Today we will be looking at the hijinks in VXX[i], and how it has become completely untethered from its benchmark, the CBOE Volatility Index (VIX).

Yesterday, VXX’s manager, Barclays, announced that it would be suspending the issuance of new notes in VXX and its cousin OIL[ii]. In a statement, the bank announced that it no longer had “sufficient issuance capacity to support further sales from inventory and any further issuances of the ETNs.” The bank was not forthcoming on other details, leading market pundits to speculate whether the bank had made this move because it had become too expensive to hedge profitably, hit a position limit at a futures exchange, or crossed an internal risk management threshold. All are plausible, but it is pointless to speculate why they undertook this measure when they did. We are more concerned with the ramifications for those who trade and invest in VXX.

It is important to remember the distinction between ETNs and ETFs. They tend to look and act alike under normal circumstances, but subtle differences have a nasty way of revealing themselves when markets misbehave. Unlike an ETF, which is essentially a pass-through structure, ETNs are liabilities of their issuers. Those issuers, usually banks, must manage their liabilities, giving them capacity constraints that ETFs, which hold assets in custody, do not. Many traders remember the demise of XIV, a Credit Suisse issued volatility-linked ETN, during the so-called “Volmageddon” of February 2018. While some may point to the current halt in RSX as a sign that ETFs are not immune, the cases are not truly analogous. There is no way to trade the underlying assets of RSX, the VanEck Russia ETF, so that impairment is exogenous. There is nothing inhibiting Barclays from trading the VIX contracts that underlie VXX. This halt is discretionary.

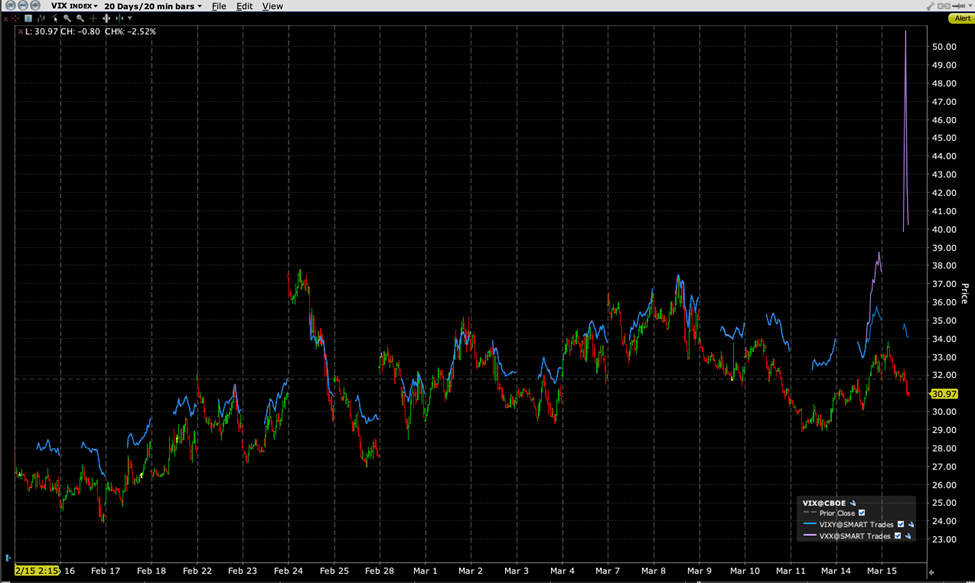

The differences between the freely convertible VIXY ETF and impaired VXX ETN are quite evident in the chart below. We see that both VIX-linked products tracked their benchmark quite nicely. In fact, VXX tracked so closely that I had to double-check the graph to see whether VXX was being properly displayed. For yesterday and today, I had no such problem, as VXX shot higher after being effectively untethered from its benchmark:

20-Day Intraday Chart of VIX (red/green), VIXY (blue), and VXX (purple)

Source: Interactive Brokers

The recent move higher may have been exacerbated by high short interest in VXX. Under normal circumstances it is difficult to have a short squeeze in an ETF because more shares can be created to fulfill the demand. That is not the case in VXX, at least not for the time being. As a result, we can get short squeezes and ensuing margin calls that push the ETN higher without regard to fundamentals.

While it may be tempting for some to try to ride the short squeeze from the long side, it is important to bear in mind that it is a risky proposition. Just last week we reminded readers that parabolic charts often resolve themselves by sharp drops without warning. If it can happen in a globally traded commodity like oil, it can certainly happen in a niche product like VXX. If you don’t remember the wild swings in TVIX last March[iii], they should prove an important reminder. At that time Credit Suisse temporarily halted issuance of that ETN amidst a short squeeze. The price surged, but then plunged once issuance resumed. Keep this chart in the back of your mind if you’re tempted to plunge into the VXX maelstrom:

TVIX Daily Chart, December 15th, 2020 to June 15th, 2020

Source: Bloomberg

[i] The full name for VXX is iPath Series B S&P 500 VIX Short-Term Futures ETN

[ii] The full name for OIL is iPath Pure Beta Crude Oil ETN

[iii] Now TVIXF, the VelocityShares Daily 2X VIX Short-Term ETN

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Margin Trading

Trading on margin is only for experienced investors with high risk tolerance. You may lose more than your initial investment. For additional information regarding margin loan rates, see ibkr.com/interest