In good news for consumers and the Federal Reserve’s aggressive inflation war, consumer price increases, while still high, were cooler than expected in October. The overall Consumer Price Index (CPI) released this morning climbed 7.7% from the same month a year ago compared to the anticipated 7.9% increase. While 7.7% is still substantial, the data release includes various reasons for optimism and have shored up investment sentiment about the possibility of the Federal Reserve (the Fed) taking a smoother approach to rate tightening in the coming months. Investors reacted by bidding up equity prices while bond yields declined. Despite this improving inflation sentiment, I believe the Fed still needs to maintain a hawkish stance that will make a soft landing unlikely.

From an optimistic perspective, the Core CPI, the services sector and annualized inflation rates show substantial moderation in price gains.

- Core CPI, which excludes the highly volatile food and energy components, climbed 6.3% year over year (y/y) in October, better than the anticipated 6.5% increase. It registered a 0.3% month over month (m/m) increase.

- Services less energy prices gains climbed only 0.5% m/m compared to the 0.8% rate in last month’s report.Services include food away from home, medical care, transportation services and shelter which have shown stubborn prices increase. For example, while September’s Core Personal Consumption Expenditure (PCE) index climbed 0.5% m/m and certain consumer goods prices declined, services increased 0.6% m/m. Inflation for services as measured by both the CPI and PCE have been persistent as consumers shift spending away home goods and toward entertainment, restaurants, travel and other services as the COVID-19 winds down.

- Inflation on an annualized rate based on October’s m/m CPI change is also encouraging. The monthly gain points to a 4.8% annualized rate for the overall index and 3.6% for the Core CPI, a lot closer to the Fed’s 2% target. Just last month, core CPI was 0.6%, an annualized rate of 7.2%. While inflation is still hot overall, progress in the core areas is certainly encouraging.

Expectations of Fed tightening moved down significantly this morning, with the market now strongly expecting a 50 basis point (bp) hike at the December meeting. Odds of a 75 bp hike in December moved down to 14% while odds of a 50 bp increase climbed to 86%. Just a few weeks ago during the last week of October, odds favored a 75 bp hike after hot inflation readings trampled hopes of a quick pivot from aggressive tightening. Driven by a reduction in inflation expectations and a less tight Fed, yields retreated significantly in a bull steepening motion, with 2s and 10s down 28 and 21 basis points respectively. The drastic downward shift in Fed tightening expectations may pave the way for a Santa Claus equity market rally into year-end.

A Formidable Challenge Persists

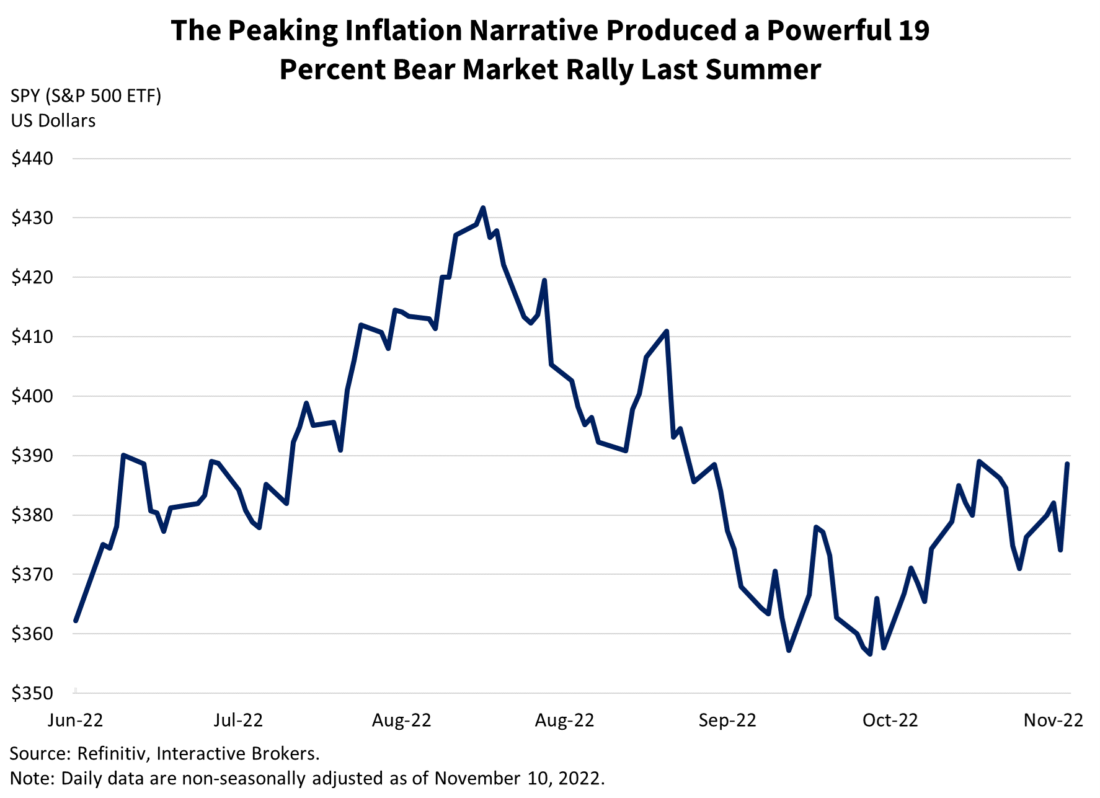

While a strong bear-market rally is likely after this report against the backdrop of what is typically a robust seasonal period for equities as the year winds down, an important question to consider is whether prices are coming down due to rising efficiencies or due to demand destruction. It would be great news if prices would come down while consumer demand remained strong, but unfortunately, I don’t think that’s the case. Importantly, efficiencies are unlikely to improve as weak sentiment among executives has curtailed business capital expenditure expectations while corporations are struggling with a shortage of workers, wage pressures, and high interest rates. Revenue guidance from the Street and declining earnings expectations for 2023 point to a burdened consumer and a deteriorating economy driving price declines due to reduced demand rather than greater efficiencies. While the market cheers a great inflation report, it’s important to remember the 19% bear market rally in August that was driven by slower inflation readings driven mainly by only category: gasoline.

Want to learn more about what goes into the Consumer Price Index report? Watch here at Traders’ Academy

—

This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice. Interactive Brokers LLC is a member of NYSE, FINRA, SIPC.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: ETFs

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.