Sweetgreen (SG) is expected to go public on November 18, 2021 with a midpoint valuation of $24/share, which would earn the stock our Unattractive rating.

Despite its large online presence, Sweetgreen lost market share in 2020 to stronger, better-positioned competitors. Sweetgreen’s locally-sourced supply chain adds safety risks and hurts the company’s ability to achieve the economies of scale that more vertically integrated restaurants enjoy.

The company has never achieved profits in any fiscal period since it began operations, and we see little to no path to profitability in the future.

Our IPO research aims to provide investors with more reliable fundamental research.

Sweetgreen’s Big Miss In 2020

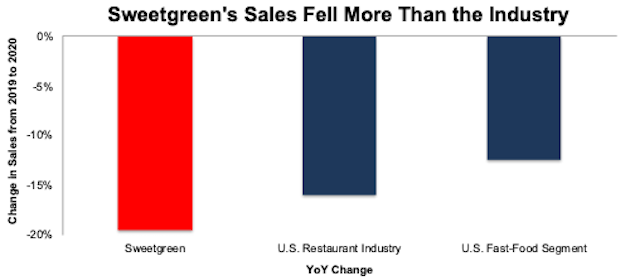

More than 10% of U.S. restaurants closed in 2020, and the survivors took their market share. In particular, quick-service restaurants (QSR) fared better than the overall industry. While U.S. restaurant sales fell 16% year-over-year in 2020, QSR sales fell just 12%.

With consumers turning to quick service and online options, 2020 was an opportune time for Sweetgreen, which generated half of its 2019 revenue from online sales, to gain market share. Instead, Sweetgreen’s share of the fast-food and overall restaurant market fell as its revenue declined 20% YoY, more than the market, in 2020, per Figure 1.

Figure 1: Sweetgreen Vs. U.S. Restaurant Industry & Fast-Food Segment: 2020 YoY Change in Sales

Sources: New Constructs, LLC, company filings, FRED, and Statista

Click here to read the full article

—

Check out this week’s Danger Zone interview with Chuck Jaffe of Money Life.

This article originally published on November 15, 2021.

Disclosure: David Trainer, Kyle Guske II, and Matt Shuler receive no compensation to write about any specific stock, style, or theme.

Follow us on Twitter, Facebook, LinkedIn, and StockTwits for real-time alerts on all our research.

[1] This list is a sample of Sweetgreen’s competitors and is not exhaustive, but serves to illustrate the crowded nature of Sweetgreen’s target market.

[2] Only Core Earnings enable investors to overcome the inaccuracies, omissions and biases in legacy fundamental data and research, as proven in Core Earnings: New Data & Evidence, written by professors at Harvard Business School (HBS) & MIT Sloan and published in The Journal of Financial Economics.

[3] Includes food, beverage, and packaging, labor, occupancy, and other operating costs to match Sweetgreen’s “Total Restaurant Operating Costs”, which are reported to include food, beverage, and packaging, labor and related expenses, occupancy and related expenses, and other restaurant operating costs.

Click here to download a PDF of this report.

Disclosure: New Constructs

David Trainer, Kyle Guske II, Sam McBride, Matt Shuler, Alex Sword, and Andrew Gallagher receive no compensation to write about any specific stock, style, or theme.

The information and opinions presented in this report are provided to you for information purposes only and are not to be used or considered as an offer or solicitation of an offer to buy or sell securities or other financial instruments. New Constructs has not taken any steps to ensure that the securities referred to in this report are suitable for any particular investor and nothing in this report constitutes investment, legal, accounting or tax advice. This report includes general information that does not take into account your individual circumstance, financial situation or needs, nor does it represent a personal recommendation to you. The investments or services contained or referred to in this report may not be suitable for you and it is recommended that you consult an independent investment advisor if you are in doubt about any such investments or investment services.

Information and opinions presented in this report have been obtained or derived from sources believed by New Constructs to be reliable, but New Constructs makes no representation as to their accuracy, authority, usefulness, reliability, timeliness or completeness. New Constructs accepts no liability for loss arising from the use of the information presented in this report, and New Constructs makes no warranty as to results that may be obtained from the information presented in this report. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, express or implied, is made regarding future performance. Information and opinions contained in this report reflect a judgment at its original date of publication by New Constructs and are subject to change without notice. New Constructs may have issued, and may in the future issue, other reports that are inconsistent with, and reach different conclusions from, the information presented in this report. Those reports reflect the different assumptions, views and analytical methods of the analysts who prepared them and New Constructs is under no obligation to insure that such other reports are brought to the attention of any recipient of this report.

New Constructs’ reports are intended for distribution to its professional and institutional investor customers. Recipients who are not professionals or institutional investor customers of New Constructs should seek the advice of their independent financial advisor prior to making any investment decision or for any necessary explanation of its contents.

In-depth risk/reward analysis underpins our stock rating. Our stock rating methodology grades every stock according to what we believe are the 5 most important criteria for assessing the quality of a stock. Each grade reflects the balance of potential risk and reward of buying that stock. Our analysis results in the 5 ratings described below. Very Attractive and Attractive correspond to a “Buy” rating, Very Unattractive and Unattractive correspond to a “Sell” rating, while Neutral corresponds to a “Hold” rating.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from New Constructs and is being posted with its permission. The views expressed in this material are solely those of the author and/or New Constructs and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.