AT A GLANCE

- Since March 2022, the Federal Reserve has raised interest rates by 300 basis points

- Higher rates are challenging both homebuyers and sellers

There are growing signs that the Federal Reserve’s rate policies are starting to bite into the U.S. housing market.

Mortgage rates on 30-year fixed rate loans have risen from around 3% at the end of 2020 to just over 7% in October 2022 as the Fed has withdrawn its accommodative monetary policy and raised short-term rates. One would have to go back two decades to the year 2000 to find U.S. mortgage rates as high as they are now. (A relatively shallow recession followed that period.)

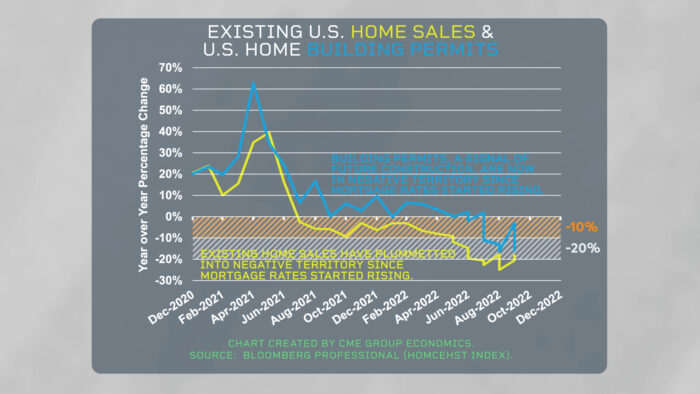

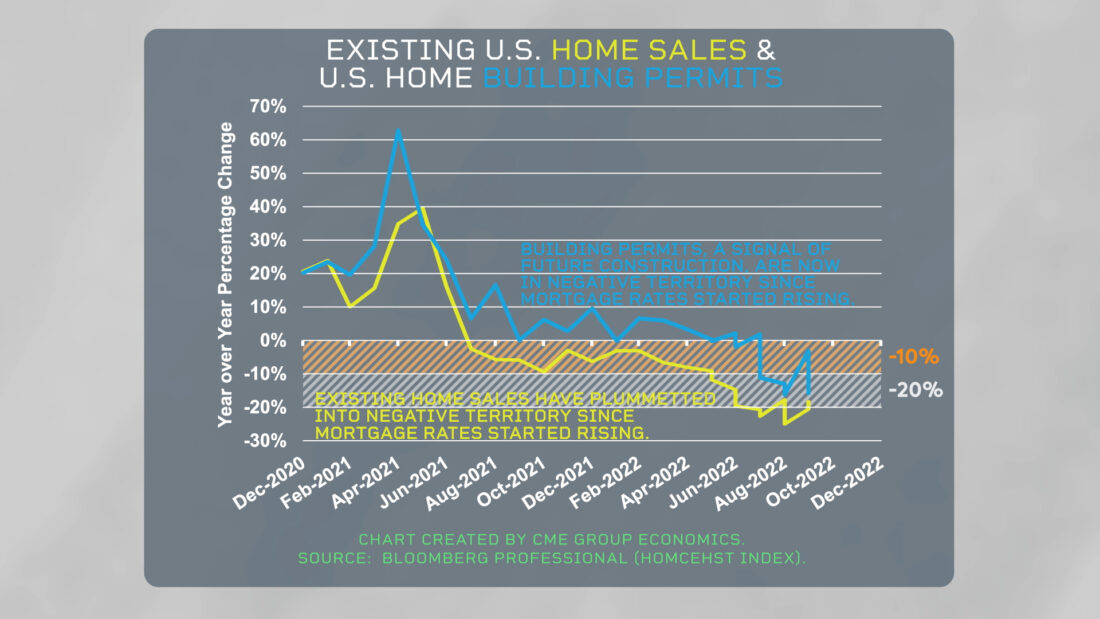

The current higher mortgage rates are clearly impacting the housing market today. Sales of existing homes have dropped to about 20% below year-ago levels, while building permits for new home construction have fallen over 10% below year-ago levels.

But is this housing slowdown likely to be anything as bad as what occurred in the sub-prime mortgage crisis that presaged the Great Recession of 2008-2009? No. It is different this time.

During the Great Recession, the unemployment rate went to 10%. Many borderline home buyers lost the income to pay their mortgages and were forced to sell their homes, deepening the economic crisis.

In 2022, the unemployment rate has yet to rise, remaining below 4% for now.

Equally important, most homeowners are of much better credit quality than in the 2008 debacle, and they are sitting on very low fixed rate mortgages. They can still pay their mortgage, so there’s no forced sales crisis this time around. But homeowners cannot afford to give up the low-rate mortgage to move up, buy a new home and sell their existing one. This means the supply of existing homes will be quite constrained, tempering the housing impact on the economy. Still, new home construction appears headed to a much slower pace in 2023.

Monetary policy acts with a lag, but for the housing market, one can now see that rising rates are taking their toll. However, one may not see the impact in the inflation data for many months to come, as the knock-on effects from a weak housing market take their time to domino through the economy.

—

Originally Posted October 31, 2022 – Trouble Ahead for U.S. Housing?

All examples are hypothetical interpretations of situations and are used for explanation purposes only. The views expressed in OpenMarkets articles reflect solely those of their respective authors and not necessarily those of CME Group or its affiliated institutions. OpenMarkets and the information herein should not be considered investment advice or the results of actual market experience. Neither futures trading nor swaps trading are suitable for all investors, and each involves the risk of loss. Swaps trading should only be undertaken by investors who are Eligible Contract Participants (ECPs) within the meaning of Section 1a(18) of the Commodity Exchange Act. Futures and swaps each are leveraged investments and, because only a percentage of a contract’s value is required to trade, it is possible to lose more than the amount of money deposited for either a futures or swaps position. Therefore, traders should only use funds that they can afford to lose without affecting their lifestyles and only a portion of those funds should be devoted to any one trade because traders cannot expect to profit on every trade. BrokerTec Americas LLC (“BAL”) is a registered broker-dealer with the U.S. Securities and Exchange Commission, is a member of the Financial Industry Regulatory Authority, Inc. (www.FINRA.org), and is a member of the Securities Investor Protection Corporation (www.SIPC.org). BAL does not provide services to private or retail customers.. In the United Kingdom, BrokerTec Europe Limited is authorised and regulated by the Financial Conduct Authority. CME Amsterdam B.V. is regulated in the Netherlands by the Dutch Authority for the Financial Markets (AFM) (www.AFM.nl). CME Investment Firm B.V. is also incorporated in the Netherlands and regulated by the Dutch Authority for the Financial Markets (AFM), as well as the Central Bank of the Netherlands (DNB).

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from CME Group and is being posted with its permission. The views expressed in this material are solely those of the author and/or CME Group and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.