AT A GLANCE

- Traditional oil refiners, which historically generated their income from fossil fuels, have turned their attention to renewable diesel.

- Soybean oil is the largest vegetable oil globally and has drawn attention for its use in greater quantities to help meet more stringent environmental mandates.

The stated global ambitions by nations to reduce their use of fossil fuels is seeing a rise in the demand for more sustainable energy sources and biofuels appears to be at the forefront of the change.

The International Energy Agency (IEA) has stated that the global production of biofuels could reach 300 million tons by 2030, a staggering three-fold increase from current levels. An annual production growth of 3% up to 2025 is expected, the IEA says in its latest biofuels report. Future production growth of 3% falls short of the IEA’s sustainable development scenario where a 10% growth rate will be required to meet the commitments on clean energy, the IEA added.

The U.S and Europe are widely leading the charge on the production of key biofuels and on the production of even lower carbon feedstocks such as renewable diesel (RD) in the U.S. or hydrotreated vegetable oils or HVO across Europe. Traditional oil refiners, which historically generated their income from fossil fuels, have turned their attention to the production of renewable diesel. Part of this change is being driven by more stringent environmental regulations but also on the softer demand outlook for fossil fuel based refined products.

Soybean Oil’s Pivotal Role

Soybean oil is the largest vegetable oil globally, and this has drawn the attention of some of the world’s largest refiners to use it in greater quantities to help meet more stringent environmental mandates. Soybean oil is widely used in the U.S and is increasingly being used in the international markets as refiners look for feedstocks at scale to meet the growing challenge to reduce carbon emissions.

Read More About Soybean Oil Futures

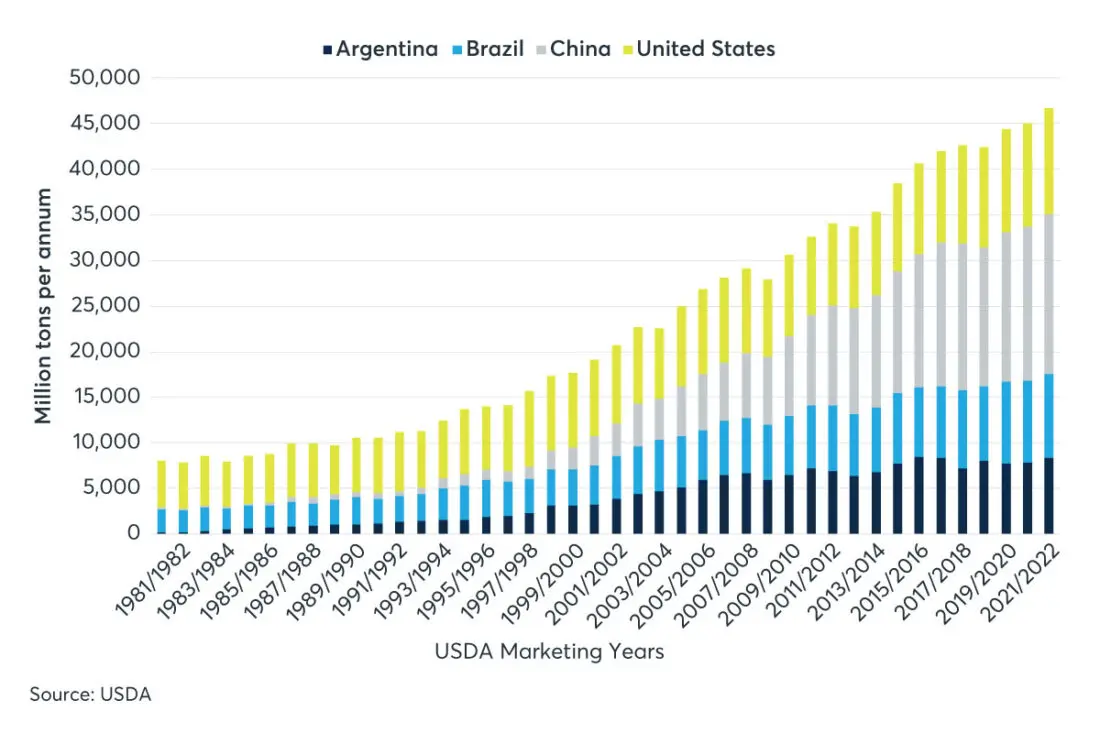

The U.S., China, Brazil and Argentina are the largest producers of soybean oil on the global stage with a total production volume of 46.6 million tons in the latest 2021-2022 marketing year, USDA data shows.

Chart 1: Global powerhouses in the soybean oil market

The Soybean Crush Spread

The Soybean crush industry is also undergoing significant change, partly to meet the growing demand for RD and HVO, as the oil which comes from the crushing process remains a key feedstock. Soybean crushing is the process of transforming whole soybeans into both soybean meal and soybean oil.

Soybean meal is used as a high-protein animal feed whilst soybean oil is a vegetable oil used in various industrial applications such as renewable diesel or HVO. Soybean oil when measured as a percentage of the crush spread has risen in recent months and now accounts for around 50% of the crush spread, incentivising the greater production of soybean oil to meet growing demand where possible. Soybean meal supplies have also been rising, leading to some to question what the world will do to process the greater quantities of soybean meal becoming available.

When a bushel of soybeans weighing 60 pounds is crushed, the conventional result is 11 pounds of soybean oil, 44 pounds of 48% protein soybean meal, four pounds of hulls and one pound of waste. To compare soybean oil with meal prices, the common method is to convert the soybean oil futures price per 11 pounds and convert the soybean meal futures price to the price per 44 pounds which reflect the outputs from crushing one bushel of soybeans.

All About Carbon Intensity

The measurement of carbon intensity (CI) of a particular feedstock will drive the choice of which feedstock to use to produce the finished product. In the U.S. the Low Carbon Fuel Standard (LCFS) is a centerpiece of U.S. greenhouse gas targets for transportation fuels. European regulators are increasingly moving towards carbon intensity and greenhouse gas emission targets as a way of reducing the impact of fuel choice on the environment. The latest E.U regulation package, referred to as the “Fit for 55” aims to reduce net greenhouse gas emissions by 55% by 2030 from 1990 levels.

Under the LCFS, producers that deliver low CI fuels to a buyer will typically receive a credit based on the CI of a particular feedstock source that the fuel is made from. First generation biofuels, such as those derived from virgin soybean oil or other equivalent vegetable oils typically have a higher CI compared to other more sustainable feedstocks such as used cooking oils or animal fats.

However, one such issue is around feedstock availability at scale, which is expected to become worse as production capacity increases with refiners chasing the same feedstocks in greater numbers. California has a stated aim of reducing the CI of transportation fuels by at least 20% by 2030. This is one reason why producers have turned to the U.S. vegetable oil markets to procure the required volume of feedstock to help achieve this aim.

Chart 2: U.S Renewable Diesel supply growth is robust

Vegetable oils look set to play an important role alongside other sustainable feedstocks like waste cooking oils and animal fats as governments gear up for meeting their stated net zero emission targets by 2050. The role of renewable diesel and hydrotreated vegetable oils is going to grow in the coming years and these products alongside existing biofuel markets will contribute to the overall expected production volumes of 300 million tons by 2030.

Sourcing sufficient volumes of lower carbon feedstocks is expected to remain a challenge for both producers and blenders and this may result in greater volatility in feedstock prices. The financial risk management in markets like soybean oil and other related markets is going to be increasingly important to deal with an increasingly volatile price scenario and this will continue to attract new players into the market as they aim to scale up their renewable energy output.

—

Originally Posted on November 4, 2021 – Biofuels Thrive on Net Zero Carbon Ambitions

OpenMarkets is an online magazine and blog focused on global markets and economic trends. It combines feature articles, news briefs and videos with contributions from leaders in business, finance, economics and politics in an interactive forum designed to foster conversation around the issues and ideas shaping our industry.

All examples are hypothetical interpretations of situations and are used for explanation purposes only. The views expressed in OpenMarkets articles reflect solely those of their respective authors and not necessarily those of CME Group or its affiliated institutions. OpenMarkets and the information herein should not be considered investment advice or the results of actual market experience.

Neither futures trading nor swaps trading are suitable for all investors, and each involves the risk of loss. Swaps trading should only be undertaken by investors who are Eligible Contract Participants (ECPs) within the meaning of Section 1a(18) of the Commodity Exchange Act. Futures and swaps each are leveraged investments and, because only a percentage of a contract’s value is required to trade, it is possible to lose more than the amount of money deposited for either a futures or swaps position. Therefore, traders should only use funds that they can afford to lose without affecting their lifestyles and only a portion of those funds should be devoted to any one trade because traders cannot expect to profit on every trade.

BrokerTec Americas LLC (“BAL”) is a registered broker-dealer with the U.S. Securities and Exchange Commission, is a member of the Financial Industry Regulatory Authority, Inc. (www.FINRA.org), and is a member of the Securities Investor Protection Corporation (www.SIPC.org). BAL does not provide services to private or retail customers.

In the United Kingdom, BrokerTec Europe Limited is authorised and regulated by the Financial Conduct Authority.

CME Amsterdam B.V. is regulated in the Netherlands by the Dutch Authority for the Financial Markets (AFM) (www.AFM.nl).

CME Investment Firm B.V. is also incorporated in the Netherlands and regulated by the Dutch Authority for the Financial Markets (AFM), as well as the Central Bank of the Netherlands (DNB).

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from CME Group and is being posted with its permission. The views expressed in this material are solely those of the author and/or CME Group and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.