(No musical link today despite the obvious reference. I’ve never liked the song)

I’ve been wrestling with what appears to be an obvious conundrum regarding the stock market’s mentality. Equity investors say that they are hopeful for a soft landing for the economy yet seem to relish signals of more overt weakness. Stock markets have rightfully shown that they crave monetary accommodation, so the prospect of rate cuts would of course be welcomed. But I have been wondering whether that desire for looser money reflects rational expectations or a more concerning addictive behavior. Have we become so obsessed with the outcome of lower rates that we lost sight about the circumstances that might bring them about?

As we write this, Fed Funds futures have completely priced out the idea of any more rate hikes. Considering the recent path of inflation and employment statistics, that certainly seems reasonable – even if a wide range of Federal Reserve speakers assiduously leave that possibility open. Remember, they remain publicly committed to both a 2% inflation target and a desire to tamp down, if not eliminate inflationary expectations beyond that target. Even though there is a high likelihood that inflation has become relatively tame, they can’t yet be fully certain that it will last. Thus, they need to keep their options open, even if the possibilities of further hikes are remote.

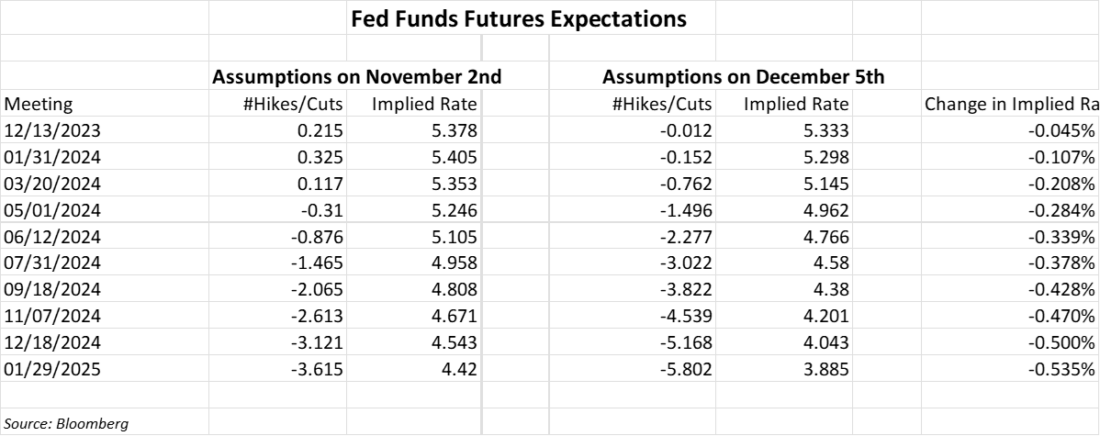

Yet the change in market expectations about future hikes since the last FOMC meeting is quite astounding, as shown in the table below. The changes are from the day after the last FOMC meeting to the present:

Among the notable changes are:

- Modest expectations (32.5%) for a 25 basis point hike by January have flipped to small expectations for a cut (15.2%)

- Cuts were not fully priced in until July. They are now expected by May, two meetings earlier.

- We’ve gone from an 11.7% expectation for a hike in March to a 76.2% probability of a cut by that meeting.

- The rate expectation for December has dropped by 50bp, from 4.543% to 4.043%. In other words, two additional cuts are now priced in for calendar year 2024.

In light of those data, consider what might be the rationale behind such a change in outlook. Hint – it’s not a robust economy. It’s probably not a soft landing either.

It simply does not seem reasonable to expect the Fed to cut rates aggressively unless economic conditions warrant such a move. As we noted last week:

My concern is that stock traders have become more enamored about the prospect of cuts without fully considering the “why.” If we do get a soft landing, why would the Fed be willing to cut as early as May? They would need to see sustained 2% inflation. Considering we’re not there yet, that seems premature. And it’s also not clear that the Fed will see the need to lower real interest rates pre-emptively if the economy is chugging along modestly. Remember, it’s the last few years that have been abnormal in that regard. The current rate is a bit high on a historical basis, but not out of line with what prevailed prior to the Global Financial Crisis. (see graph at bottom)

Finally, consider also that next year is an election year. The Fed is historically loath to change rates ahead of an election to avoid perceptions that they are picking sides. As we saw in 2020, it is unlikely that the Fed would refrain from activity if circumstances dictate. But it would also mean that any pre-emptive or discretionary changes would likely need to occur earlier in the year. Futures are currently pricing in at least one rate cut between July and November. Bottom line: if you’re buying bonds because you expect aggressive rate cuts in the coming months (and not simply chasing performance), then it is understandable why your base case scenario involves economic weakness. But if you’re buying stocks for that same reason – that cuts are coming – ask yourself whether you are implicitly anticipating a soft landing or something much worse.

Source: 10-Year Real Interest Rate (REAINTRATREARAT10Y) | FRED | St. Louis Fed (stlouisfed.org)

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.

Leave a Reply

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

One of these days we might mention the elephant in the room which is the housing market. S&P/ Case Shiller at 312.313 seriously? I’m not suggesting this will effect the short term equity bull run but I definitely not seeing a reversal in interest rates until the housing market has a well overdue correction.

i want a phone # have a ??

Hello, please view this link to connect with Client Services via phone:

https://www.interactivebrokers.com/en/support/customer-service.php?p=contact

We hope this helps.

Why is everybody discounting the possibility of a real soft-landing where inflation continues to crash under 2% but economy remains strong and the Fed cuts rates just so real rates aren’t out of whack?

Because the Fed historically has never engineered a soft-landing.

a soft landing is still a landing.

So is a landing on the ground if the chute opens or fails to open

I don’t understand how a rate cut could even be priced in when food inflation is still so high. Strip out oil and gas and inflation is still well above 2%