")

An ETF investor guide to supply chain disruptions.

KEY TAKEAWAYS

- Supply chain bottlenecks are hitting sectors including labor, microchips and housing.

- Some of these disruptions will be around for the longer term, and investors should think about what they mean for portfolios.

- ETFs can help provide diversified, low-cost access to targeted sectors of the market to help offset the effects of supply-chain disruptions.

Odds are high that you’ve recently experienced COVID-related supply chain woes in some form or another. The disruptions hit home for me at the local bike store, where the owner told me they would have no Treks in my size until March 2022 — a full six months from now. The hold-up is about delays in manufacturing overseas and a backlog at West Coast ports.

Investors can no longer avoid supply chain disruptions, whether it’s surging electricity prices in China (crippling factory production), a widespread microchip shortage (creating a scarcity of new cars), or a lack of workers to perform key jobs, like driving trucks (sparking delivery delays for gasoline). It appears that the reverberations of the pandemic on the economy will be with us for longer than most economists expected, and in complex ways.

This article lays out the supply chain considerations that keep coming up in our conversations and how exchange traded funds (ETFs) can help investors navigate the backdrop.

FORCES AT WORK

The most recent jobs report from the U.S. Department of Labor showed 5 million fewer people at work compared with before the pandemic.1 Many factors are at play: The pandemic has taken a significant toll on women, given fewer options for childcare.2 And about half of those no longer working are over 55, may have retired and are therefore not likely to return to the labor force.3

While there are fewer workers, demand for hiring has never been stronger. Job openings are near record levels with 49% more vacancies than pre-pandemic and more people quitting to find new jobs.4 The share of workers quitting their jobs hit the highest level since 2000, with a quits rate of 2.9%.4 Wages have ticked up based on the supply and demand dynamics, something we expect to continue in the medium term.

WHAT IT MEANS FOR INVESTORS

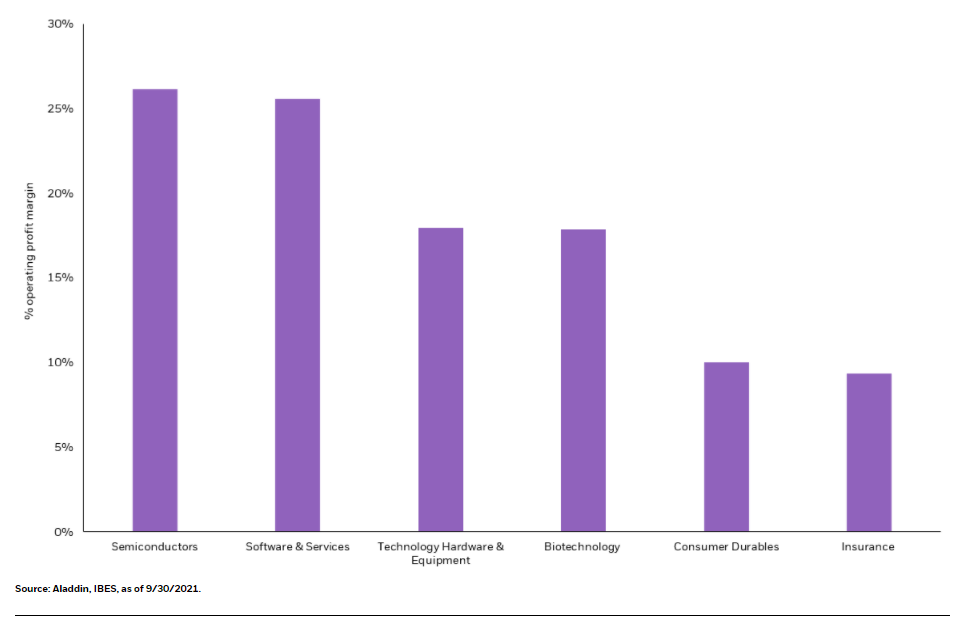

Higher wages mean higher costs for companies, and we favor sectors and industries that are less sensitive to labor costs and have the highest profit margins. On this front, think technology companies, consumer discretionary companies, and financial companies, including banks, to help insulate portfolios against rising labor costs.

S&P 500 industries with the highest profit margins (less impacted by rising wages / input costs)

Click here to read the full article

—

Originally Posted on October 15, 2021 – The Long and Short of Shortages

© 2021 BlackRock, Inc. All rights reserved.

1 U.S. Department of Labor, as of 9/3/2021

2 COVID-19: Implications for business, McKinsey report, 10/6/2021

3 U.S. Department of Labor, as of 9/3/21

4 Job Openings and Labor Turnover Survey (JOLTS), as of 10/13/2021

5 Bloomberg, as of 9/30/2021

Carefully consider the Funds’ investment objectives, risk factors, and charges and expenses before investing. This and other information can be found in the Funds’ prospectuses or, if available, the summary prospectuses, which may be obtained by visiting the iShares Fund and BlackRock Fund prospectus pages. Read the prospectus carefully before investing

Investing involves risk, including possible loss of principal.

International investing involves risks, including risks related to foreign currency, limited liquidity, less government regulation and the possibility of substantial volatility due to adverse political, economic or other developments. These risks often are heightened for investments in emerging/ developing markets or in concentrations of single countries.

Funds that concentrate investments in specific industries, sectors, markets or asset classes may underperform or be more volatile than other industries, sectors, markets or asset classes and than the general securities market.

Technologies perceived to displace older technologies or create new markets may not in fact do so. Companies that initially develop a novel technology may not be able to capitalize on the technology.

Real estate investment trusts (“REITs”) are subject to changes in economic conditions, credit risk and interest rate fluctuations.

The iShares GSCI Commodity Dynamic Roll Strategy ETF is a commodity pool, as defined in the Commodity Exchange Act and the applicable regulations of the Commodity Futures Trading Commission, or “CFTC,” and is managed by its Advisor, BlackRock Fund Advisors, a commodity pool operator registered with the CFTC.

The Fund’s use of derivatives may reduce the Fund’s returns and/or increase volatility and subject the Fund to counterparty risk, which is the risk that the other party in the transaction will not fulfill its contractual obligation. Commodity futures trading may be illiquid. In addition, suspensions or disruptions of market trading in the commodities markets and related futures markets may adversely affect the value of the Fund. Certain derivatives may give rise to a form of leverage and may expose the Fund to greater risk and increase its costs. To the extent that the Fund invests in rolling futures contracts, it may be subject to additional risk. An increase in interest rates may cause the value of fixed-income securities held by the Fund to decline.

Investing in commodity-linked derivatives and commodity-related companies may increase volatility. Price movements are outside of the Fund’s control and may be influenced by weather and climate conditions, livestock disease, war, terrorism, political conflicts and economic events, interest rates, currency and exchange rates, government regulation and taxation. Commodity futures trading may be illiquid. In addition, suspensions or disruptions of market trading in the commodities markets and related futures markets may adversely affect the value of the Fund.

Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments.

Non-investment-grade debt securities (high-yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher-rated securities.

TIPS can provide investors a hedge against inflation, as the inflation adjustment feature helps preserve the purchasing power of the investment. Because of this inflation adjustment feature, inflation protected bonds typically have lower yields than conventional fixed rate bonds and will likely decline in price during periods of deflation, which could result in losses. Government backing applies only to government issued securities, and does not apply to the funds.

An investment in the Fund is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency and its return and yield will fluctuate with market conditions.

This material represents an assessment of the market environment as of the date indicated; is subject to change; and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any issuer or security in particular.

The strategies discussed are strictly for illustrative and educational purposes and are not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. There is no guarantee that any strategies discussed will be effective.

The information presented does not take into consideration commissions, tax implications, or other transactions costs, which may significantly affect the economic consequences of a given strategy or investment decision.

This material contains general information only and does not take into account an individual’s financial circumstances. This information should not be relied upon as a primary basis for an investment decision. Rather, an assessment should be made as to whether the information is appropriate in individual circumstances and consideration should be given to talking to a financial professional before making an investment decision.

The information provided is not intended to be tax advice. Investors should be urged to consult their tax professionals or financial professionals for more information regarding their specific tax situations.

The Funds are distributed by BlackRock Investments, LLC (together with its affiliates, “BlackRock”).

The iShares Funds are not sponsored, endorsed, issued, sold or promoted by Bloomberg, BlackRock Index Services, LLC, Cohen & Steers, European Public Real Estate Association (“EPRA®”), FTSE International Limited (“FTSE”), ICE Data Indices, LLC, NSE Indices Ltd, JPMorgan, JPX Group, London Stock Exchange Group (“LSEG”), MSCI Inc., Markit Indices Limited, Morningstar, Inc., Nasdaq, Inc., National Association of Real Estate Investment Trusts (“NAREIT”), Nikkei, Inc., Russell or S&P Dow Jones Indices LLC. None of these companies make any representation regarding the advisability of investing in the Funds. With the exception of BlackRock Index Services, LLC, which is an affiliate, BlackRock Investments, LLC is not affiliated with the companies listed above.

Neither FTSE, LSEG, nor NAREIT makes any warranty regarding the FTSE Nareit Equity REITS Index, FTSE Nareit All Residential Capped Index or FTSE Nareit All Mortgage Capped Index. Neither FTSE, EPRA, LSEG, nor NAREIT makes any warranty regarding the FTSE EPRA Nareit Developed ex-U.S. Index or FTSE EPRA Nareit Global REITs Index. “FTSE®” is a trademark of London Stock Exchange Group companies and is used by FTSE under license.

© 2021 BlackRock, Inc. All rights reserved. BLACKROCK, BLACKROCK SOLUTIONS, BUILD ON BLACKROCK, ALADDIN, iSHARES, iBONDS, FACTORSELECT, iTHINKING, iSHARES CONNECT, FUND FRENZY, LIFEPATH, SO WHAT DO I DO WITH MY MONEY, INVESTING FOR A NEW WORLD, BUILT FOR THESE TIMES, the iShares Core Graphic, CoRI and the CoRI logo are trademarks of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other marks are the property of their respective owners.

iCRMH1021U/S-1863290

Disclosure: iShares by BlackRock

The iShares Funds are distributed by BlackRock Investments, LLC (together with its affiliates, “BlackRock”).

The iShares Funds are not sponsored, endorsed, issued, sold or promoted by Markit Indices Limited, nor does this company make any representation regarding the advisability of investing in the Funds. BlackRock is not affiliated with Markit Indices Limited.

©2022 BlackRock, Inc. All rights reserved. iSHARES and BLACKROCK are registered trademarks of BlackRock, Inc., or its subsidiaries in the United States and elsewhere. All other marks are the property of their respective owners.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from iShares by BlackRock and is being posted with its permission. The views expressed in this material are solely those of the author and/or iShares by BlackRock and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

")