")

Many of us are familiar with the phrase “don’t let the facts get in the way of a good story.” It applies to many facets of life, but certainly to investing in so-called “meme stocks”. The latest news on AMC Entertainment (AMC) shows that the company’s management has decided to fully embrace, if not encourage meme stock traders. One can argue that this is even a prudent strategy. It’s hard to blame the management of a heavily indebted company of capitalizing upon a market mania to issue highly (ridiculously?) valued equity to help it replace expensive debt. Besides, who doesn’t like free popcorn?

The latest news from AMC is that they created a program called AMC Investor Connect, and one of the perks for shareholders will be free popcorn at the company’s theaters. The free popcorn has replaced a much more inconvenient item in the news cycle — though to be fair, traders didn’t seem to care anyway. On Tuesday, AMC sold $230 million worth of new shares to a hedge fund called Mudrick Capital in a private deal. In a more conventional company, investors might be concerned about potential dilution, but the stock rallied after traders decided that the benefits to AMC’s balance sheet outweighed the dilution. At least that’s a reasonable explanation it rallied – who knows if that was actually the Reddit mob’s thought process. Later that day, news reports stated that Mudrick Capital had already sold their shares for a tidy profit (no lockup, apparently), and called the shares overvalued. This had little effect on the stock price, mind you, but before the potentially negative story could dominate today’s news flow, traders were distracted by free popcorn.

AMC has been a serial issuer of stock over the past few months. Before yesterday’s private deal, they sold $407.3 million worth of shares on April 27th, and announced another offering of $50 million on December 11th. There were also small offerings in November and September of last year. In all these cases, it appears that management decided that the risk of dilution to current investors was outweighed by the company’s capital needs. That is an understandable and rational choice, particularly when we consider the following uncomfortable facts about the company’s balance sheet and profitability.

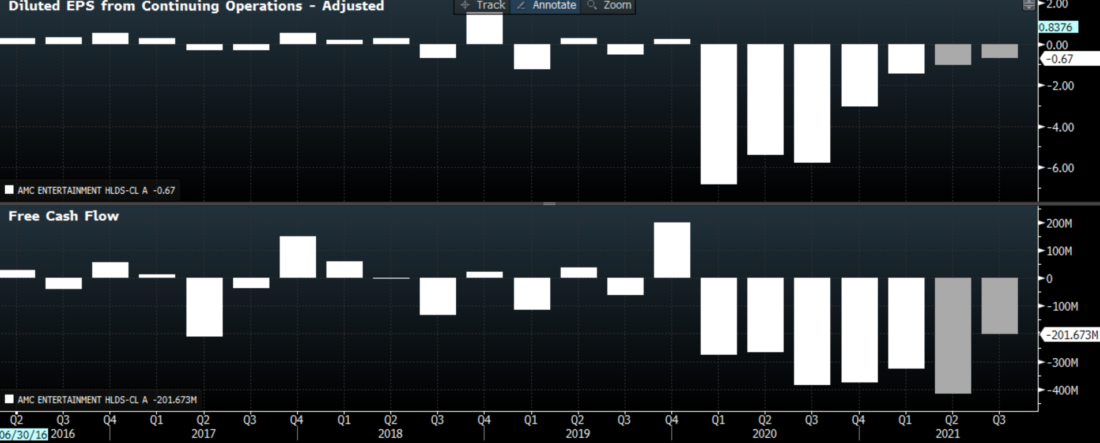

We all know how cinemas as a whole, and AMC specifically, were severely injured by pandemic-induced lockdowns. It is hardly surprising that a company that operates theaters would be dealt a massively negative blow when people were legally prevented from attending its venues. But the graphs below show that AMC was not a particularly profitable or cash-flow generating company even before the pandemic:

AMC Earnings per Share (EPS, top) and Free Cash Flow (bottom), 5 Years Quarterly (white) + 2 Quarters Analyst Consensus (grey)

Source: Bloomberg

The damage caused by Covid is readily apparent, but we can see that the company frequently alternated quarterly profits with losses, and had several quarters with negative free cash flow. Even under normal circumstances, AMC failed to demonstrate the type of consistent earnings, let alone growth, that investors crave. Bondholders, who are understandably more concerned with seeing positive cash flows that enable a company to service its debts, were also unimpressed. Even after the numerous equity capital raises, AMC bonds trade at highly distressed levels:

AMC Bond Details, Prices and Yields

Source: Bloomberg

We see that AMC bonds yield between 8% – 12.5%, which are significantly above those of investment grade corporate bonds. Bondholders are demanding to be compensated for what they deem to be a high risk to their repayment. It is important for equity investors to remember that bondholders get paid before equity holders in case of a default or bankruptcy. To be sure, the bonds are not trading at truly distressed levels, but it is clear that bondholders are hardly convinced that AMC is a thriving company. Call them boring or call them sober minded, but bondholders care only about whether they get paid back. Hype is meaningless unless they receive the interest payments they are due and their principal is repaid in full.

But we now see that the management of AMC has a very valid rationale for embracing and perhaps even encouraging the enthusiasm, if not mania, for the company’s shares. If there is a significant group of investors who are willing and eager to continue boosting the stock price, and the company is able to raise cheap equity capital that allows them to service its debts, management would be sensible to take advantage of that opportunity. (Let’s leave aside any benefit that accrues to management from stock ownership and options for now.) There must be a limit to a company’s ability to keep its stock meme-worthy enough to continue selling high-priced stock, but AMC hasn’t found it yet. For now, it is far more profitable to sell shares than movie tickets.

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Margin Trading

Trading on margin is only for experienced investors with high risk tolerance. You may lose more than your initial investment. For additional information regarding margin loan rates, see ibkr.com/interest