Economic updates released today and Federal Reserve Chairman Jerome Powell comments paint a somewhat favorable outlook for the war on inflation, but investors are reacting to the developments with mixed emotions as they examine the demand picture.

Yesterday, Powell hinted at continued rate increases, additional balance sheet reductions and a likely higher-than-anticipated terminal rate, but investors focused on his comments about the central bank moderating the pace of rate hikes and the Chairman’s belief in the ongoing possibility of a soft landing. This optimism and accompanying equity rally were sustained early this morning by the Core PCE Index showing a slight moderation in inflation. Sometimes, however, good news is followed by bad news, at least in the eyes of investors who reacted negatively to this morning’s ISM Purchasing Managers’ Index (PMI). The PMI contracted for the first time since the spring of 2020 against the backdrop of weak new orders, employment and prices. While the ISM has dampened investor sentiment by pointing to future declines in corporate earnings, its weakness implies that the Federal Reserve’s rate hikes are weakening demand for products and services, thereby providing additional fodder for optimism that the central bank will slow its rate hikes. The PCE and ISM reports are providing mixed signals as investors grapple with focusing on either slower inflation and lower yields or slower demand and reduced earnings. Equities are now giving back some of the gains from yesterday, with yields and the dollar down as well.

Today’s PMI of 49 was the lowest level since the 43.5 seen during the depths of the COVID-19 pandemic in May 2020. Today’s number fell short of consensus expectations for a 49.8 reading and was worse than October’s 50.2 level. The report confirms the deterioration of manufacturing, which we covered last week in our commentary, “Manufacturing Slips Deep into Contraction Territory While Layoffs Rise Markedly” based on the PMI flash release from S&P Global. In today’s ISM report, new orders slipped further into contraction territory, employment entered contraction land and prices fell to the lowest index level since May 2020, illustrating deflationary pressures in goods but sparking concerns about earnings and economic growth prospects.

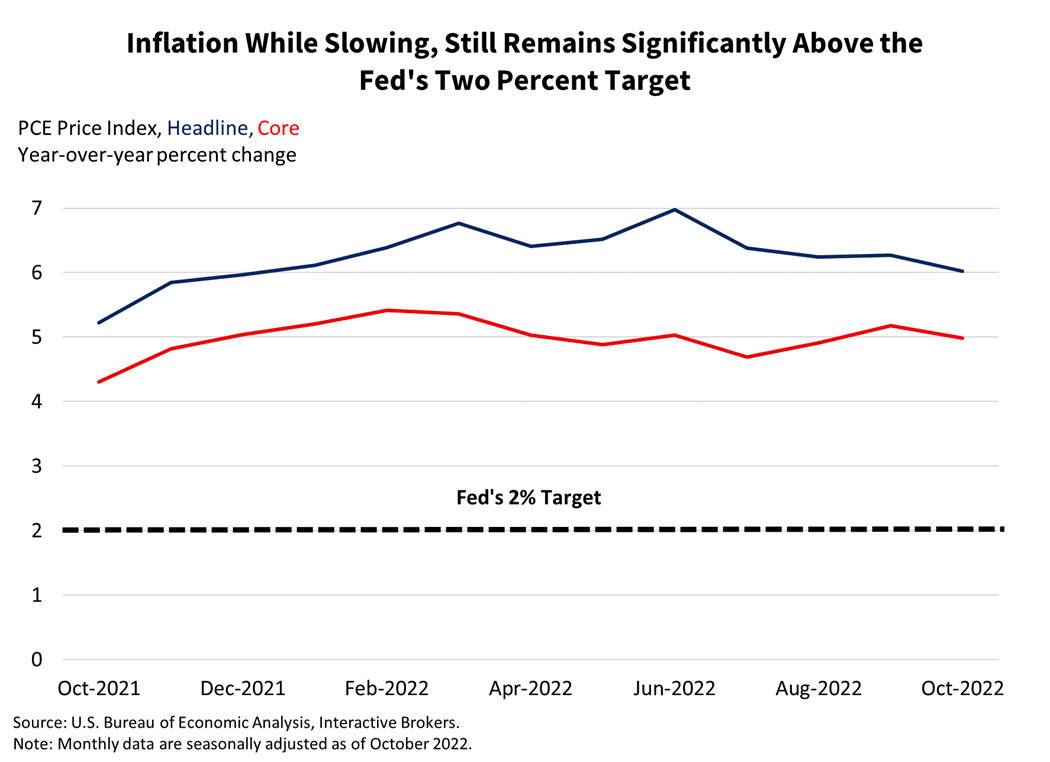

The Core PCE Price Index climbed 5.0% year over year (y/y) and 0.2% month over month (m/m) in October, near market expectations of 5.0% and 0.3%, respectively, and cooler than September’s readings of 5.2% and 0.5%. The general PCE Price Index, which includes food and energy, increased 6.0% y/y and 0.3% m/m.

The PCE also showed that personal income increased 0.7% versus the 0.4% consensus expected, while personal spending came in-line at 0.8%. This increasing spending rate is unlikely to be sustainable for various reasons:

- Spending continues to outpace income, and the personal savings rate remains severely depressed at 2.3%, the lowest level since 2005.

- Some consumers are spending savings resulting from a once-in-a-lifetime opportunity to accumulate wealth—lockdowns and stay-at-home orders enacted to slow the spread of Covid.

- Consumers are also increasing their credit card debt. With floating interest rates, monthly credit card payments are likely to become unstainable for some consumers as rates increase.

- Consumers are also increasingly using home equity lines of credit. Like credit cards, home equity loans have floating interest rates that will increase as interest rates increase.

- Wage increases are trailing the pace of inflation, reducing the amount of discretionary income.

Chair Powell acknowledged that housing and goods prices are softening considerably while the threat of persistent inflation is coming from labor-intensive services. To bring inflation down he implied, labor market weakness would be needed to bring it back to equilibrium. Excess retirements have contributed to too many job openings, fueling wage growth as businesses need to pay more to get prospective workers into the door. Wage growth is rising too fast and is not consistent with 2% inflation. His goal is to dent job openings without increasing the unemployment rate; however, the Fed’s tools lack the precision to target one economic indicator without affecting the others. In my view, a failure to bring down services inflation and job openings would result in inflation being stuck at 3.5 to 4%, a level too high relative to current market pricing. For now, however, investors will need to grapple with whether inflation is coming down due to declining demand or due to rising efficiencies, economic indicators point to the former. Further downside in equities may occur alongside falling yields, as demand destruction and contracting earnings take center stage while Powell and the Fed rest in the bullpen for a few innings.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.