S&P rising triangle pattern. Resolution likely higher, but probability fades if not soon.

Silver cup and handle developing out of inverse head and shoulders.

Gold back and fill. Retesting previous resistance, now rare major four-star support.

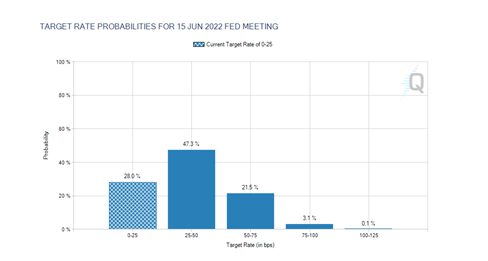

Probability of a Fed hike by June is now 72%. On heels of Clarida comments Friday.

Market Activity

– Global equity markets mixed to flat, but U.S. equity benchmarks extend gains led by Tech. Fresh record highs in the NQ for the third straight session.

– S&P had a soft finish from highs Friday after hawkish comments from Fed Vice-Chair Clarida; taper timeline can be reevaluated at the December meeting.

– People’s Bank of China left rates unchanged but dropped hawkish verbiage from statement, alluding to willingness to stimulate if needed. PBOC has been adamant about controlling inflation.

– Austria enters full lockdown. Violent protests breakout across Europe against Covid lockdowns.

– Risk-assets had moved lower early Friday on Europe lockdown fears, but German Foreign Minister said full/broad lockdown unlikely and losses were quickly pared.

– We have been highlighting case counts in Germany for weeks, this will be ever important. Rise in cases subdued over the weekend, typical though.

– White House is throttling out SPR, asking Asian nations to join. Japan indicated willingness to follow.

– Chicago Fed National Activity due at 7:30 am CT and Existing Home Sales follow at 9:00 am CT.

– Europe and U.S. Flash PMIs tomorrow, as well as 7-year Note auction.

E-mini S&P (December) / NQ (December)

S&P, yesterday’s close: Settled at 4694.50, down 7.00 on Friday and up 16.25 on the week

NQ, yesterday’s close: Settled at 16,575, up 93.75 on Friday and 382.25 on the week

– S&P and NQ working to define higher floors. The S&P solidified 4667-4669 last week on two tests. Recurring level 4684.75-4685.50 would be next in line. The NQ is detailed with rare major four-star support in the levels below.

– Price action in the S&P holding steadily above 4701-4705, previous resistance, now aligns with momentum indicator as our Pivot and point of balance.

– Higher price action overnight in the S&P struggled through the open last week, but stabilized to finish well.

– Week 3 option expiration in the rearview mirror, and no bats of true volatility given elevation. Remember 50 points in the S&P is now 1%! However, weakness now may find less footing from dealers defense.

– S&P currently playing out a rising triangle pattern (chart above), typically resolves higher and the direction of the underlying trend. However, rising triangles that drag out can become rising wedges. These have a higher probability of resulting in a reversal. Key takeaway; the sooner the resolution, the more likely it is a bullish one…. Click here to get our (FULL) daily reports emailed to you!

Crude Oil (January)

Yesterday’s close: Settled at 75.94, down 2.47 on Friday and 3.75 on the week

– China alluding to liquidity support helped underpin and overnight rally from rare major four-star support but stalled at first key resistance at 76.67-76.98 perfectly.

– Expect SPR discussion to evolve. We have said and maintain, we view extensive action as capitulatory, resulting in a more intermediate-term bullish rally. Remain cautious until such.

– Managed-Money net-longs down by 10% for week ending last Tuesday. This is welcomed.

– Momentum indicator is our Pivot; continued action below Click here to get our (FULL) daily reports emailed to you!

Gold (December) / Silver (December)

Gold, yesterday’s close: Settled at 1851.6, down 9.8 on Friday and 16.9 on the week

Silver, yesterday’s close: Settled at 24.781, down 0.119 on Friday and 0.565 on the week

– Day in and day out, we have highlighted how well Gold and Silver have held ground despite U.S. Dollar strength (DX highest since July 2020) and a broadly lower Treasury complex (last week until the Friday rally). This supports a longer-term continuation of the newfound strength into Q1.

– Back and fill is important. How is it received?

– Gold Managed-Money Net longs, highest since April 2020, built out of Covid consolidation and into record summer rally. Silver, highest since June 2021 fallout.

– Comments from Vice-Chair Clarida on Friday, reevaluating pace of taper, hit Gold and Silver. Remember, very dovish November meeting, basically net-zero taper, was a bullish catalyst.

– China less hawkish, may dovish, supportive to Silver overnight.

– Silver bullish cup and handle developing out of inverse head and shoulders, holding neckline. Descending wedge handle can be very powerful.

– December option expiration today, can open up trading ranges.

– Major three-star support in Silver has been defended very well at 24.51-24.58.

– Extremely bullish upon close above major three-star resistance at… Click here to get our (FULL) daily reports emailed to you!

—

Originally Posted on November 22, 2021 – S&P and Silver, Resolutions Imminent

Charts Source: Trading View

Disclosure: Blue Line Futures

Futures trading involves substantial risk of loss and may not be suitable for all investors. Trading advice is based on information taken from trade and statistical services and other sources Blue Line Futures, LLC believes are reliable. We do not guarantee that such information is accurate or complete and it should not be relied upon as such. Trading advice reflects our good faith judgment at a specific time and is subject to change without notice. There is no guarantee that the advice we give will result in profitable trades. All trading decisions will be made by the account holder. Past performance is not necessarily indicative of future results. The information contained within is not to be construed as a recommendation of any investment product or service.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Blue Line Futures and is being posted with its permission. The views expressed in this material are solely those of the author and/or Blue Line Futures and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Options Trading

Options involve risk and are not suitable for all investors. Multiple leg strategies, including spreads, will incur multiple commission charges. For more information read the "Characteristics and Risks of Standardized Options" also known as the options disclosure document (ODD) or visit ibkr.com/occ

Disclosure: Futures Trading

Futures are not suitable for all investors. The amount you may lose may be greater than your initial investment. Before trading futures, please read the CFTC Risk Disclosure. A copy and additional information are available at ibkr.com.