Summary: Sugar production is being disrupted in various parts of the world, intentionally and unintentionally. Production is falling on a global level, as are stockpiles. Meanwhile, the United States, facing a supply deficit is on track to import more sugar this year than it has in almost four decades. All those factors, combined, could push sugar prices higher in 2020, creating an opportunity for investors to generate alpha.

The price of sugar has experienced some serious ups and downs this decade, and investors are hoping to embark on another dramatic “up cycle” like the one that occurred between mid-2015 and mid-2016. Sugar’s price doubled during that period, although those gains completely evaporated over the following two years due to a supply glut.

Weather patterns, Brazil’s allocation of its sugar crop to ethanol production, and the US dollar’s movement relative to the world’s currencies are usually strong contributors to sugar’s price swings. This year is proving to be no different.

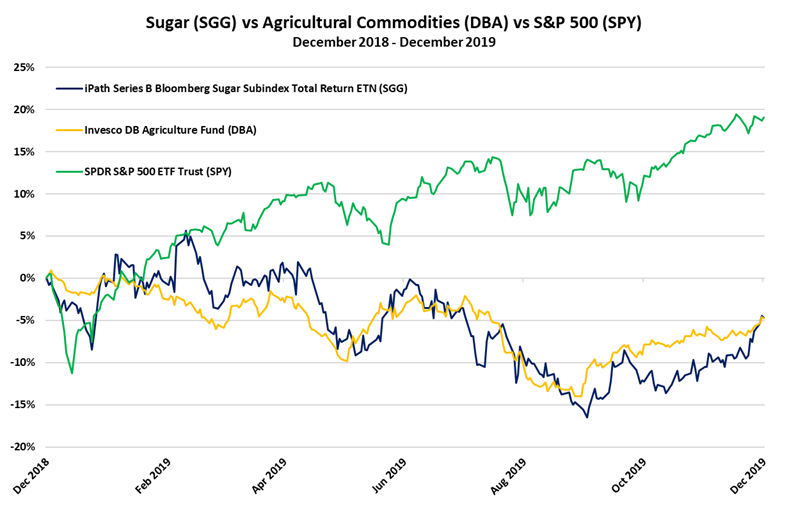

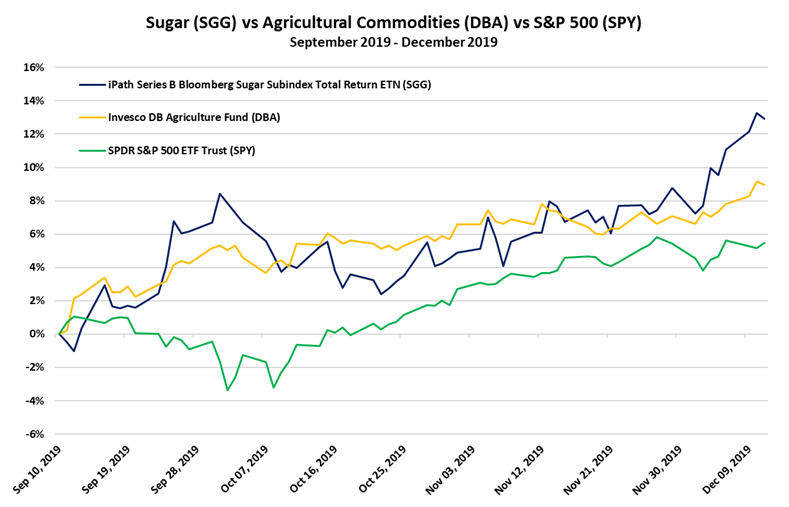

Sugar prices have risen 18% over the past three months, supported by reduced production in Brazil and India, the #1 and #3 exporters in the world, and a developing supply squeeze in the United States, which is a huge consumption market for sugar.

Drop in India’s 2019 Sugar Production & Stockpiles

Maharashtra, India’s second-biggest sugar producing region, faced an unusual situation this year. The price of cattle feed rose so much that it became more profitable for farmers to sell their sugar cane as cow fodder than to process it into sweetener. Many farmers ended up selling their cane as cattle feed, leading to a drop in India’s sugar production.

The United States Department of Agriculture (USDA) puts out a monthly report on the world’s sugar market and trade. Last month’s report showed a 15% decline in India’s production, from 34.3 million tons in the season 2018/19 to 29.3 million tons this new season. A 15% decline in India’s sugar stockpiles is reflected as well, which should be supportive of global sugar prices.

Brazil’s Record Shift to Ethanol

Brazil is responsible for one third of the world’s sugar exports, per the November 2019 USDA report on sugar, so any production or export declines in that market can affect global prices. Crude oil prices have been higher on average these past couple of years (December 2017 – December 2019) than during the preceding three years (December 2014 – December 2017). Higher oil prices have made ethanol more competitive than gasoline for Brazilian drivers.

As ethanol demand boomed, so too did ethanol prices, prompting Brazil’s farmers to dedicate a bigger share of their sugar cane crop to the production of the fuel rather than to the sweetener. That shift partially explains the two-year decline in Brazil’s sugar exports. During the upcoming 2019/20 season, Brazil is forecasted to export 18.6 million tons of sugar. That’s 5% less than last season and 34% less than the 2017/18 season.

Supply Deficit in the United States

Half of the sugar produced in the United States comes from sugar beets, grown mainly in upper Midwest states like Minnesota, North Dakota, Colorado, and Montana. The other half of the country’s sugar is derived from sugar cane grown in warmer states like Florida, Hawaii, Louisiana and Texas. This year was particularly bad for both the sugar beet and sugar cane harvests due to inclement weather.

As a result, the US beet harvest for 2019-20 will be at least 10% lower than last year, while the sugar cane harvest will be 3-4% lower. Due to the production deficit, the US has had to increase its sugar imports to meet domestic demand, a trend that will continue into 2020.

Economists at the Agriculture Department estimate that meeting the domestic demand for sugar will take 3.86 million tons of imported sugar, the greatest amount to be imported since 1981. Meanwhile, US stockpiles are expected to shrink to 1.166 million tons, marking the lowest level in at least two decades and a decline of 28% from 2018/19.

Winner and Losers

The three developments mentioned above are positive for the sugar market. Lower exports and stockpiles in countries like India and Brazil help to tighten global supplies and support higher prices, benefitting those same countries.

An additional consideration that would help sugar prices would be some weakness in the US dollar. The buck’s strength in recent years has weighed on commodity prices including sugar. Any strides towards reducing trade tensions should contribute to a softer dollar. In turn, any moderate weakening of the greenback could boost sugar futures due to the inverse correlation between the dollar and commodity prices.

The biggest impact from lower US production, meanwhile, will really be felt by companies that profit from increased US sugar imports — namely, foreign exporters that are able to send more sugar into the United States, and domestic refiners that process incoming cane into sugar.

Winners are US Sugar Cane Refineries: The imports into the United States will be raw product from sugar cane (rather than beets) which can only be processed at a handful of refineries in coastal locations such as Savannah, Ga., Baltimore and New York City, according to Frank Jenkins, a sugar market expert and head of JSG Commodities.

The USDA’s December 10 report on World Agricultural Supply and Demand Estimates shows US cane sugar production hitting 3.91 million tons for 2019/20. Adding projected imports of 3.86 million tons to that number essentially doubles the amount of cane sugar product that will need to be refined. Those coastal factories don’t usually see this much business in a typical year, so the extra volumes would represent a big win for them if they can ramp up their capacity utilization.

Winners are Mexico’s Sugar Exporters: While there are plenty of countries that can supply the United States with sugar, including Brazil, Thailand, France and India, most of the shipments will likely come from Mexico, because trade agreements give Mexico first dibs on the American market. As such, Mexico’s sugar exporters are potentially big winners in the coming year, especially with the added support of USMCA behind them.

While total US imports for the 2019/20 season are projected to rise by 26% year-on-year (from 3.07 million tons to 3.86 million tons), imports from Mexico are projected to rise by a whopping 83% (from 1 million tons to 1.83 million tons), according to the USDA’s December 10 report.

Brazil is ranked second (after Mexico) among countries from which the US imports sugar. As such, Brazil could also benefit next year, seeing that Mexico is projected to supply just half of the imports needed.

Losers are producers and processors of beet sugar: Rising commodity prices are usually bad for manufacturers that require the material to produce their end products. And US food and beverage companies are certainly paying more for their sugar lately, as prices have risen 18% since September. Still, with sugar trading on the commodity markets at $0.13 per pound — which is 30% lower than three years ago and 60% lower than ten years ago — and companies able to bring sugar in from elsewhere, prices would have to rise significantly more before denting into the profits of candy-makers, bakers, and other commercial users.

The most pain will be felt by domestic entities that will lose business because of the bad harvests. This includes the growers that suffered crop losses (some farmers lost more than a third of their harvest) and processors with less product to refine into sugar. Two major distributors of sugar, including United Sugars Corp., took the rare step of declaring “force majeure,” a legal term that companies invoke when they cannot honor a contract due to circumstances outside their control.

How to Invest in Sugar

Investors seeking exposure to sugar in the commodity markets can get it via the iPath Series B Bloomberg Sugar Subindex Total Return ETN (SGG), which launched in January 2018, or via the older but smaller Tecrium Sugar ETN (CANE). Both ETNs track an index of sugar futures contracts.

Sugar vs Agricultural Commodities vs S&P 500

Questions, comments or learn more about subscribing to MRP, contact – Rob@mcalindenresearch.com/646-964-6152.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from McAlinden Research Partners and is being posted with its permission. The views expressed in this material are solely those of the author and/or McAlinden Research Partners and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.