One of the questions I’m asked most often is why is the CBOE Volatility Index (VIX) so high or so low. And yes, the question is posed in both directions about equally. I assert that volatility, using VIX as a proxy, is neither too hot nor too cold. It is just about right.

The direction of the question is usually a “tell” for whether the inquirer is bullish or bearish about stocks. The bears think VIX is of course too low, and they wonder why traders aren’t paying more for protection. The opposite is the case for the bulls. Of course each side wants to find the flaw in the other side’s logic.

Yet VIX has settled into a 25-30 trading range for the past few weeks. Stable prices tend to reflect that a rough equilibrium between supply and demand has been achieved. That could certainly be the case for volatility protection right now.

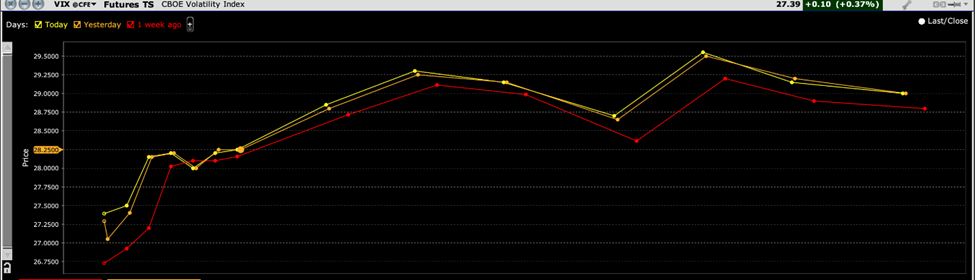

One technique that I use to gauge whether a given commodity is amply available or in shortage is the shape of the futures term structure. When looking at the graph from left to right, it is typical to see an upward slope, aka “contango”. That is the normal state of affairs for most commodities in a positive interest rate environment. A current snapshot of the VIX futures curve shows that we are in a modest contango from today through the October-November period that encompasses the midterm elections. It implies that there is an adequate supply of available volatility protection in the marketplace:

VIX Futures Term Structure

Source: Interactive Brokers

That we are not witnessing an obvious imbalance in the supply and demand for volatility protection should be sufficient justification for why VIX shouldn’t be higher than it is right now. Bear in mind that when VIX trends well above 30, we usually see backwardation in the futures. That has been the case during the volatility spikes that we saw earlier this year.

Those spikes and periods of backwardation tend not to persist for long periods of time. For starters, it can be expensive to own volatility through options. Options decay, and options with higher implied volatilities tend to decay faster. That mitigates against the likelihood that VIX can remain elevated for extended periods of time. It is simply cheaper in the long run for portfolio managers who wish to mitigate their risk to raise cash or move into lower beta stocks rather than constantly paying for expensive insurance.

As for why VIX isn’t lower, I would assert that the levels of volatility that persist in the market are justifying VIX around current levels. The nature of the VIX calculation doesn’t offer a simple route to compare its implied volatility assumptions with historical volatility, but the current VIX trading range offers a rough estimate that traders are expecting about 1.25%-1.5% daily intraday moves on the S&P 500 (SPX). That seems to be a fair assumption, given the moves that we have been experience and are likely to see in the coming weeks. Combine that with the known tendency for options to trade somewhat above historical volatility – that’s one of the ways that market makers compensate themselves for bearing the risks of selling options – and we end up with VIX at roughly current levels.

Traders need to respect the messages sent by the markets. The message that is being sent by VIX is that the 25-30 trading range seems about correct under current market conditions. The implication would be that traders should consider buying volatility if VIX is at 25 or less and take profits if it gets to 28 or so. Shorting above 30 can be much riskier because of the tendency of VIX to spike far higher if conditions get rocky. Under those circumstances, calendar spreads that involve selling high priced near term volatility and hedging with cheaper volatility in longer expirations can mitigate risk if we see backwardation. This scenario should persist as long as we continue to experience the levels of market volatility and central bank uncertainty that have been persisting for the previous weeks and months.

As always, if circumstances change, so must your outlook and strategies. For now, with circumstances as they are VIX is more or less “just right.”

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.

Disclosure: Options Trading

Options involve risk and are not suitable for all investors. Multiple leg strategies, including spreads, will incur multiple commission charges. For more information read the "Characteristics and Risks of Standardized Options" also known as the options disclosure document (ODD) or visit ibkr.com/occ