Labor conditions remained strong in October as robust demand for workers persisted while labor force participation slipped. Despite isolated pockets of weakness, overall labor data indicates businesses are still facing considerable staffing challenges.

The economy added 261,000 jobs for the month, exceeding the 200,000 consensus expectation but trailing the 315,000 notched in September, according to today’s Labor Department job data release. Average hourly earnings for private sector employees grew 0.4%, higher than the expected increase of 0.3%, which would have been the same as August. The labor force participation rate, or the portion of individuals that are either working or seeking work, declined for the second consecutive month and hit 62.2, a 10-basis point month-over-month drop and 1.2 percentage points below the February 2020 pre-pandemic level.

The data underscores that the tight labor market is contributing to increased wage pressure and sticky inflation in services while the weakness in labor force participation is also concerning. The weak labor force participation has prevented businesses from increasing productivity, which in combination with higher wages is squeezing margins. From a longer-term perspective, this could create challenges for equity investors. While market valuations have declined year to date, earnings forecast revisions, in my view, have not been lowered sufficiently to reflect likely economic deceleration, inflation, wage pressures and the lack of productivity gains.

Mixed market reactions to the employment data are occurring today. Major equity indices climbed roughly 2% following the data release, the dollar index declined close to 2%, crude oil gained 5% and yields advanced across the curve initially with short-duration debt reaching new highs against the backdrop of expectations shifting toward a marginally tighter Federal Reserve bank. Yields have since retreated and are now down on the day.

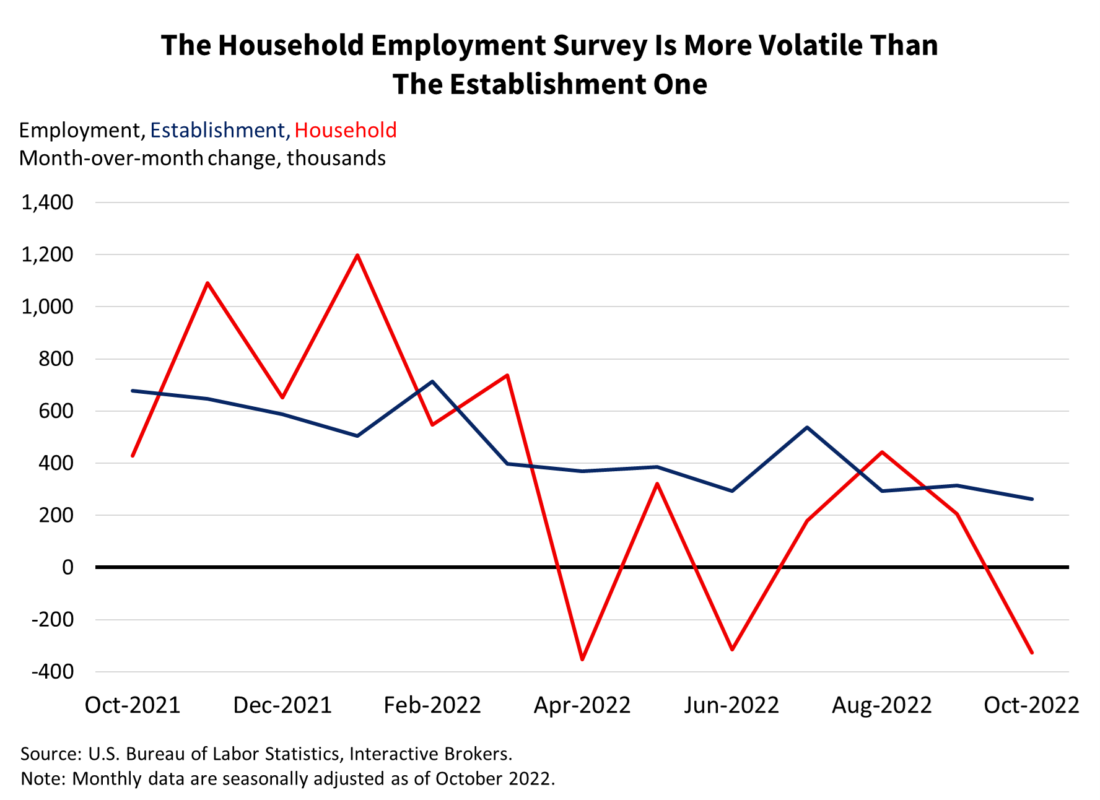

Despite the strong headline job data numbers, pockets of weakness emerged in the report. The unemployment rate rose from 3.5% in September to 3.7%, which was higher than the expected 3.6% rate. Rising unemployment was driven by an employment decline in the household employment survey. But wait, didn’t we just say that we added around a quarter of a million jobs? Yes, and the discrepancy results from the Labor Department using two different surveys: the establishment survey, which is based on company payrolls, and the household survey, which is based on households answering survey questions. The household survey reflects a loss of 328,000 jobs, the first loss since June and therefore pushes up the unemployment rate. The household survey, however, is more volatile than the establishment survey and should carry less significance when assessing the economy.

October’s job gains were led by the education and health services, professional business services, leisure and hospitality, manufacturing and government sectors, with each adding 79,000, 39,000, 35,000, 32,000 and 28,000 jobs, respectively. Gains were broad based, with almost all other sectors contributing to gains albeit more modestly. The mining and logging category was the exception as employment was unchanged during the period.

Overall, the economy continues to add jobs and that’s positive for economic growth and financial markets; however, cracks are surfacing. Just this week, several more large corporations announced hiring freezes and layoffs, adding to the long list. On the other hand, releases from the Labor Department on Tuesday and Thursday regarding job openings and unemployment claims reflect a labor market with many job opportunities and a low level of layoffs. Conditions remain strong overall, but not as strong as they were in the beginning of the year. The one problem, however, is that this report doesn’t solve the global economy’s biggest problem—Inflation.

Meanwhile, north of the border in Canada, the employment gain was 108,100 in October, higher than the 21,000 jobs gained in September and blowing away expectations of 10,000. The unemployment rate remained unchanged at 5.2%, better than the expectations for a rise to 5.3%.

—

Want to learn more about what goes into the Payroll Employment report? Watch here at Traders’ Academy

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.