By J.C. Parets & All Star Charts

Wednesday, 30th November, 2022

1/ SPY Reclaims its 200-day Moving Average

2/ An Economic Bellwether Coils

3/ The Uptrend Persists for Yields

4/ Dollar Weakness Broadens

Investopedia is partnering with All Star Charts on this newsletter, which both sells its research to investors, and may trade or hold positions in securities mentioned herein. The contents of this newsletter are for informational and educational purposes only, however, and do not constitute investing advice.

1/ SPY Reclaims its 200-day Moving Average

As the rally off the October lows extends, we’re focusing on several critical levels in the major indexes.

Among the levels we’re monitoring, the 200-day moving average (MA) for the S&P 500 is coming into play.

In August, this long-term average briefly acted as resistance before prices were rejected lower. Today, prices are reclaiming it for the first time since April.

This could be a logical level for overhead supply to enter in the short term, and a major development for the bulls if price can reclaim it.

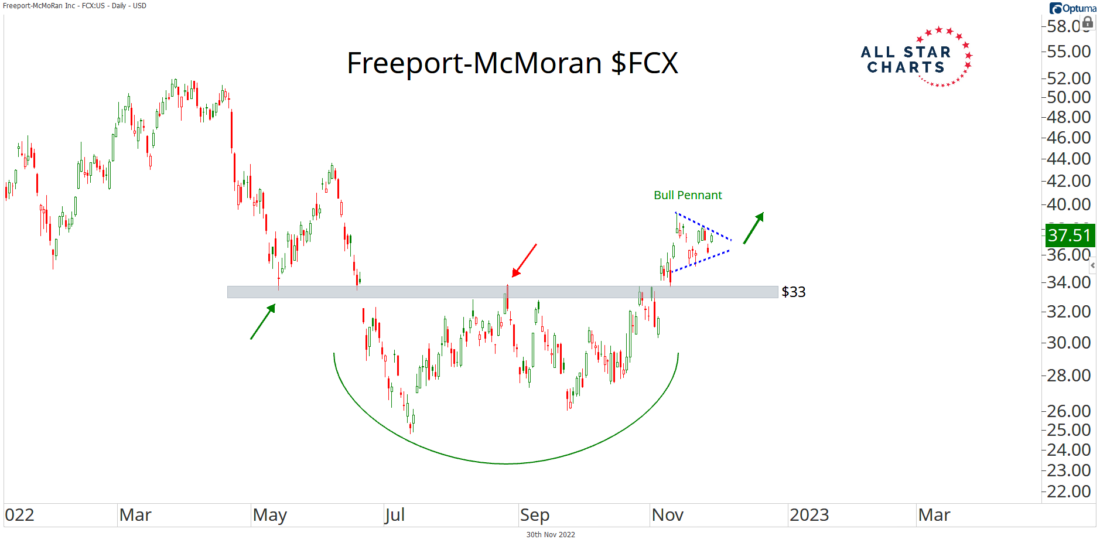

2/ An Economic Bellwether Coils

Last week, Freeport-McMoRan (FCX) joined our list of stocks above the August highs. It completed a bearish-to-bullish reversal, breaching the upper bounds of its range.

Fast-forward to today, and price has been coiling within a tight consolidation just above the breakout level.

Typically, these continuation patterns tend to resolve in the direction of the underlying trend. When they don’t, it could be a sign that the trend is running out of fuel, and due for a reversal.

An upside resolution from this economic bellwether could suggest an improving risk appetite for commodity-linked stocks and cyclical value sectors. It could also bode well for the broad market and support the recent price action.

On the other hand, a downside resolution could see FCX fall back into its prior range. Such a scenario could signal strong risk-off sentiment.

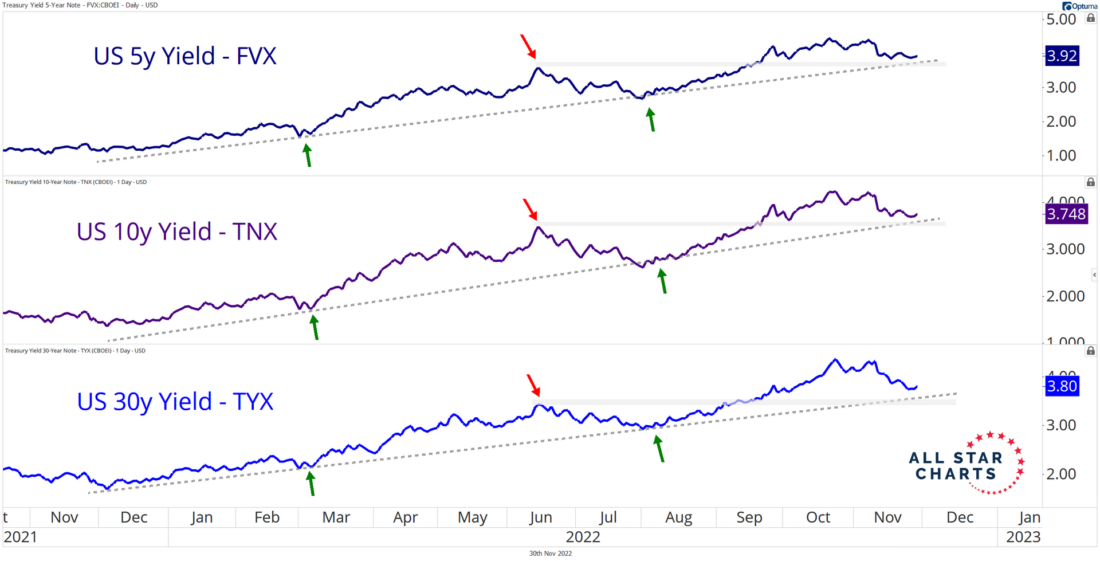

3/ The Uptrend Persists for Yields

The dollar and yields have dominated the conversation among investors this year, as their impacts have been felt throughout the market.

In recent weeks however, the U.S. Dollar Index (DXY) has broken its year-to-date trendline, raising the question of whether interest rates could follow suit.

So far, they haven’t, as the uptrend remains intact for the five-year, 10–year, and 30-year Treasury yields.

If and when rates do begin to roll over, we’re monitoring the June pivot highs for confirmation. A break below these former highs could indicate a relief in selling pressure for long-duration assets, including bonds and growth stocks.

4/ Dollar Weakness Broadens

Data continues to arrive suggesting the U.S. dollar may have found a short-term top.

Earlier this week, the USD/CNY currency pair undercut its former 2020 highs, printing a potential failed breakout.

The risk may be to the downside as long as USD/CNY holds below its former highs. A sustained move lower for this forex (FX) pair would add to the growing list of emerging market currencies strengthening against the dollar.

It’s no longer just the six components of the U.S. Dollar Index driving the decline in the dollar, as participation broadens among major global currencies.

—

Originally posted 30th November 2022

Disclosure: Investopedia

Investopedia.com: The comments, opinions and analyses expressed herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. While we believe the information provided herein is reliable, we do not warrant its accuracy or completeness. The views and strategies described on our content may not be suitable for all investors. Because market and economic conditions are subject to rapid change, all comments, opinions and analyses contained within our content are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy. This information is intended for US residents only.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from Investopedia and is being posted with its permission. The views expressed in this material are solely those of the author and/or Investopedia and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: ETFs

Any discussion or mention of an ETF is not to be construed as recommendation, promotion or solicitation. All investors should review and consider associated investment risks, charges and expenses of the investment company or fund prior to investing. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

Disclosure: Forex

There is a substantial risk of loss in foreign exchange trading. The settlement date of foreign exchange trades can vary due to time zone differences and bank holidays. When trading across foreign exchange markets, this may necessitate borrowing funds to settle foreign exchange trades. The interest rate on borrowed funds must be considered when computing the cost of trades across multiple markets.