For many years, UPS (UPS) had a memorable slogan: “We run the tightest ship in the shipping business.” It is catchy, yet idiomatic. The phrase refers to a detail-oriented management style applied to complex logistics, and was effective even for a company that its customers associate with brown trucks, not oceangoing vessels. That said, before goods can be loaded onto those ubiquitous trucks, UPS and its competitors rely on a variety of modes of transportation to get the goods from a wide range of locales. Last week, my wife and I rented a vacation house with a couple of friends who are in the business of moving freight around the world. My week was quite relaxing, thank you. Theirs was decidedly not.

For some perspective, the husband deals primarily in air freight and the “last mile”. Companies that ship via air are either behind schedule or moving something that is perishable, like medicine. The wife tends to utilize sea and ground transportation to move items that are bulkier and less time critical than her husband’s. Between the two friends, both of whom have decades of experience in logistics, I received a crash course in logistics and the multitude of factors that are impeding the smooth flow of goods throughout the world.

Although I did my best to take a week off of obsessing about markets and the economy, I felt the need to tweet about the events that were causing my friends so much angst. I’ll recap them here:

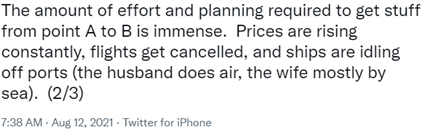

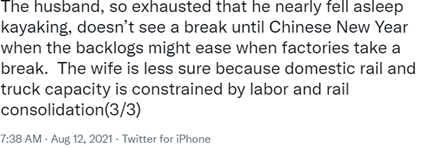

Find tweets here:

- https://twitter.com/SteveSosnick/status/1425783626499829772?s=20

- https://twitter.com/SteveSosnick/status/1425783627850391556?s=20

- https://twitter.com/SteveSosnick/status/1425783628907393027?s=20

- https://twitter.com/SteveSosnick/status/1425787580931526665?s=20

Globalization and “just-in-time” manufacturing have brought many benefits to the economy. There are efficiencies to utilizing relative advantages found in a variety of locations that can outweigh the costs and difficulties of shipping goods from place to place. As consumers, we have benefitted from items produced in inexpensive locales by manufacturers utilizing cheaper raw materials and labor.[i] Yet a globalized economy requires a smooth flow of goods, often from one end of the earth to another. There are innumerable moving parts to that process (literally and figuratively), and when even one step in those complex processes goes awry, it causes great angst for those who are responsible for managing them.

According to my friends, there is plenty of blame to go around. The cost of shipping containers has been rising steadily. That creates a self-fulfilling feedback loop. Those who can afford to do so are absorbing capacity at nearly any price, making others panicky and willing to pay ever higher prices. Covid has created port delays, most recently in China at the port of Ningbo and Nanjiang airport. These are on top of bottlenecks that exist at ports. Ships are idling off the port of Long Beach, California, with my friend attributing delays to both capacity at the docks and a shortage of truckers willing and able to move the containers once they are offloaded.

It is quite obvious that the companies that are affected by higher shipping costs will do their best to pass them along to consumers. Some will be able to do so, causing inflationary pressures, others will not, impacting margins. That is a key question for investors, who will need to assess which companies will have earnings shortfalls because of tighter margins. The key question for the Federal Reserve is whether they believe that the higher cost of transit is indeed transitory. If this is indeed the result of a global economy awakening from a Covid-induced stupor and a US economy juiced by recent fiscal stimulus, one could credibly claim that we are seeing a situation that could resolve itself naturally – perhaps by next spring after the Chinese New Year, as my friend theorized.

Unfortunately for investors, we need to concern ourselves not only with the problem of higher shipping costs themselves, but more importantly how the Fed perceives them. It is a second-order problem, like all the questions that involve not only the economy itself but how they could affect monetary policy. Like it or not, that is what floats the market’s boat.

—

[i] Indeed, there are many hidden costs to globalization, including jobs lost to unfair trade and labor practices and the climate effects of sourcing goods globally rather than locally. I recognize them, but fully addressing them is beyond the scope of this piece.

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.