Emerging markets are not a homogenous group, and there will be both winners and losers from higher energy prices.

In Europe, a near-exponential surge in the price of natural gas, which is up just over 100% year-to-date, has stoked fears about inflation and outright shortages of energy.

Activity in China has been disrupted after a surge in coal prices saw power companies pull the plug. And the price of oil is creeping higher as the OPEC+ group elected to stick to its recently agreed production targets in spite of rising demand.

There are a lot of moving parts meaning that it is hard to know where prices will go from here. The government in China has moved to ease the energy crunch by ordering an increase in mining output. Meanwhile President Putin appeared to signal that Russia will pipe more gas to Europe. As the northern hemisphere heads into winter though, there is a good chance that energy prices will remain high.

In the longer term, the energy transition should lead to a structural, long term decline in demand for fossil fuels. However, in the near term a reluctance to invest in new capacity means that there are likely to be more periodic episodes of high prices for fossil fuels. As such, it makes sense to consider which emerging markets benefit from higher energy prices and which do not.

Who are the EM winners from higher energy prices?

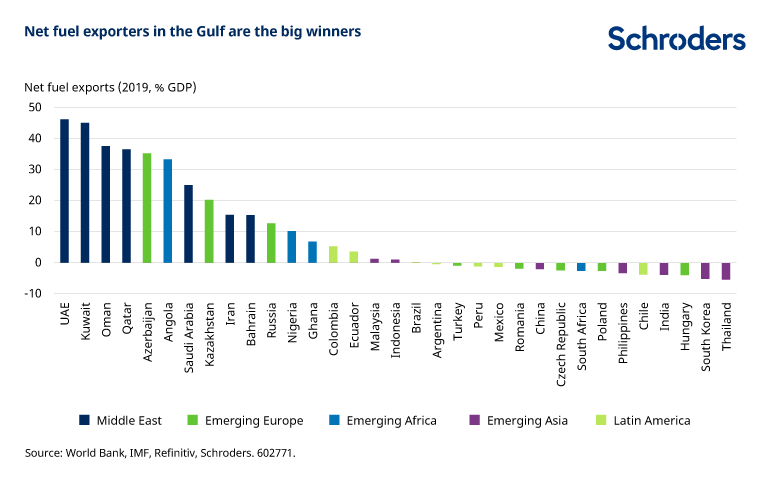

The winners are obvious. Those EM that are major net exporters of fossil fuels are set for a windfall from higher receipts. As the chart below makes clear, the biggest beneficiaries are in the Gulf, where net fuel exports are worth almost 50% of GDP in the UAE and Kuwait, while they are equivalent to roughly one quarter of national output in Saudi Arabia. The other big winners are Russia, along with various frontier markets.

All other things equal, higher energy prices will boost the terms of trade, the ratio of exports prices to imports prices, of energy exporters. This should support growth, help to improve balance of payments positions and give a lift to floating exchange rates where they are present. Colombia is likely to be a key beneficiary here, given its structurally poor balance of payments.

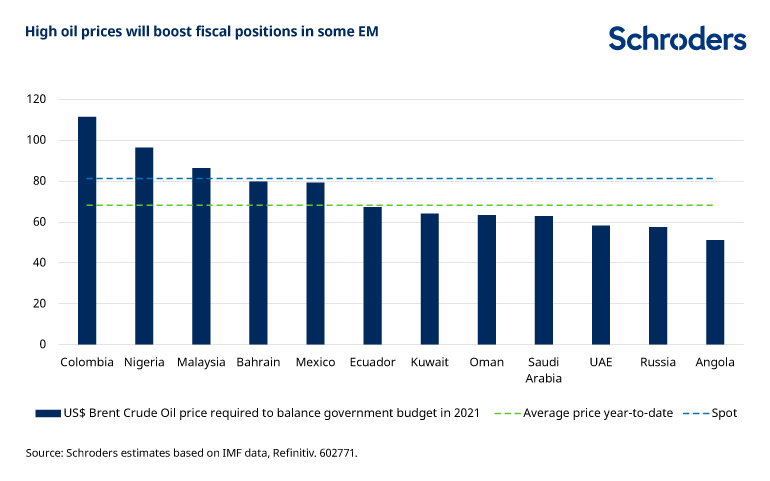

Moreover, for governments that rely heavily on revenues from fossil fuels, higher prices should similarly improve fiscal positions allowing either debt to be paid down debt or spending to be increased. Our rough estimates show that most major EM oil producers need an oil price of around $60 per barrel in order to balance the public finances. As such, if oil prices were to remain around current levels of about $80 per barrel for an extended period of time, these EM would build fiscal surpluses.

Wealthy nations are likely to save much of the windfall. Perhaps the bigger impact would be in heavily indebted frontier markets such as Angola and Ecuador, where poor debt dynamics would be eased, justifying tighter spreads on hard currency bonds.

Which EM could stand to lose from higher energy prices?

However, many major EM are net importers of fuel and therefore stand to lose from higher energy prices.

Net energy imports are equivalent to 2-5% of GDP in many countries in Central Eastern Europe (CEE) and Asia. Higher energy costs can have a negative impact by causing external accounts positions to deteriorate, driving-up production costs for manufacturers and dampening demand by squeezing real incomes through higher inflation.

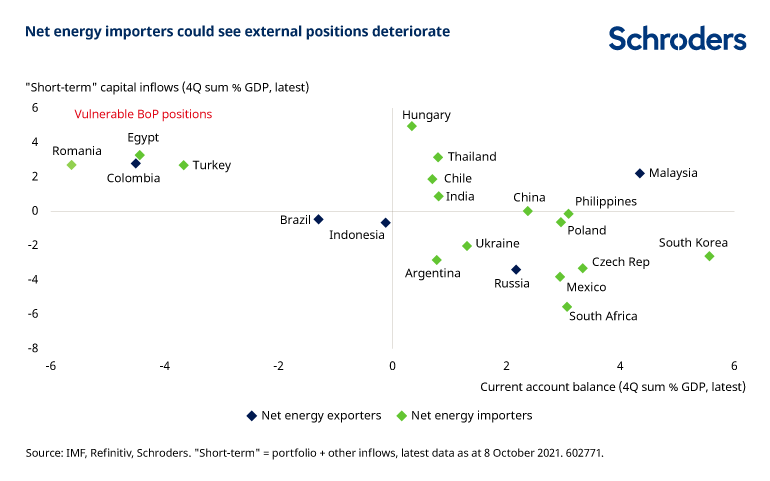

The good news from the perspective of external positions is that most EM enter the energy price spike with solid external positions. The Covid crisis and subsequent economic recessions saw imports plunge, resulting in most EM running current account surpluses. That leaves those that are net importers of energy, marked in the chart below in green, with room to absorb higher energy costs without creating worrying external imbalances.

The main exceptions are those EM marked in green in the top-left quadrant, which run current account deficits that are funded in large part by short-term capital inflows – Egypt, Turkey and Romania. These EM face the prospect of higher import costs at a time when Federal Reserve tapering, and concerns about stagflation and growth in China make financing conditions more tricky.

Persistent pressure on external positions in these EM would be likely to cause currencies to underperform. It would also force some retrenchment in domestic growth as financing conditions tighten and, in a worst case scenario, force interest rates higher to protect the capital account.

Although India enters the bout of higher energy inflation in relatively better shape, news that coal reserves have been depleted raises the risk that imports will need to increase, causing the current account to swing into deficit and putting pressure on the rupee.

My colleague Piya Sachdeva has looked in greater detail at the situation in India here: what are the risks from power shortages in India?

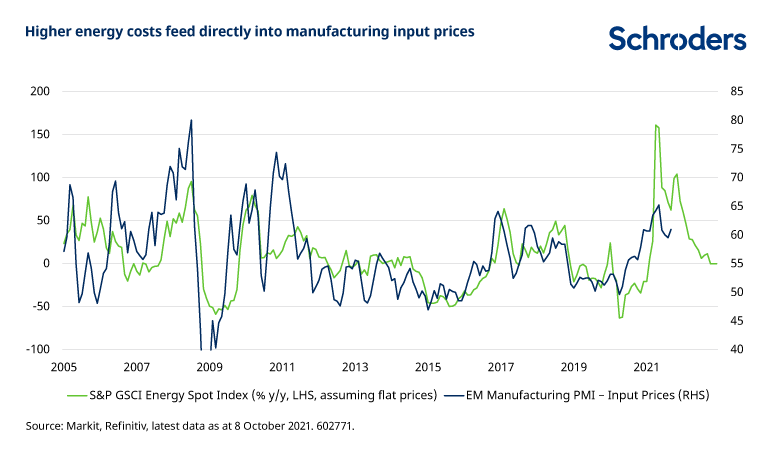

On the production side, as the chart below shows, higher energy costs mechanistically feed through into manufacturing costs, represented here by the input prices sub-component of the EM manufacturing PMI. Strong global demand for manufactured goods during the past 18 months meant that firms were able to pass on higher costs to consumers. However, if energy prices start to squeeze global demand as the world takes a more stagflationary tilt, this may be harder to achieve, putting pressure on margins.

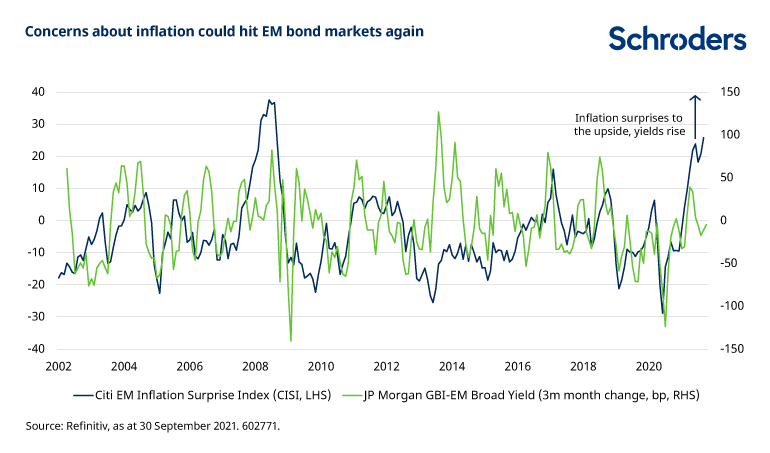

Finally, higher energy costs are a threat to inflation. Energy generally accounts for 5-10% of consumer price index (CPI) baskets across the emerging world. We previously noted, absent an increase in oil prices towards $90-$100 per barrel, energy inflation should fall back in EM as powerful base effects wash out of CPI data. With oil prices grinding towards those sort of levels, the outlook for energy inflation is now less benign. And an added complication comes from the surge in the price of natural gas, which will be a particular threat to CEE economies.

This raises the spectre that upside surprises to inflation could start to rattle bond markets again and extend the interest rate hiking cycle that has already got underway. Poland was the latest EM central bank to be drawn into tightening monetary policy last week.

—

Originally Posted on October 13, 2021 – What Higher Energy Prices Mean For Emerging Markets

The views and opinions contained herein are those of Schroders’ investment teams and/or Economics Group, and do not necessarily represent Schroder Investment Management North America Inc.’s house views. These views are subject to change. This information is intended to be for information purposes only and it is not intended as promotional material in any respect.

Disclosure: Schroders

Important Information: This communication is marketing material. The views and opinions contained herein are those of the author(s) on this page, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. It is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a reliable indicator of future results. The value of an investment can go down as well as up and is not guaranteed. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. Regions/ sectors shown for illustrative purposes only and should not be viewed as a recommendation to buy/sell. The opinions in this material include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realized. These views and opinions may change. Schroder Investment Management North America Inc. is a SEC registered adviser and indirect wholly owned subsidiary of Schroders plc providing asset management products and services to clients in the US and Canada. Interactive Brokers and Schroders are not affiliated entities. Further information about Schroders can be found at www.schroders.com/us. Schroder Investment Management North America Inc. 7 Bryant Park, New York, NY, 10018-3706, (212) 641-3800.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Schroders and is being posted with its permission. The views expressed in this material are solely those of the author and/or Schroders and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.