International tourist arrivals to Singapore rose in January to a new post-pandemic high, with over 930,000 visitors. The Singapore Tourism Board expects the nation to receive up to 14 million international visitors this year, more than double the 6.3 million recorded in 2022. Tourism receipts are also expected to grow from around S$14 billion in 2022 to as high as S$21 billion this year.

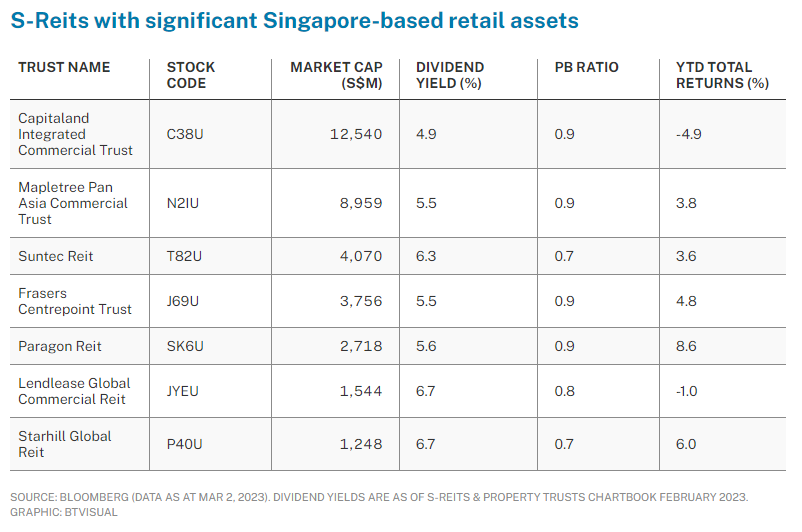

This may bode well for domestic consumer, leisure and hospitality-related sectors. Listed in Singapore are seven S-Reits that have significant exposure to Singapore-based retail properties.

CapitaLand Integrated Commercial Trust (CICT) for its FY2022 reported 25 per cent and 22.5 per cent year-on-year (yoy) growths in shopper traffic and tenant sales, respectively.

Downtown malls saw higher growth, with over 30 per cent increases in both shopper traffic and tenant sales. CICT noted that operating metrics in its retail portfolio surpassed pre-pandemic figures on the back of healthy market demand. Retail portfolio occupancy improved to 98.3 per cent as at Dec 31, 2022 (vs 96.8 per cent as at Sep 30, 2022) and positive rent reversion was recorded.

Mapletree Pan Asia Commercial Trust’s VivoCity Mall reported that its Q3 FY22/23 sales continued to exceed pre-pandemic levels, with shopper traffic and tenant sales growing 50.5 per cent and 38.5 per cent yoy, respectively. VivoCity recorded positive rent reversion at 7.9 per cent.

Suntec Reit reported 27.3 per cent and 38.8 per cent yoy growth in gross revenue and net property income, respectively, for its retail portfolio in H2 FY22. Growth was driven by higher occupancy, rent and advertising revenue at its Suntec City Mall. Overall retail portfolio committed occupancy improved to 98.1 per cent as at Dec 31, 2022 and the Reit recorded positive rent reversion at 4.4 per cent in FY2022.

Frasers Centrepoint Trust reported that shopper traffic and tenant sales in Q1 FY23 remained robust and grew 38.3 per cent and 13.4 per cent yoy, respectively. Retail portfolio committed occupancy improved to 98.4 per cent as at Dec 31, 2022 on healthy leasing demand.

Paragon Reit’s Paragon Mall saw sales recover to above pre-Covid levels as tenant sales for the January to December 2022 period increased 45 per cent yoy. Footfall was around 80 per cent of pre-Covid levels. The Clementi Mall remained resilient as tenant sales increased 12 per cent across the same period, with footfall gradually trending upwards post relaxation of pandemic restrictions.

Lendlease Global Commercial Reit’s retail portfolio maintained a portfolio occupancy rate of 99.5 per cent as at Dec 31, 2022, with positive rent reversion of around 2 per cent. The Reit noted that tenant sales and visitation in H1 FY23 surpassed pre-Covid levels and was five times and 2.8 times, respectively, what it was in H1 FY22.

Starhill Global Reit’s Wisma Atria saw tenant sales and shopper traffic improve in H1 FY23 by 32.6 per cent and 30 per cent, respectively, yoy. Overall portfolio occupancy rate of the Reit was at 97.1 per cent as at Dec 31, 2022.

In February, S-Reits posted negative 2 per cent in total returns (based on the iEdge S-Reit Index). Retail investors net bought the sector, totalling S$89 million in net inflows; while institutional investors net sold the sector, at S$42 million in net outflows.

REIT Watch is a weekly column on The Business Times, read the original version

—

Originally Posted March 6, 2023 – REIT Watch – Retail S-REITs’ metrics surpass pre-Covid; poised to benefit from tourism boost

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Singapore Exchange and is being posted with its permission. The views expressed in this material are solely those of the author and/or Singapore Exchange and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Alternative Investments

Alternative investments can be highly illiquid, are speculative and may not be suitable for all investors. Investing in Alternative investments is only intended for experienced and sophisticated investors who have a high risk tolerance. Investors should carefully review and consider potential risks before investing. Significant risks may include but are not limited to the loss of all or a portion of an investment due to leverage; lack of liquidity; volatility of returns; restrictions on transferring of interests in a fund; lower diversification; complex tax structures; reduced regulation and higher fees.