")

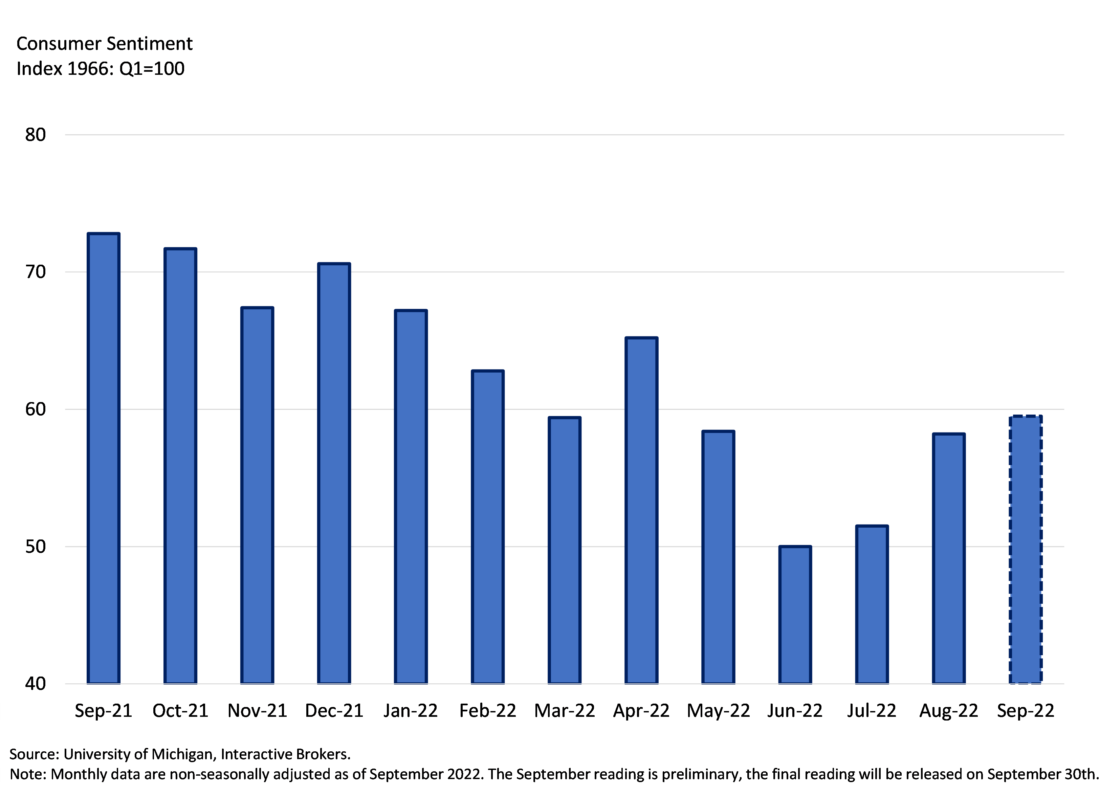

Preliminary consumer sentiment for September came in at 59.5, slightly softer than market expectations of 60 and an improvement from August’s 58.2 level. The one-year economic outlook improved as declines in energy prices are alleviating cost pressures on household budgets. Declines in energy prices help consumers at the gas pump, on electricity bills, when buying air fares, when shopping for goods and services, etc. Lower energy costs contribute to declines in transportation costs which limit business costs and places downward pressure on inflation. Consumers don’t like higher prices and lower energy bills support budget flexibility. Expectations for inflation one year from now declined to 4.6 percent from 4.8 percent in August while expectations for inflation five years from now declined from 2.9 percent to 2.8 percent. Consumers expressed concerns about their personal finances, their ability to purchase high-cost durable goods and uncertainty regarding economic conditions.

Things are getting better as energy costs relieve a large burden; however, a reading of 59.5 is consistent with a recessionary consumer. In addition, a personal savings rate of 5 percent also points to recessionary stress as consumers are pressured by higher costs despite a tight labor market with growing wages. Labor market wage gains continue to trail inflation which means that on balance, workers are not maintaining their purchasing power and are receiving less goods and services for their hours worked. Finally, and with serious concern, credit card debt is piling up to historic records as consumers turn to unsecured debt to fund their lifestyles. Hold on, what about higher interest rates, isn’t that bad for credit card balances?

As a kid a very, very long time ago, I recall a large segment of the community talking about how bad credit cards were. “It’s easy to buy everything you want, but then it’s much more difficult to pay it back, especially when carrying large balances”. This quote from my childhood is especially true against the backdrop of Fed tightening. As the Fed raises rates and tightens financial conditions, credit card rates rise in the aggregate. Which means that the high level of credit card balances will need to be paid back at higher rates of interest, compound interest in a not so wonderful way.

It’s music to the Fed’s ears to know that inflation expectations are falling and consumers are feeling lousy, it places downward pressure on demand and inflation; however, I suspect that credit card debt is the culprit contributing to signals of hot demand. Just this week we saw an inflation reading and a retail sales reading that were solidly above expectations. These hot readings led to selloffs in equities and bonds as the street ratcheted up their expectations of the Fed tightening and long-term inflation expectations. Consumers may be feeling lousy, but they are clearly continuing to spend.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

")