There is a tendency to avoid looking at your finances and investments when things are bad, so I am guessing there isn’t going to be mad rush to open year-end brokerage statements this year. That’s understandable, since investors feel losses twice as much as they value gains. Why ruin this holiday season by looking at how much you’re down over the past year. But rather than dwell on the past, it’s more important is to implement discipline and consistency to your financial plan and investment approach — and what better time to do it than at the end of the year.

Here are six year-end moves to consider to help as you look to grow and optimize your wealth, financial and personal health going forward.

Inventory Your Investments & Returns

For many investors, the first step is super simple. Create an investment inventory list of the following:

- Where are your investments and what is the value?

- What do you hold/own?

- What percentage are you in stocks and bonds?

- How have your investments fared over the last year (and few years – if you can get this information.)

This is as simple as logging into your accounts and pulling down your account values as of the end of the year. You can capture this in a spreadsheet or even use account aggregation tools like Intuit’s Mint that allow you view all your accounts under one roof. Get it organized, and know what you own and where you fall on the stock vs. bond scale.

Many online brokerages or 401K account providers offer you to the ability to look at your past performance. Some go back a year, while others offer longer periods of time. When looking at your returns, you always want to look at the longest period possible to assess how your investments have fared. You should be able to compare this to the overall market to see how much deviation (positive or negative) you’d had over time.

Some investors may use the performance to make changes in their allocations / holdings. This may not be optimal from a long-term performance standpoint since we tend to weight recent performance more and behavioral biases come into play. However, by assessing the performance relative to the market or other benchmarks, you may be able to get a sense of the risk exposures you have, whether or not active or passive funds should be at the center of your approach and if you are on track to meet your goals with your current investment portfolio and the expected future returns you may be able to generate.

The Rebalancing Effect

In past years when the stock market has gone into bear market territory, investors were usually presented with an opportunity to rebalance their portfolios by taking money from areas that held up better (i.e., bonds) to re-allocate back into stocks. But in 2022, stocks and bonds both fell simultaneously, and by a lot. An investor in a 50-50 stock and bond portfolio at the start of the year is probably right around the target threshold of 50-50 today. But there are still rebalancing considerations for investors. For example, if you strongly believe we’re in a prolonged period of high inflation, it could make sense to seek out inflation fighting asset classes like commodities. Another example may be bonds – with the short-term bonds yielding over 4% some conservative investors may consider rebalancing out of high dividend paying stocks, which they were invested in for the income, and into short-term fixed income now that yields are significantly higher than they were at the start of the year.

Tax Loss Harvesting

Losses are never fun, but for investors with taxable investment accounts harvesting (i.e. selling) losing positions is one way to book losses now to help set up gains in future years. One of the tricky things with harvesting losses is what to do with the excess cash from the sales of the proceeds. One option is to sit on the cash and re-deploy after 30 days into the same names you sold (so you avoid the wash sale rule) but you risk missing out if stocks move higher. Buying the broader market through a low-cost ETF or buying ETFs that give you exposures similar to what you previously held are other options. Whatever you do, tax loss harvesting can help manage tax labilities in the future so it’s worth looking at what you can harvest today for the benefits of tomorrow.

RMD Updates

Investors required to take required minimum distributions from IRAs need to make sure they get those in before 12/31 to avoid any penalties.

Furthermore, the SECURE Act of 2020 changed a number of things with required minimum distributions. If you turned 70 ½ in 2020 or later, you must take your first RMD by April 1 of the year after you reach72 (vs. the year an individual turned 70.5). The other big change came to inherited (or beneficiary) IRAs for non-spouse account holders. For non-spouses that inherited IRAs after Jan. 1st, 2020, account holders are required to distribute the full balance of their account by December 31 of the 10th year following the original IRA owner’s death. These changes can be tough to follow for some so it’s best to consult your accountant or financial advisor.

Consider Trend Following, Not Market Timing

During bear markets it’s inevitable that some investors will engage in market timing: selling out of the market in an attempt to try to sidestep the worst of a market decline while maintaining a belief they can get back at lower prices. It’s not impossible, but usually this detracts from returns over time. Those investors with cash on the sidelines may be better served by using trend following signals to get back into stocks vs. using headlines and hunches. This way, you take the emotion out of the decision and you’re not frozen in your decision making, which can happen to many investors.

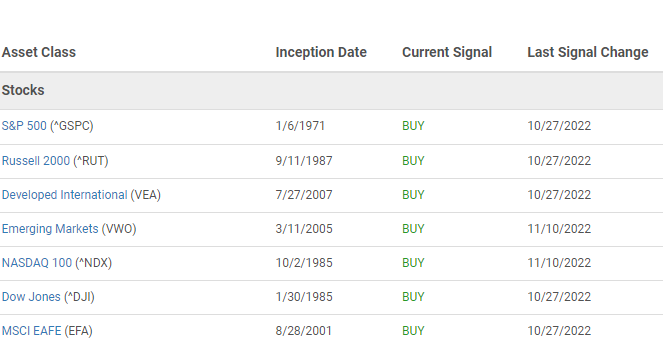

In late October and early November, the most of the major equity indices went into “buy” status using Validea’s Trend Following system. This could be a good tool to reference for those looking to get back in with long-term money allocated to stocks.

Being Open to Different Ideas

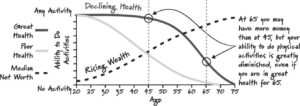

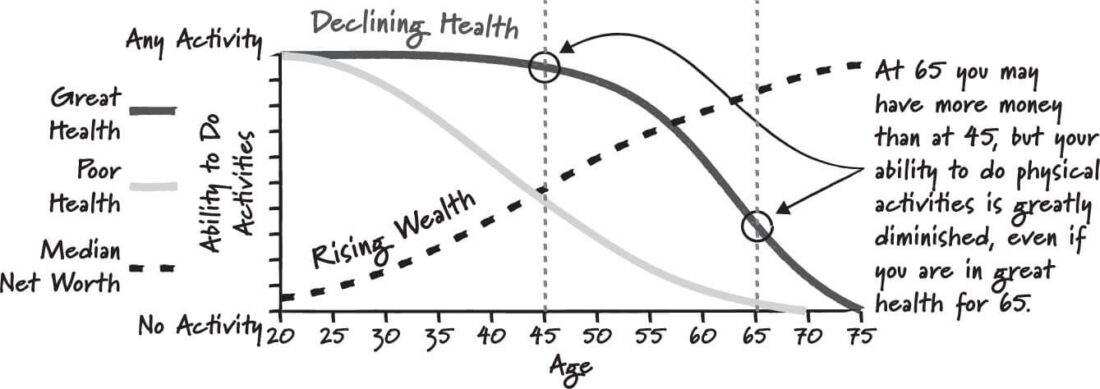

I have a tendency read and seek out others who I largely agree or identify with. But that is why I was interested in reading a new book, “Die With Zero,” on the recommendation of a young blogger I follow. The central idea book is to maximize net fulfillment throughout life with experiences vs. maximizing net worth. The author makes the point that we spend our life savings and focused on maximizing our wealth but as we get older and later on in life, we have less time, energy and good health to enjoy that wealth through experiences. This idea of spending on experiences and memories now and accumulating less is not something that feels totally natural to me but the chart below really jumped out because I am right at the age where as humans we start the steady decline, albeit slow at first, in health and I also have two children whose time with us won’t be forever. The book has helped open my mind to a different way to think about savings and experiences.

These are just a few ideas that jump out at me. If you have other year-end ideas, feel free to reach out and share them.

—

Originally Posted December 7, 2022 – Six Year-End Financial Moves to Consider

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Validea Capital Management and is being posted with its permission. The views expressed in this material are solely those of the author and/or Validea Capital Management and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.