CMT Association’s Market Insights features timely technical analysis of current global markets by veteran CMT charterholders. Each post appears on www.tradingview.com/u/CMT_Association/ in an effort to explain process, tools, and the responsible practice of technical analysis. Shared content and posted charts are intended to be used for informational and educational purposes only. The CMT Association does not offer, and this information shall not be understood or construed as, financial advice or investment recommendations. The information provided is not a substitute for advice from an investment professional. The CMT Association does not accept liability for any financial loss or damage our audience may incur.

Since credit has far greater potential to create systemic issues than does equity, corporate credit conditions are much more important to the Federal Reserve (Fed) than changes in equity prices. If you have interest in macro, monitoring and understanding the basics of corporate credit is a must have skill. If there is any one thing that might actually cause a Fed pivot , it is disfunction in this market.

There is a significant amount of current commentary around the sharply higher all-in-yields of high yield (HY) and investment grade (IG) corporate debt. In most cases the pieces conflate extreme price weakness in the large credit ETFs (HYG & LQD) with credit distress. Most pieces seem to conclude that the declines are linked to declines in credit quality and highlight financing problems in the sector. Most of that commentary suffers from a misunderstanding of the relationship between credit and Treasury spreads, what the price declines/yield increases are communicating about macro conditions, and how vulnerable companies, particularly IG companies, are being forced to refinance into a higher rate environment.

In February 2022 I published a piece on credit conditions that covered using the TradingView platform to monitor secondary market credit spreads and conditions, why the declines in most credit ETFs had nothing to do with credit quality, and the basics of monitoring credit on the platform. That piece is linked below.

The short course: 1) Corporates trade at a yield spread to treasuries. The spread compensates the corporate debt investor for the higher risk of default. 2) If Treasury yields rise, their dollar price declines. Since corporates trade at a yield spread to treasuries, if treasury yields rise, so do corporate yields (prices decline). 3) Since corporate spreads are generally far less volatile than Treasury yields, in most time periods, corporate total returns are driven by changes in Treasury yields rather than changes in corporate spreads. 4) The lower the credit quality, the wider the spread or default compensation. For instance, BBB rated corporates have more credit risk and thus more spread/yield above Treasuries than A rated bonds, 6.27 verses 5.65%. The difference of 62 basis points is the markets compensation (risk premium) for owning the riskier bond.

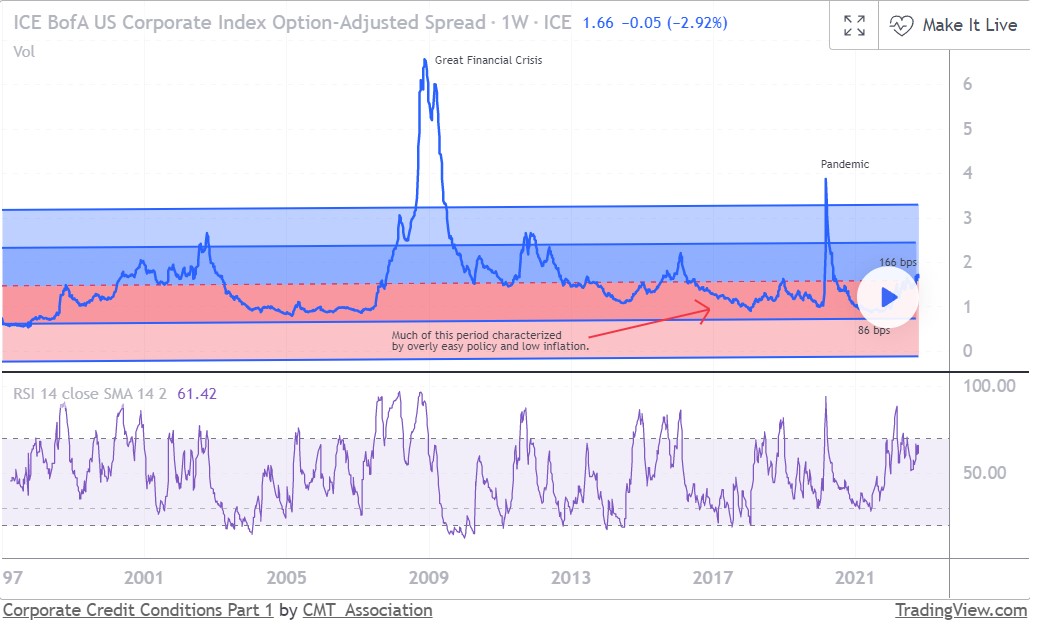

The chart is a weekly chart of the option adjusted spread ( OAS ) of the ICE BofA Corporate Index back to the 1997 index inception. OAS is the standard way of assessing the credit spread compensation over and above the Treasury rate. The higher the OAS , the more compensation the investor receives. The bands are plotted 1 and 2 standard deviations above and below the from inception date median value. The large spikes higher in 2008 and 2020 are the great financial crisis and the pandemic. Spread compensation is only now back to the long term median. This after spending most of the last decade trading nearly a standard deviation rich to the long term median. I view this as the residual of the Feds QE translating to richer than normal asset prices.

In short, there is no evidence of credit distress in the broad IG market. There is also, at least in this chart, no compelling value argument to be made. However, credit spread is only part of the equation. Remember that corporate total returns are more a function of changes in base or treasury rates than in changes in corporate spreads.

In the next installment we will focus on the IG and HY markets in detail, some fundamental observations and finally, the correlation between rates and the major credit ETFs.

And finally, many of the topics and techniques discussed in this post are part of the CMT Associations Chartered Market Technician’s curriculum.

—

Originally Posted November 2, 2022 – Corporate Credit Conditions Part 1

Shared content and posted charts are intended to be used for informational and educational purposes only. The CMT Association does not offer, and this information shall not be understood or construed as, financial advice or investment recommendations. The information provided is not a substitute for advice from an investment professional. The CMT Association does not accept liability for any financial loss or damage our audience may incur.

Disclosure: CMT Association

Shared content and posted charts are intended to be used for informational and educational purposes only. The CMT Association does not offer, and this information shall not be understood or construed as, financial advice or investment recommendations. The information provided is not a substitute for advice from an investment professional. The CMT Association does not accept liability for any financial loss or damage our audience may incur.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from CMT Association and is being posted with its permission. The views expressed in this material are solely those of the author and/or CMT Association and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.