As usual, markets had a major move while I was on vacation last week. It is always tempting for me to buy VIX calls just before I leave, but in this case the Cboe Volatility Index is almost exactly at the 21.63 level it was before my ski trip. Good conditions made it easier to temporarily wean myself from my usual firehose of financial news – though I was riveted by the Congressional hijinks during off-mountain hours – but it was impossible to ignore the immense reaction to Friday’s payrolls report. Markets are hoping desperately for a soft landing, and Friday’s data dump was as welcome for investors as Utah’s sequential powder dumps were for my fellow skiers.

Without belaboring Friday’s statistics, it was clear that investors were quite pleased that even though payrolls were higher and unemployment lower, wages rose by less than expected. The initial reaction may have been a bit of a “glass half full” read to the December numbers, but a solid labor market that fails to ignite inflationary pressure is indeed a key element of the soft-landing thesis. The subsequent ISM Service report got an even more charitable interpretation. The headline number missed substantially, dipping to 49.6 when 55 was expected, but the prices paid number fell modestly. A drop below 50 in an index of this type indicates contraction, but the die had already been cast. Bond yields rightly plunged, and stock traders were quite inclined to follow that lead.

At a gut level, the rally was quite understandable. It is not unusual for equity markets to rally around the start of a new year, and after spending two weeks mired in a relatively tight trading range, we were likely to break out in one direction or another. We also see leadership in names that were some of last year’s biggest laggards. Their declines into year-end were likely exacerbated by tax-loss selling. The turn of the calendar removes that motivation. See the recent outperformance of Meta Platforms (META) for one example.

That said, today’s continuation of Friday’s rally is a welcome development. Last year we had more than our share of one-day wonders – days when major indices jumped on a positive news item only to give back those gains over subsequent sessions. We noted often that bear market rallies are short, sharp and ferocious, and while it is indeed far too early to say that this two-day bounce is anything other than another bear market rally, the strong follow-through is constructive.

Yet this could also be another case of investors’ selective hearing. Even as markets were soaring, they seemed to ignore comments from three key Fed voices (Bostic, Barkin, Cook) that inflation remained well above their comfort levels, implying that they are at odds with the Fed Funds futures’ continued expectations for peak rates below 5% with rate cuts beginning in the second half this year. Perhaps a bit of perspective is required.

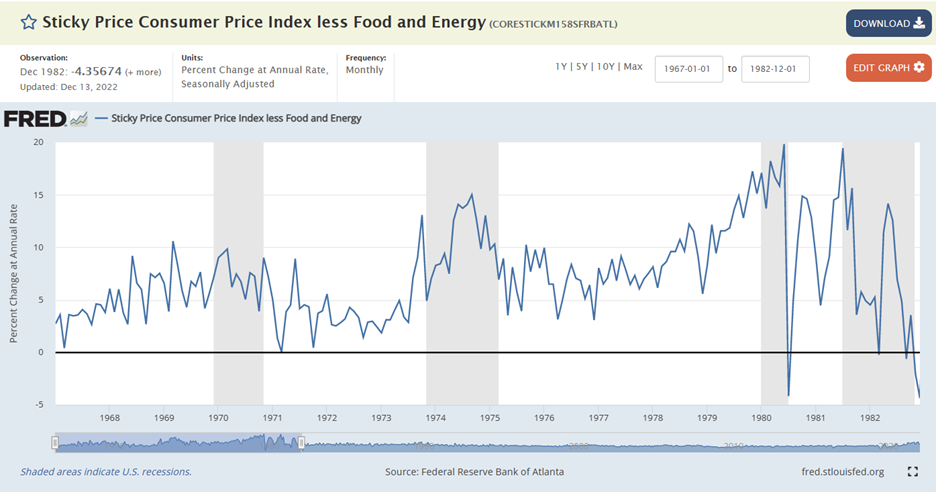

Chair Powell and his colleagues have been quite consistent in their rhetoric about continuing to fight inflation, even if it risks affecting unemployment and economic growth. The latest unemployment reading of 3.5%, and the Atlanta Fed’s GDPNow estimate for 4Q GDP is currently 3.8%. Neither is hardly an impediment to the inflation fight. More importantly, it is useful to remember that an improving pace of inflation is a necessary but hardly sufficient condition for a return to the Fed’s 2% target. The slowing pace of inflationary gains is the second derivative of price levels, with inflation – the rate of change of prices — being the first derivative. The historical experience of the 1970s shows us that inflation rates can decline frequently and sometimes precipitously even as the levels of inflation remain uncomfortably high. The following graph shows the monthly CPI changes on an annualized basis. The rate reverted to nearly zero in the wake of President Nixon’s wage and price freeze in 1971, but then stayed consistently around 5% or more in the latter half of the decade.

Source: fred.stlouisfed.org

For example, note the big drop in late 1978. The annualized inflation rate was halved in that timeframe, though it remained uncomfortably high. Also, even as Fed Chair Volcker’s policies in the early 1980’s finally tamed the worst of the prior decades inflation, there were still periods when inflation rebounded. It is hard to believe that these lessons are lost on today’s policymakers.

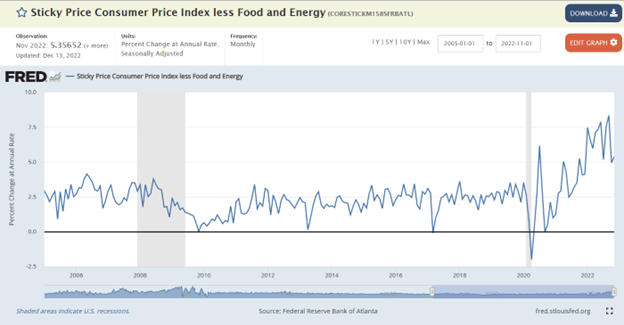

Compare that period to the current one, shown in the graph below. We have been spoiled by over a decade of stable inflation and few recessions. Yet even though we have seen some recent declines in the annualized monthly CPI inflation data, it is clearly above the desired levels and trend. We may yet get a soft landing – even if the recent news from consumer stocks like Lululemon (LULU) and Macy’s (M) seem to indicate otherwise – but in any event, it seems premature to test the Fed’s resolve about rates.

Source: stlouisfed.org

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Options Trading

Options involve risk and are not suitable for all investors. Multiple leg strategies, including spreads, will incur multiple commission charges. For more information read the "Characteristics and Risks of Standardized Options" also known as the options disclosure document (ODD) or visit ibkr.com/occ