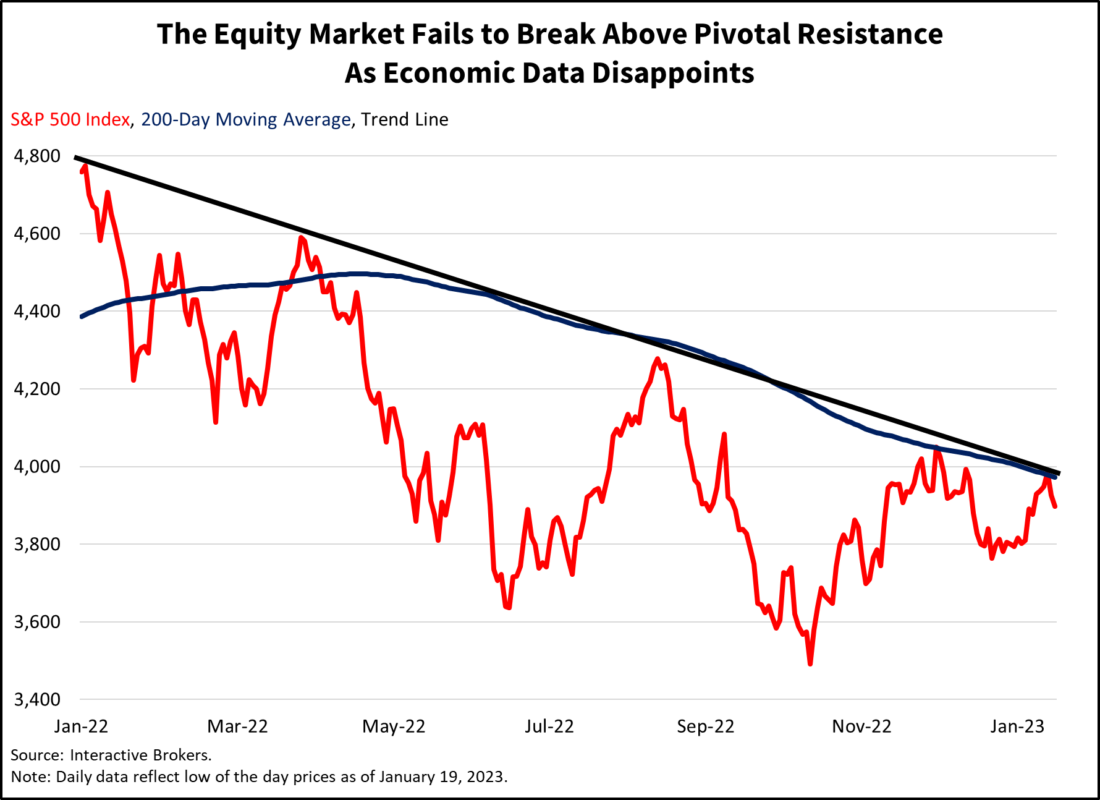

This morning’s data showing growing weakness in real estate alongside lackluster earnings reports drove an early morning equity selloff following yesterday’s 1.6% decline in the S&P 500. A dreadful one-two punch of contracting retail sales released yesterday and this morning’s news of a 1.6% month-over-month decline in housing permits has taken center stage among investors, who appear to be neglecting this morning’s positive news regarding the labor market. Investors are bracing for a potential recession this year while risks concerning the U.S. debt limit are adding to already strong headwinds. The continued market selloff occurs after yesterday’s failed morning rally, occurring right near the pivotal 200-day moving average and 12-and-a-half-month downtrend line that we’ve covered closely in our commentaries.

Markets are continuing their downtrend with the S&P 500 down 0.8% in early trading, with yields up roughly 2 to 5 basis points across the duration curve. Crude oil is up 0.7% while the dollar is roughly unchanged. Earnings season has failed to propel the market higher so far after an impressive start to 2023 for equities. Is it a new year, new story, or a new year, last year’s story? I suspect the latter case as expressed in 2023’s economic outlook, with 2022’s Federal Reserve (the Fed) rate hikes being felt in 2023, additional rate hikes this year, the Fed’s significant balance sheet reduction of roughly 1.6 trillion dollars since last April’s peak, persistent inflation and global instability.

Building permits continued their decline in December, as homebuilders are increasingly apprehensive about adding housing supply in a market hampered by two years of heavy construction activity post COVID-19, weak affordability, high interest rates, higher credit standards, labor shortages, etc. Permits fell 1.6% from the previous month, the fourth consecutive month of declines, further denting momentum despite yesterday’s modest increase in homebuilder sentiment, the first increase in 13 months. The expectation of a 1.4% increase in building permits due to recent, but modest, declines in mortgage rates failed to materialize. Starts and completions also contracted 1.4% and 8.4%, despite expectations for an increase.

Yesterday’s drop in industrial production also propelled recession fears, with the headline dropping 0.7%, shattering expectations of a 0.1% modest decline. The headline was the sharpest contraction since September 2021. Taken together, weakness in real estate and manufacturing is significant as combined they make up 30% of the economy. This morning’s initial unemployment claims report, on the other hand, showed surprising strength, dropping to 190,000 on the week. This number was substantially better than expectations of 214,000 and consistent with our prediction that the 2023 recession won’t be characterized by significant unemployment, but rather by the sting of inflation, margin compression, earnings contractions, and a slowdown in investment spending.

This morning’s data illustrates that the increasingly darkening cloud of weakening economic data has a silver lining—a persistently strong labor market.

This morning’s data illustrates that the increasingly darkening cloud of weakening economic data has a silver lining—a persistently strong labor market. While each week seems to bring new news of high-profile tech layoffs, such as Microsoft disclosing that it’s slashing 10,000 positions, unemployment claims show that it’s a job seekers’ labor market. Many employers are hesitant to lay off workers due to a tight labor market, low labor participation and the nation having 1.8 job openings for every unemployed individual. The good news story for employees, however, comes with a painful sidebar—housing affordability is at historically low levels and inflation, while moderating, is still causing sticker shock at the cash register. As the Fed continues to tighten its monetary policy, it’s important to remember that accommodative liquidity conditions significantly propelled asset valuations and the roaring bull markets of the last 15 years or so. In other news associated with the end of the liquidity party, Party City declared bankruptcy yesterday.

—

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from IBKR Macroeconomics and is being posted with its permission. The views expressed in this material are solely those of the author and/or IBKR Macroeconomics and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.