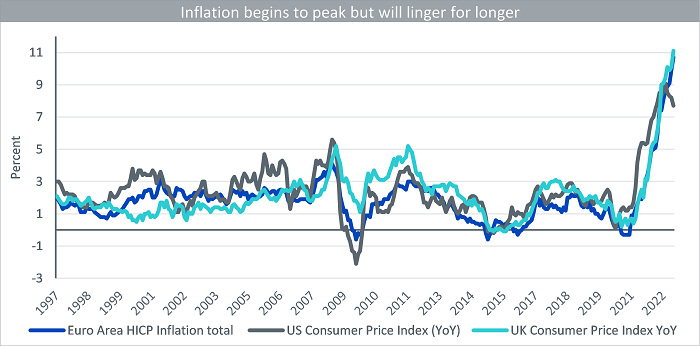

This week the UK economy posted its highest inflation reading in 41 years rising 11.1% year on year (yoy) in October. The recent jump is largely the result of the uprating of the household energy price cap in October. Core inflation moved sideways at 6.5% yoy. We expect this to represent the peak for UK inflation. As the base effects of high energy prices begin to factor in, headline inflation in the UK is likely to fall. At the same time, the ongoing recession is likely to strip away the underlying price pressures. This has been evident in lacklustre consumer demand alongside waning housing market activity.

Source: Bloomberg, WisdomTree as of 31 October 2022.

Please note: HICP is the Harmonised Index of Consumer Prices used to measure consumer price inflation.

Historical performance is not an indication of future performance and any investments may go down in value

UK Government claws back its credibility with the Autumn Statement

Meanwhile the UK Government’s fiscal statement released this week1, confirmed significant fiscal austerity with spending cuts and widening of the tax base amounting to around 2% of Gross Domestic Product (GDP) after five years, although its mainly backloaded. The energy price guarantee will now have its cap for average household dual tariff annual bill lifted from £2500 to £3000 from April 2023 and remain in place for a further 12 moths. This is less generous than the original plan to cap bills at £2500 for two years. The Office for Budget Responsibility’s (OBR) analysis suggests that the measures announced in the Autumn statement reduce the depth and length of the recession this year and next but leave the economy on a similar growth trajectory over the medium term. We expect real GDP to contract by 1.3% next year followed by growth of 2% in 2024. With this is mind, we expect the Bank of England (BOE) to pause its tightening cycle once rates get to 3.5% in December followed by 50Bps of cuts in H2 2023.

Eurozone to endure a short recession

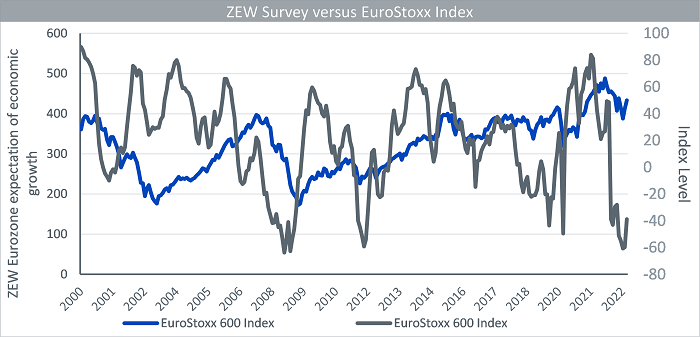

Owing to the external supply shock, Eurozone has faced a similar inflation narrative as the UK. In October Eurozone inflation reached 10.6% yoy. We expect inflation to remain high in the next few months, however starting early next year, the annual rates should decline aided by the base effects from the surge in energy prices in 2022. Owing to which we expect European Central Bank to continue to tighten monetary policy until Q1 2023. On the positive side, while Eurozone will endure a recession in Q4 2022 and Q1 2023, we expect the recession to be less deep than previously expected owing to the less dire gas situation. This was evident in the November ZEW survey, which showed expectations gauge for the economy in the six months ahead improve significantly to -38.7 in November from -59.2 in October. This remains in line with our view that in six months’ time the Eurozone economy should be on its way out of a recession.

Source: Bloomberg, WisdomTree as of 18 November 2022.

Historical performance is not an indication of future performance and any investments may go down in value

Federal Reserve (Fed) speakers singing from the same hymn book

Fed officials backed expectations they will moderate interest-rate increases to 50 basis points next month, while stressing the need to keep hiking into 2023. St. Louis Fed President James Bullard said policy makers should increase interest rates to at least 5% to 5.25% to curb inflation. He also warned of further financial stress ahead. Bullard’s comments came a day after San Francisco Fed President Mary Daly said a pause in rate hikes was “off the table.” Fed Governor Waller (one of the more hawkish Fed officials) emphasized that while rate hikes will likely slow to 50bp in December, the ultimate destination or “cruising altitude” will depend on labour market and inflation data. Waller echoed Atlanta Fed President Bostic’s concerns about labour costs pushing up service sector prices which in our view remains the key upside risk to inflation even as core goods prices have slowed. Fears are mounting that relentless rates increases will hit economic growth, with a critical segment of the Treasury yield curve at the most steeply inverted in four decades, historically such an inversion has tied in with a US recession.

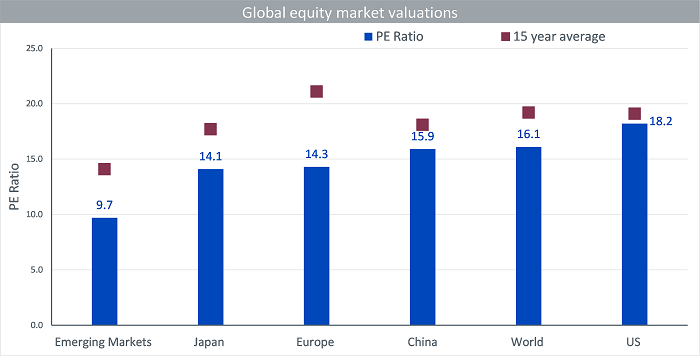

Maintaining a value bias within equities

Amidst the challenging backdrop for global equities, we have observed the value factor outperforming the growth factor by 17.3%2 in 2022. Across global markets, European equities are trading at the deepest discount (32%) from price to earnings (p/e) ratio to their 15-year average owing to fears of the energy crisis being detrimental to the economy.

Source: Bloomberg, WisdomTree as of 31 October 2022.

Historical performance is not an indication of future performance and any investments may go down in value

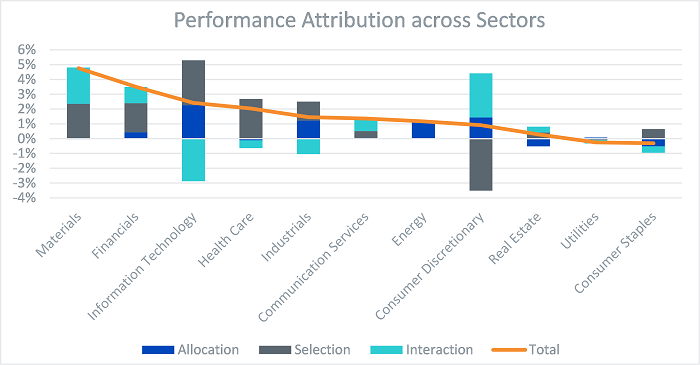

The recent 3Q 2022 earnings season provided evidence that European earnings have remained stubbornly resilient despite the broader macro turmoil. A deeper dive into the sector level suggest that energy, transport, utilities and healthcare have seen some of the biggest increases to their Earnings Per Share (EPS) estimates in 2022. The WisdomTree Europe Equity Income Index outperformed the MSCI Europe Index by 17% in 2022. The performance attribution highlighted below illustrates that the higher exposure to value sectors such as materials, financials, healthcare, industrials, and energy contributed to the outperformance.

Source: Bloomberg, WisdomTree as of 31 October 2022.

Historical performance is not an indication of future performance and any investments may go down in value

Sources

1 Source: Office for Budget responsibility as of 17 Nov 2022

2 Source: Performance difference between MSCI Global Value Index versus the MSCI Global growth index from 31 December 2021 to 31 October 2022. Historical performance is not an indication of future performance and any investments may go down in value.

—

Originally Posted November 21, 2022 – What’s Hot: Endgame for central banks far from done

Disclosure: WisdomTree Europe

This material is prepared by WisdomTree and its affiliates and is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. The opinions expressed are as of the date of production and may change as subsequent conditions vary. The information and opinions contained in this material are derived from proprietary and non-proprietary sources. As such, no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by WisdomTree, nor any affiliate, nor any of their officers, employees or agents. Reliance upon information in this material is at the sole discretion of the reader. Past performance is not a reliable indicator of future performance.

Please click here for our full disclaimer.

Jurisdictions in the European Economic Area (“EEA”): This content has been provided by WisdomTree Ireland Limited, which is authorised and regulated by the Central Bank of Ireland.

Jurisdictions outside of the EEA: This content has been provided by WisdomTree UK Limited, which is authorised and regulated by the United Kingdom Financial Conduct Authority.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from WisdomTree Europe and is being posted with its permission. The views expressed in this material are solely those of the author and/or WisdomTree Europe and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.