The Consumer Sentiment Index for November plummeted to 54.7, much worse than market expectations of 59.5 and a sharp decline from October’s 59.9 level. The dramatic decline offsets half of the recovery from this June’s low of 50, the worst reading since the survey began in 1952. This month’s reading reflects broad weakening across all categories and implies that consumers are feeling the pain of inflation, rising interest rates and tighter credit conditions.

Pessimism among consumers may be a positive for the Federal Reserve’s (the Fed) inflation battle with today’s data implying that Americans are ready to tighten their purse strings, yet in my view, it also implies that the economy is heading for a recession next year rather than a soft landing.

Importantly, sentiment regarding the economy, purchasing conditions and inflation worsened.

Economic Conditions

Sentiment for current economic conditions declined from 65.6 in October to 57.8. Consumers aren’t feeling warm and fuzzy about the future either, with sentiment concerning future economic conditions declining from 56.2 to 52.7. Sentiment tanked across diverse age groups, educational attainment levels, income levels, geographies and political affiliations. Global economic growth deceleration and midterm election uncertainty were cited as reasons that weighed on overall sentiment.

Purchasing Conditions

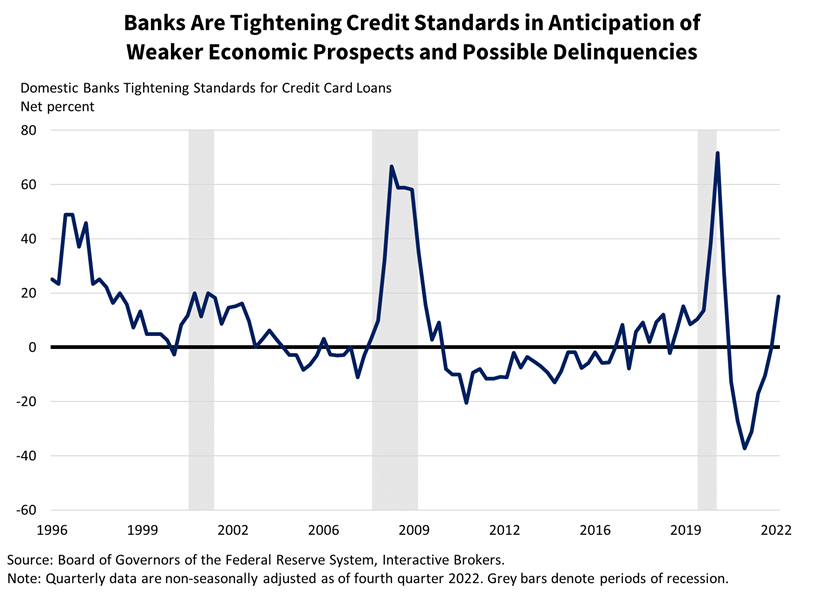

Purchasing conditions for durable goods worsened significantly and weighed the most on the headline number. The one-two punch of higher financing costs and higher prices has hampered demand for durable goods, leading to rising inventories. Banks are also tightening credit conditions, which isn’t helping sentiment. Consumers who don’t satisfy incrementally rigid credit requirements when attempting to make a large purchase are likely to feel dejected.

Additionally, supply chain challenges from Chinese lockdowns continue to weigh on production, materials, labor and transportation, propelling prices higher. The potential easing of Chinese lockdowns reported today, if sustained, may help temper inflation longer term through supply chain efficiency gains. In the short term, however, it’s likely to propel inflation higher as it will increase demand for commodities, especially oil and gas whose prices remain very high amidst tight supplies. Oil and natural gas are up 4% and 3% in early trading today in response to the news about Chinese lockdowns.

Inflation

Consumers are expecting inflation next year to be 5.1%, up from the 5.0% expectation recorded last month. Consumers are expecting longer term inflation over the next five years to settle closer to the Fed’s 2% target at 3%, up from 2.9% last month.

A Potentially Rocky Road Ahead

While today’s data implies consumer demand may weaken, which can help soften future price gains, the low sentiment is consistent with economic downturns, strengthening the case for a hard landing next year. While most recent recessions have been accompanied by higher joblessness, the coming downturn will be characterized by an affordability sting for consumers. Overall, this report points to a tapped-out consumer that is likely to weaken further into next year.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.