Code along Robot Wealth as they present an analysis of the SPY returns process using the QuantConnect research platform.

Excerpt

Example Research With QuantConnect Code

Using the QuantConnect ecosystem in a typical quant workflow.

Note: This code is meant to be used within QuantConnect research environment

# Import dependecies

import numpy as np

import seaborn as sns

import matplotlib.pyplot as plt

plt.style.use(‘ggplot’) #There is a positive correlation between chart pretiness and risk-adjusted returns

plt.rcParams[‘figure.figsize’] = [10, 7]

# QuantBook Analysis Tool

# Load SPY historical data

qb = QuantBook()

spy = qb.AddEquity(“SPY”)

history = qb.History(qb.Securities.Keys, 5000, Resolution.Daily) #5000 days of SPY daily data

# Drop pandas level

history = history.reset_index().drop(‘symbol’,axis=1)

# Calculate SPY returns and fillna

history[‘returns’] = (history[‘close’].pct_change() * 100).fillna(0)

1. Analysing the return distribution

Now that we have SPY daily returns let’s quickly see what we’re dealing with.

history[‘returns’].describe()

count 5000.000000

mean 0.030071

std 1.235997

min -11.638806

25% -0.443536

50% 0.061797

75% 0.573180

max 11.360371

Name: returns, dtype: float64

Let’s look at the extreme values of returns ie max and min

history[history[‘returns’] == min(history[‘returns’])]

history[history[‘returns’] == max(history[‘returns’])]

The recent corona drawdown is the biggest single-day market drop in history, and we have the biggest up move in 2008.

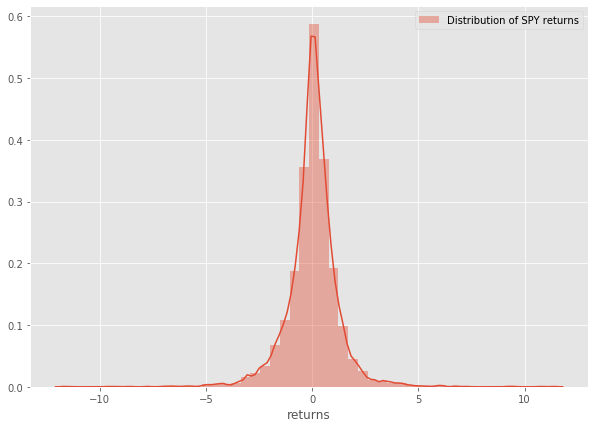

Let’s look at the distribution of daily returns for the SPY

sns.distplot(history[‘returns’],label=’Distribution of SPY returns’) plt.legend()

2. Comparing to a normal distribution

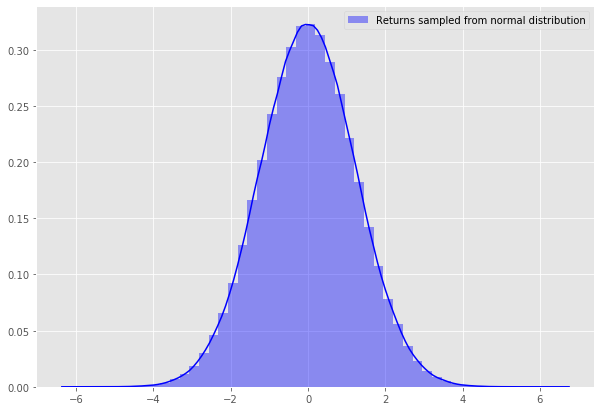

Let’s first create some random data and plot their distribution

random = np.random.normal(scale=1.23,size=500000)

sns.distplot(random,label=’Returns sampled from normal distribution’,color=’blue’)

plt.legend()

random_series = pd.Series(random)

There it is, a beautiful well behaved normal distribution, Let’s see how this compares to our SPY returns distribution.

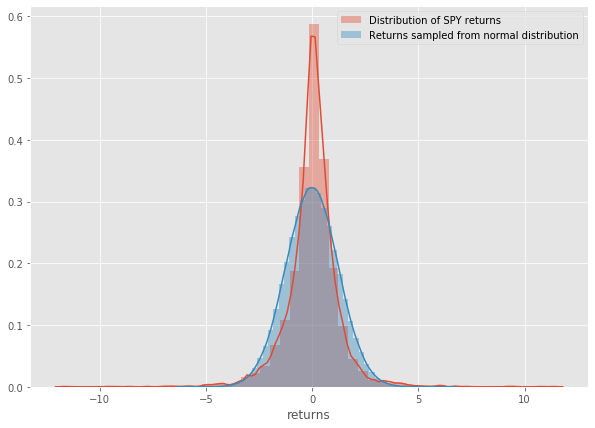

sns.distplot(history[‘returns’],label=’Distribution of SPY returns’) sns.distplot(random,label=’Returns sampled from normal distribution’) plt.legend()

Now the high kurtosis of the SPY returns becomes even more apparent.

So far we’ve learned that:

- SPY returns do resemble random returns

- but they have big tails in their distribution

- which means we can expect outsized moves to the upside and downside, more so than a normal distribution would suggest.

Now let’s look at a simple workflow for researching, seasonal patterns in our financial data.

Visit Robot Wealth to read the next steps Researching possible seasonal patterns and Looking for auto-correlation (trend) in the return process, and to download the sample code: https://robotwealth.com/how-to-be-a-quant-trader-experiments-with-quantconnect/

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Robot Wealth and is being posted with its permission. The views expressed in this material are solely those of the author and/or Robot Wealth and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.