")

As inflation thrives like a genie released from its bottle, some analysts are questioning if the Federal Reserve’s (the Fed) monetary policy tightening is working. Data released today shows that the tightening appears to be making its way throughout the economy and dampening demand for consumer goods and services.

Today’s September retail sales report showed weakness with an unchanged reading on a month-over-month basis, much lower than market expectations of a 0.2% rise and lower than August’s 0.4% gain. These figures are not adjusted for inflation, meaning that consumers purchased less goods and services when adjusting for volumes since yesterday’s inflation data showed a 0.4% gain. The weakness was led by miscellaneous store retailers, gasoline stations, electronics & appliance stores and furniture & home furnishing stores showing declines of 2.5%, 1.4%, 0.8% and 0.7%. Sporting goods & bookstores and motor vehicle & parts dealers also contributed to the weakness. While most categories were weak, strength was seen in the control group, with general merchandise stores, health & personal care stores, e-commerce, and food at dining establishments and at supermarkets having gains of 0.7%, 0.5%, 0.5%, 0.5% and 0.4%.

Today’s preliminary consumer sentiment release for October was 59.8. While slightly better than market expectations of 59 and an improvement from September’s 58.6 level, it is still near record lows. Consumers expressed concerns regarding uncertainty about financial markets, inflation and the overall economy. Expectations for inflation one year from now rose to 5.1% from 4.8% in September while expectations for inflation five years from now rose to 2.9% from 2.8%. On a somewhat encouraging note, easing supply chain pressures contributed to an improvement in purchasing conditions for durable goods.

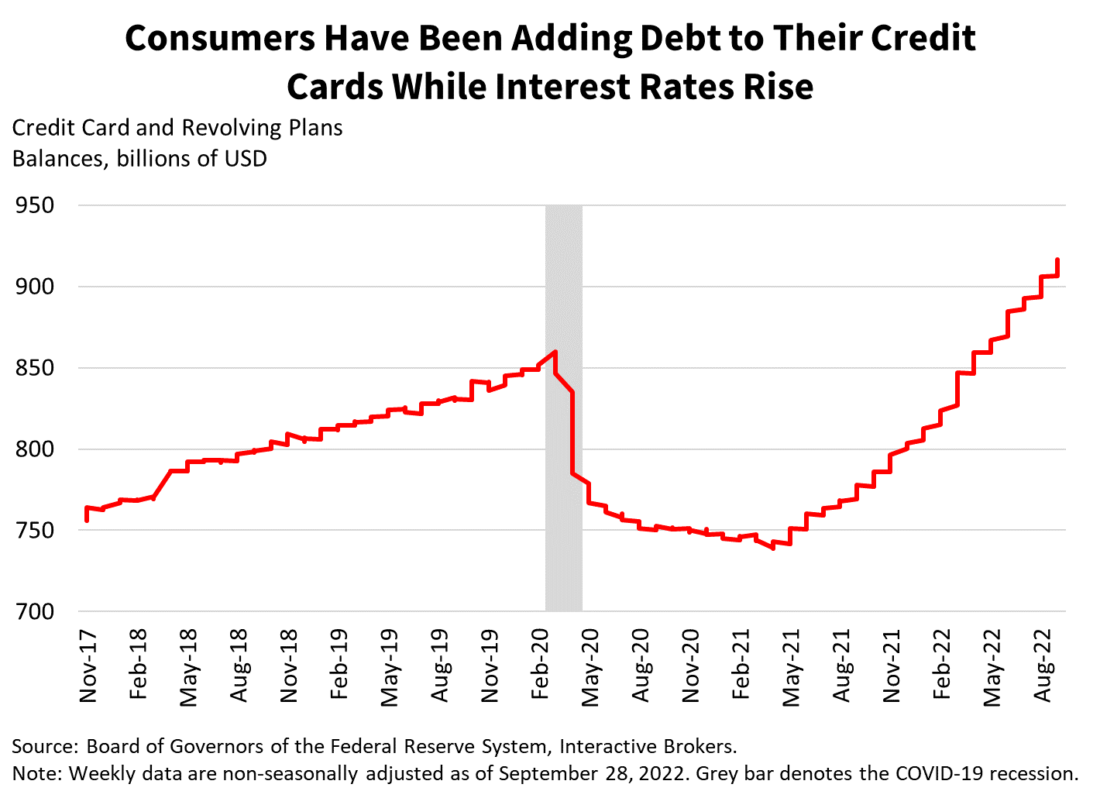

Higher interest rates and tighter financial conditions continue to point to weak consumption and sentiment overall, especially in the manufacturing and real estate categories. Record levels of credit card debt are also punishing consumers as higher interest rates kick in and increase the share of Americans’ budgets that are allocated toward interest expenses rather than necessities. The continued deceleration in the manufacturing PMI, durable goods orders, housing starts and home sales confirms the slowdown in the manufacturing and real estate sectors. As rate hikes and tighter financial conditions work their way through the economy, demand will continue to slow.

Yesterday’s CPI data was awful and many wondered if the Fed is tightening for no reason due to a lack of progress on the inflationary front. The challenge is that once the inflationary genie is out of the bottle, it requires a lot of effort and might to reverse the trend. Monetary policy tightening takes time to reach the broad economy and it typically hits leading indicators first, which are weakening and are emblematic of a tightening campaign that is truly working.

Markets declined after the retail sales and consumer sentiment reports were released, erasing morning gains after yesterday’s monster comeback. The S&P 500 Index is down roughly 1%, yields are up slightly across the curve and the dollar index (DXY) is up roughly 50 basis points. It is less than two dollars away from its 52-week high of $114.78. While yesterday’s report was disappointing on the inflation front, today’s reports are mixed. They show that demand and sentiment are weak, which is what the Fed wants and that’s great for taming inflation and rates, but adverse for corporate revenues and earnings.

Watch the Retail Sales Educational Video at Traders’ Academy – Click Here

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.