Study Notes:

Once a municipal bond issuance has been priced and the deal is closed, the bond then resides in the secondary market, where it may be bought, sold or held by an investor until it reaches maturity, or is called away by the issuer.

In this lesson, we’ll explore some features of municipal bonds an investor should be aware of when making a purchase, including:

- Accrued interest,

- The dated date, as well as

- Yield-related pricing terms

Accrued Interest

The buyer of a municipal bond is required to pay the market price for the issuance, as well as the accrued interest on it. To find the amount of the accrued interest, we’ll first need to know a few specific dates, which are:

- The most recent coupon date

- The bond’s settlement date, and

- The maturity date

It’s important to keep in mind that municipal bonds settle on a T+2 basis, meaning they settle two days after their initial purchase and, for the purposes of counting daily interest, we consider every month, regardless of the month, as comprising 30 days, and every year, a fixed-number of 360 days.

Note also that interest payments on municipal bonds are made semiannually, with payments made on dates based on the maturity date.

The number of accrued days of interest spans from the last coupon date up to, but not including, the settlement date.

Accrued Interest Calculation: Example

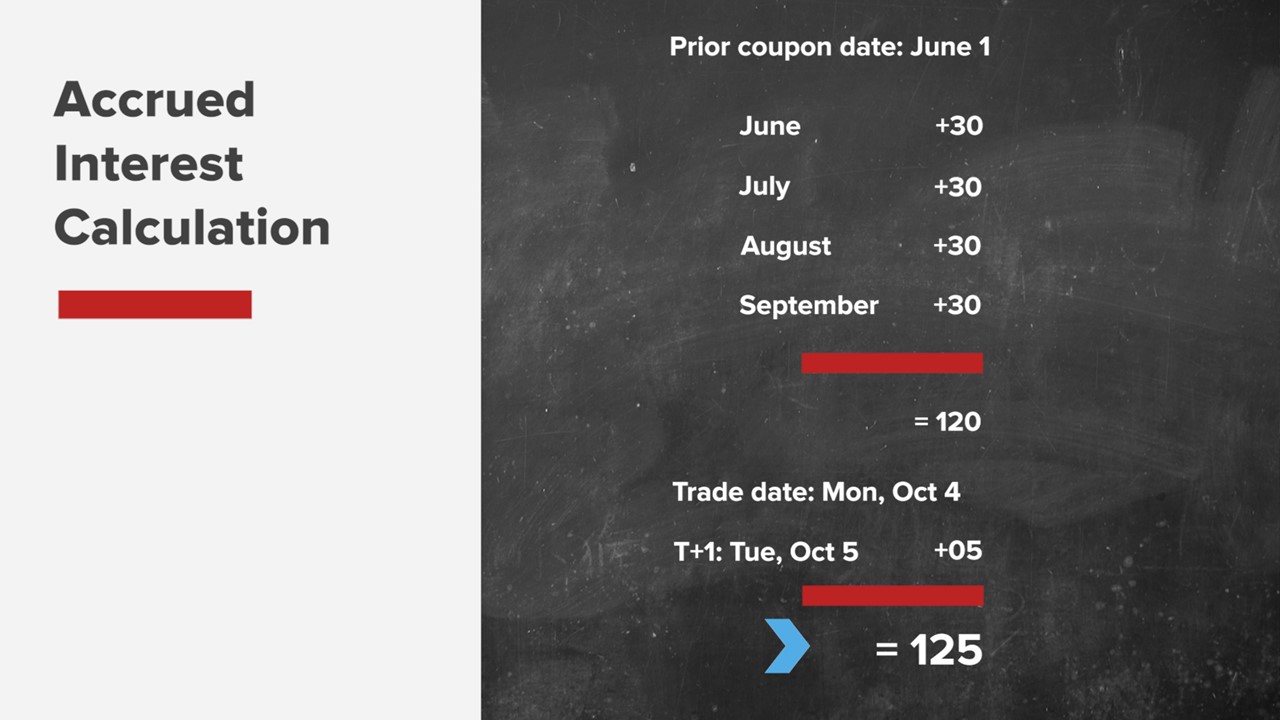

On Monday, October 4th, you buy $20,000 worth of a 3% municipal bond that matures on December 1, 2019.

Determine the Number of Accrued Days

Since interest payments are made semiannually based on the maturity date, we can anticipate they will be made on June 1 and December 1.

Now, because you bought the bond on October 4th, the last coupon date prior to the purchase was June 1—marking the starting point to the accrued interest calculation.

To figure out the end point, just use the day prior to settlement. Remember, settlement occurs two business days after the trade date (T+2). This means the bond will settle on Wednesday, October 6—two days after October 4, when it was bought.

The entire timeline, then, is from June 1, the most recent coupon date prior to purchase, to October 5, that is up to, but not including the settlement date.

How many days are in this timeline?

Well, recall that we consider every month as having 30 days, regardless of the month. With that, we count:

30 days for each of June, July, August, and September, plus those five days in October, for a total of 125 days of accrued interest.

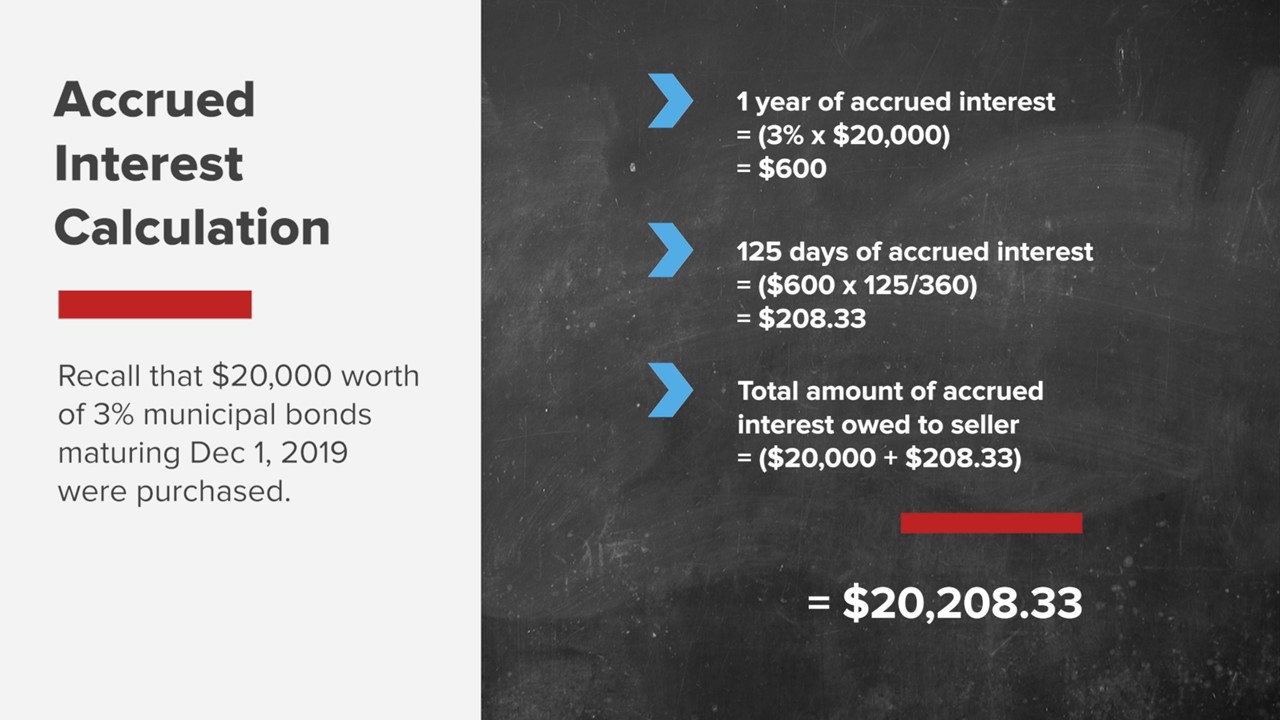

Determine the Amount Owed

Now that we know the number of days, we can figure out how much the buyer needs to pay the seller for the accrued interest.

Taking a look at the formula below, we see that the total amount the buyer will pay the seller when purchasing this bond will be US$20,208.33.

What is the ‘Dated Date’?

When referring to the dated date of a municipal bond, this simply means the date on which interest begins to accrue. If it’s a new issuance, then there would be no prior coupon date to consider the dated date, therefore the dated date is the same as the issue date.

Pricing

Because municipal bonds may have a call feature, a date that the bond may be called away from the buyer, in addition to a final maturity date, the Municipal Securities Rulemaking Board (MSRB), requires the seller to disclose whichever price or yield would be the worst case scenario for the buyer, or the ‘yield-to-worst’. Would it be the yield calculated to maturity or the yield calculated to the call date?

MSRB & EMMA

The MSRB is a self-regulatory organization (SRO) for firms that deal in municipal securities.

It crafts the rules and regulations that relate to municipal underwritings, as well as houses official statements and other documents related to municipal bond issuance in its Electronic Municipal Market Access system (EMMA).

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.