![[Gamma] Scalping Please](https://ibkrcampus.com/wp-content/smush-webp/2024/04/tir-featured-8-700x394.jpg.webp "[Gamma] Scalping Please")

There are some core principles that are supposed to govern investing. If I were to ask you to come up with the most important one of those principles off the top of your head, there is a pretty good chance you would tell me that to get a better return you need to take more risk. And in my experience, that principle is a very good one and does hold the majority of the time.

But there is one key area of factor investing where it doesn’t. That outlier is the low volatility factor.

One would expect that buying less volatile stocks would lead to a lower return. But the research is very compelling that it doesn’t. While it is rare for there to be any free lunches in investing, low volatility does appear to be one of them.

Before we get into why that is, it is probably best to first define what the factor is.

What is Low Volatility?

Defining low volatility is probably the easiest of all the factors we follow. Value can be challenging to define because there are a lot of value metrics. Quality is even worse and everyone seems to have a different definition for it. But low volatility is just about buying stocks that are the least volatile. There are two major metrics that are typically used. The first is standard deviation, which measures the standalone volatility of any asset. The second is beta, which takes into account how the asset moves relative to the market in addition to its own volatility.

By the way, one thing to keep in mind when you look at investment strategies in this area is that there is a significant difference between low volatility and minimum volatility. Low volatility focuses on the volatility of the individual assets you are purchasing. Minimum volatility is a portfolio level concept that focuses on keeping the volatility of the overall portfolio low. There is certainly some overlap between the concepts, but it is important to keep in mind that they are different things when you see funds and ETFs that deploy the two strategies.

Does Low Volatility Work?

I think the clear answer this this question based on the academic research is yes.

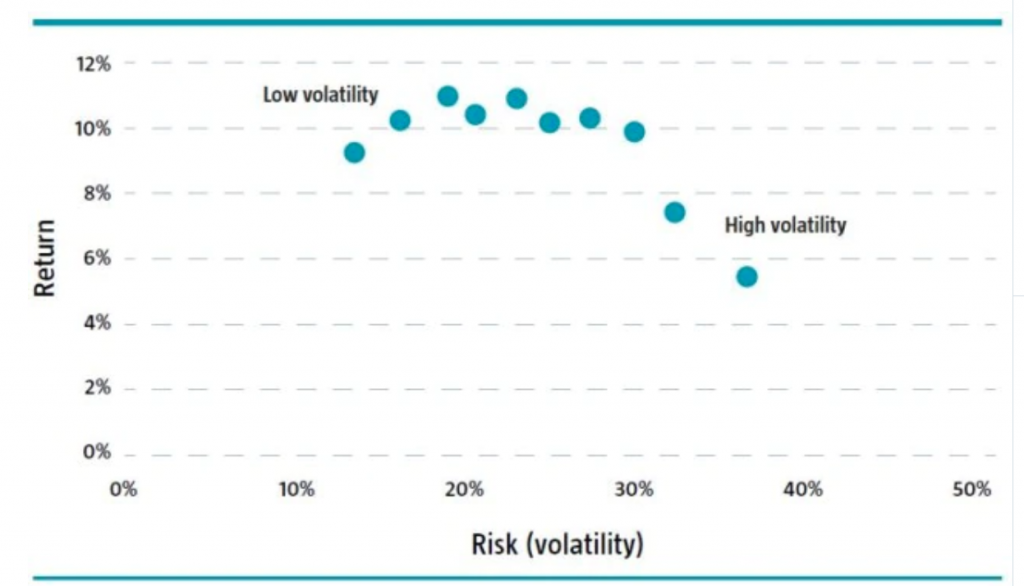

This chart from Robeco does an excellent job of showing the relationship between return and volatility. You would expect that as volatility increases, return would too, but that is not what the data shows.

https://www.robeco.com/au/key-strengths/quant-investing/glossary/low-volatility-factor.html

We were able to interview Robeco’s Pim van Vliet, who is one of the world’s leading experts in low volatility, for our podcast Excess Returns. If you want to dig deeper into low volatility, I highly recommend you check it out as Pim can explain these concepts much better than I can.

Why Does Low Volatility Work?

Factors typically work for two different reasons. Either they produce an excess return by taking on more risk or they capitalize on the behavior of other investors that leads to a mispricing. With low volatility, using the risk-based framework doesn’t lead to very satisfying results since by definition the factor is selecting lower risk stocks. Low volatility is certainly prone to periods of underperformance just like the other factors, but using a standard risk framework, it is difficult to explain why the factor works.

That leaves us with the behavioral based explanation. But that can be challenging with low volatility as well. With value and momentum, the behavioral explanations are more intuitive, but in this case, you have to dig a little bit deeper to come up with one. The best explanation I have heard is that investors who cannot use leverage need a mechanism to boost their returns. As a result, they seek out higher volatility stocks as a means to do that and thus create a situation where they are overpriced relative to their low volatility counterparts. This creates a relative opportunity.

Low Volatility and Other Factors

Even if you are skeptical about low volatility, the good news is that it doesn’t need to be used on its own to be effective. In fact, research has shown that using low volatility with other factors enhances its long-term return without a major impact on its risk reducing benefits.

Robeco and other researchers have found that both value and momentum can enhance a low volatility strategy. In Pim van Vliet’s paper “Enhancing a low-volatility strategy is particularly helpful when generic low volatility is expensive”, he found that when low volatility is cheap, it outperforms the market by 2.2% per year, but when it is expensive, it underperforms by 1.4% (although it still outperformed on a risk-adjusted basis). In his paper “The Conservative Formula: Quantitative Investing made Easy”, he also found that coupling low volatility with price momentum and high net payout yields produces enhanced returns. The formula produced a 15.1% annualized return since 1929, which was well in excess of the market return.

Challenges to Low Volatility

The biggest challenge I have seen to low volatility is not that it doesn’t work, but rather that its success can be explained by other factors. For example, Larry Swedroe has talked about how the majority of the excess returns from low volatility comes from when the stocks are cheap. Or in other words, a lot of low volatility’s success can be explained by periods where low volatility stocks were also value stocks.

And if you couple value with profitability or quality, the result gets even more compelling, as some research has shown that combination explains effectively all the returns of low volatility.

Larry wrote an excellent article where you can find more details on these arguments.

The Factor That Shouldn’t Work

There are many skeptics about low volatility because the logic behind it seems to challenge the core investing belief that increasing returns should require taking on more risk. I can understand these arguments because I have been one of these skeptics myself. But in the end, there is strong evidence to support the factor. The evidence may not rise to the level of the evidence supporting value or momentum, but it is still hard to refute. Even if the risk of low volatility doesn’t show up in standard risk metrics, though, it still exists and the factor can go through extended periods where it doesn’t work just like all the other factors. But for investors who want to focus on reducing volatility in their portfolio, the factor is certainly worthy of consideration.

—

Originally Posted March 8, 2023 –The Surprising Investment Factor That Defies the Risk-Return Tradeoff

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Validea Capital Management and is being posted with its permission. The views expressed in this material are solely those of the author and/or Validea Capital Management and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: ETFs

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Complex or Leveraged Exchange-Traded Products

Complex or Leveraged Exchange-Traded Products are complicated instruments that should only be used by sophisticated investors who fully understand the terms, investment strategy, and risks associated with the products. Learn more about the risks here: https://gdcdyn.interactivebrokers.com/Universal/servlet/Registration_v2.formSampleView?formdb=4155