")

I imagine that many readers are familiar with the term “butterfly effect”. In common parlance, its oversimplified definition is that a large weather system can be influenced by a small perturbation, such as a butterfly flapping its wings thousands of miles away. In actuality, it describes an aspect of chaos theory when “a small change in one state of a deterministic nonlinear system can result in large differences in a later state.” We can write dissertations about whether markets are deterministic and nonlinear, and to what degree chaos theory is applicable to markets[i], but this morning’s market activity appears to be a wonderful illustration of the butterfly effect in US equity markets.

On Friday evening I got an alert on my phone saying that the Turkish president removed the country’s central bank governor. My trading week was over by the time the news arrived, with a quarterly triple (not quadruple) witching expiration behind us. I have to admit, my first thought was not “I need to buy NQ futures on Sunday night”, but that would have become a solid trade by the time that US markets opened on Monday. It appears that the news out of Turkey is another example of the butterfly effect in global financial markets.

I am by no means an expert in Turkish politics, but it is hardly a sign of economic stability when a president fires his third central bank governor in less than two years. Markets are not happy when central bank independence is threatened, let alone usurped by political leaders, especially when that becomes somewhat routine. No one should have been surprised that the Turkish lira plunged by more than 15% against the US dollar (it has since improved to -10% today) or that major Turkish equity indices fell by about 10% this morning. While it is not uncommon for local stock indices to rise when a nation’s currency is devalued, that occurs when investors believe that the weaker currency will spur exports. That was not the interpretation for investors in Turkish assets. Markets gave this move a true vote of no confidence.

It is therefore not surprising that US Treasury bills and notes rallied this morning. US Treasuries are considered a haven by much of the world’s investment community, and benefit from a “flight to safety” bid. Turkish investors, along with those in other emerging markets, sought protection in Treasuries and other safe assets. Prices of those assets rose, pushing yields lower. The combination of a flight to safety bid and a somewhat oversold bond market led to a 3 basis point reduction in the key 10-year yield.

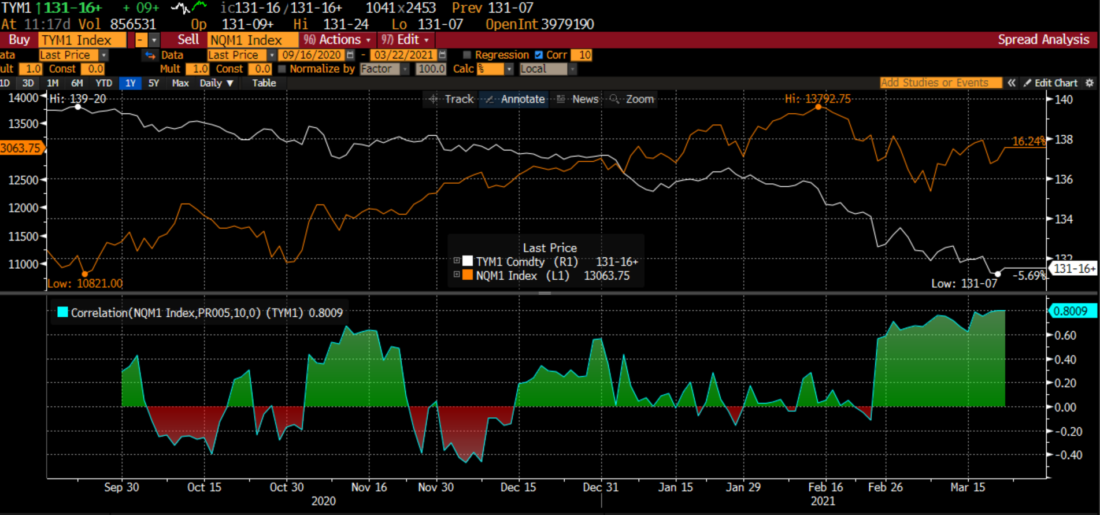

That would normally be the start of a “risk-off” day for the markets. But the situation in Turkey was relatively contained. There are few signs of contagion throughout other emerging markets and European banks. Thus, with the rest of the world still in a generally “risk-on” mood, traders were free to interpret the bond markets’ moves in a positive light. Over recent sessions, there has been a definite correlation between 10-year note rates and the NASDAQ 100 Index (NDX). By one measure, they have an R^2 of about 0.80, which is substantial[ii]. If ordinary investors and the media notice this correlation, we can be certain that algorithms are already taking advantage of this relationship.

We can argue whether there is causation as well as correlation in the relationship between 10-year notes and NDX (space simply does not permit it here), but it is clear that traders would be reacting favorably to a decline in yields as long as the risk-off mentality is limited to a specific region and set of investors. (Other risk-off assets like gold failed to find a bid and traded lower.) Thus, the risk-off mentality that took root in Turkey led to a rally in NDX and many of its key components[iii].

That, dear readers, is an example of the butterfly effect in global markets and specifically in US equities. A central bank governor in Turkey, someone who has virtually no effect on US technology shares on a daily basis, is fired. That led to a flight to safety bid in US Treasuries as investors fled the Turkish lira, which in turn led to bid for the NDX index and its components. A small change in one part of the system led to a large influence elsewhere.

[i] My takes: markets are not deterministic, since randomness is certainly involved in the development of future stages in the system; they are almost definitely nonlinear, since changes in output are quite frequently not directly proportional to inputs; and that there are many applications of chaos theory to investing. Markets are clearly chaotic, but I would argue that markets are non-deterministic and not truly subject to the tenets of chaos theory. Yet there is a fractal nature to markets – think of how intraday charts can resemble long term charts – and strange attractors appear to exist.

[ii] Here is a graph from Bloomberg that shows the high recent correlation between percentage moves in the front month Treasury Note (TYM1) and NASDAQ (NQM1) futures:

[iii] Another key factor positively affecting NDX was the $3,000 price target placed upon Tesla (TSLA) by Cathie Wood of Ark Management. One could certainly question the objectivity of an asset manager placing an outlandish price target on her largest holding, but I’ll avoid that fray for now.

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Forex

There is a substantial risk of loss in foreign exchange trading. The settlement date of foreign exchange trades can vary due to time zone differences and bank holidays. When trading across foreign exchange markets, this may necessitate borrowing funds to settle foreign exchange trades. The interest rate on borrowed funds must be considered when computing the cost of trades across multiple markets.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.