-in hybrid electric vehicles. Data is for the world in the ‘Stated Policies Scenario (STEPS)’.

Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

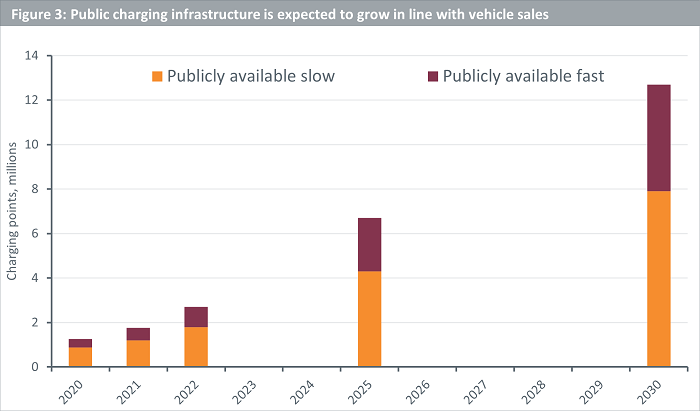

One of the biggest hurdles in EV adoption is the availability of ample public charging infrastructure. Fortunately, charging infrastructure is developing quickly, albeit at different rates in different countries. Overall, however, the IEA have an optimistic view on the number of publicly available charging points worldwide by 2030.

Source: International Energy Agency, April 2023. BEVs are battery electric vehicles. PHEVs are plug-in hybrid electric vehicles. Data is for the world in the ‘Stated Policies Scenario (STEPS)’.

Forecasts are not an indicator of future performance and any investments are subject to risks and uncertainties.

A renewed focus on the supply chain

According to the IEA, automotive lithium-ion (Li-ion) battery demand increased by about 65% to 550 gigawatt hours (GWh) in 2022, from about 330 GWh in 2021, primarily because of growth in electric passenger car sales. In 2022, about 60% of lithium, 30% of cobalt, and 10% of nickel demand was for EV batteries. Only five years prior, these shares were around 15%, 10% and 2%, respectively.

Electric vehicles are not only driving demand for batteries, but also the underlying commodities. For investors, this means a holistic view of automotive and battery value chains is warranted when considering the electrification megatrend. For example, China holds a dominant position in both value chains and its role in terms of where it sits within the value chain is evolving rapidly. China is the biggest manufacturer of batteries worldwide but is also quickly establishing itself in the segment of car companies (OEMs) with the emergence of brands like BYD.

But as competition increases, more regulation is introduced, and further innovation happens, supply chains will develop. Some links may get broken while others get formed. All in all, an exciting time to be following this space.

Sources

1 International Energy Agency Global EV Outlook 2023.

2 International Energy Agency Global EV Outlook 2023.

3 International Energy Agency Global EV Outlook 2023.

4 International Energy Agency Global EV Outlook 2023.

Originally Posted June 1, 2023 – IEA’s bullish outlook for electric vehicles and what it means for investors

Disclosure: WisdomTree Europe

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Please click here for our full disclaimer.

Jurisdictions in the European Economic Area (“EEA”): This content has been provided by WisdomTree Ireland Limited, which is authorised and regulated by the Central Bank of Ireland.

Jurisdictions outside of the EEA: This content has been provided by WisdomTree UK Limited, which is authorised and regulated by the United Kingdom Financial Conduct Authority.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree Europe and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree Europe and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.