On Friday, after the blowout payrolls report, we noted that the stock market seemed to be ignoring the messages sent by the bond market. For the full message, I suggest reading the linked article, but the TLDR version is that renewed enthusiasm for rising stocks is allowing equity enthusiasts to ignore the eroding monetary conditions that had enabled huge rises in risk-asset valuations for the better part of a decade-plus.

It is one thing to observe a phenomenon, another to explain it. I’ve been wrestling with the proper hypothesis, and I kept coming back to two themes that should be painfully familiar to faithful readers: FOMO and nihilism.

FOMO, an acronym for “Fear of Missing Out”, has been a factor in rising markets more or less forever. No one likes to be left behind, and investors are especially averse to watching others make money while they sit on the sidelines. The fear is particularly acute for institutional investors, who find themselves with smaller asset pools, or even jobless, if they underperform for extended periods of time. A period of positive momentum brings out FOMO even in unenthusiastic investors.

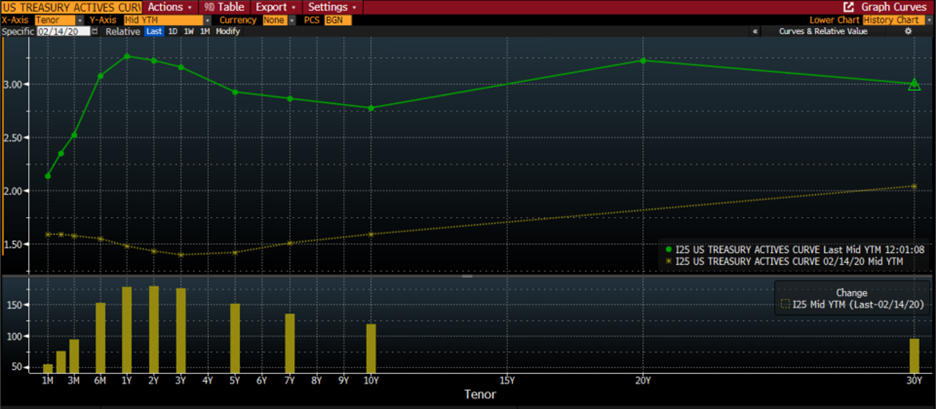

Nihilism, an extreme skepticism maintaining that nothing in the world has a real existence, is a much more pernicious term. We first unveiled it at an extraordinarily auspicious time. On February 14, 2020, we published “Confessions of a Market Nihilist”. We were wrestling with the stock market’s inability to pay attention to, let alone properly discount, the warning signals that were abounding throughout the economy. Stocks rose for another week, then fell by about 1/3 in the ensuing weeks. I re-read the piece this morning, and the following graph jumped out at me:

US Treasury Yield Curve, February 14th, 2020 (green) vs. One Month Prior (yellow)

Source: Interactive Brokers, via Bloomberg

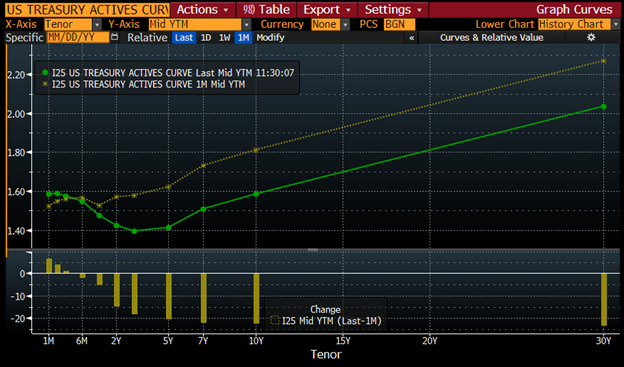

With perfect hindsight, the bond market got it right when stocks didn’t. There was a notable inversion in the 2-5 year segment of the yield curve – again in hindsight, not inverted enough – but stock traders carried on buying. When we look at the current yield curve we see an even deeper inversion, though in a different portion of the curve:

US Treasury Yield Curve, Today (green) vs. February 14th, 2020 (yellow)

Source: Bloomberg

Instead of the dip in the intermediate term, bonds are pricing in further rate hikes that eventually will need to be reversed in about two years. The amount of inversion in the 2-10 year portion of the curve is about 40 basis points, something we haven’t seen since the early 1980’s. Few of us were active in the markets at that time, but it was an ugly one for the economy and markets.

Last week we addressed the kookiness surrounding AMTD Digital (HKD), noting that while it was difficult to classify HKD as a new meme stock, it appeared to attract many of the participants in various meme stock rallies. While HKD appears to be coming back to earth somewhat, down about 20% to $570 as I write this, the traditional meme favorites are back in favor today. Both AMC and GameStop (GME) are both up over 10% this morning. Throw in bitcoin’s flirtation with the $24,000 level, and we can assert that speculation is back. It’s not back in full force, mind you, but back nonetheless.

The return of speculative names is what makes me consider whether it is FOMO or nihilism driving the recent action. For now, I’ll side with FOMO. There are sufficient contrary voices to make me think that we are not at full nihilism, just in a period where giddy performance chaser are in control of light summer volumes. But neither promises to be a lasting prospect.

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Bitcoin Futures

TRADING IN BITCOIN FUTURES IS ESPECIALLY RISKY AND IS ONLY FOR CLIENTS WITH A HIGH RISK TOLERANCE AND THE FINANCIAL ABILITY TO SUSTAIN LOSSES. More information about the risk of trading Bitcoin products can be found on the IBKR website. If you're new to bitcoin, or futures in general, see Introduction to Bitcoin Futures.