Last week the Energy Information Administration (EIA) released their 2023 International Energy Outlook. It came out on Wednesday, the same day that Exxon Mobil (XOM) confirmed their acquisition of Pioneer Natural Resources (PXD), and they’re linked in more ways than simply their announcement date.

When energy companies issue long term energy forecasts they’re well aware that environmentalists will pore over them looking for an absence of fealty to the UN’s Zero By 50 goal – that is, that emissions of greenhouse gases will be eliminated by that date in order to limit anthropogenic global warming to 1.5 degrees C above the levels of 1850.

BP concluded that publishing data and forecasts was so fraught that they handed off their Statistical Review of World Energy after seven decades to the Energy Institute. But the EIA is unburdened by such concerns, and their latest publication should have agitated climate extremists more than XOM investing $60BN in adding oil and gas production.

The EIA produces several scenarios (“cases”) incorporating high versus low global GDP growth, oil prices and zero-carbon technology, along with a Reference Case which is based on current policies. They warn that they’re making projections not forecasts, although the difference is a subtlety only meaningful to the EIA.

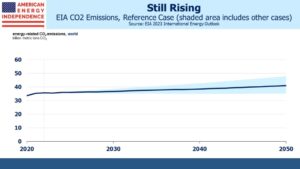

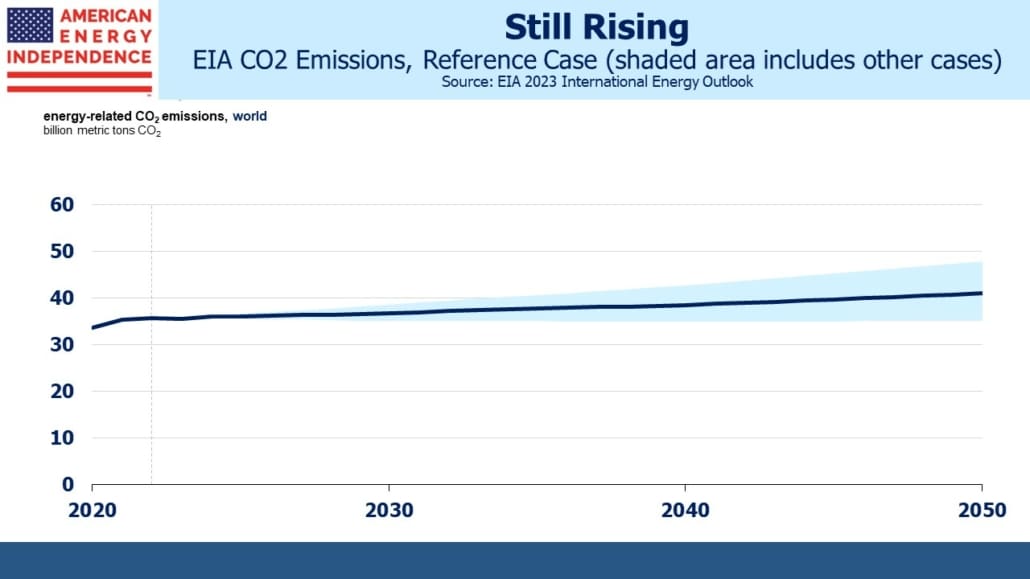

The headline could be, “EIA Forecasts Increase In CO2 Emissions By 2050” if their publications received such coverage. Higher living standards and population in developing countries will more than offset improving energy efficiency. When people have more disposable income, they use more energy. There is no historical precedent suggesting that can be avoided, so the EIA projects primary energy consumption will grow from 640 Quadrillion BTUs (Quads) to 856 Quads, a 1.1% annual growth rate.

The EIA includes some other dramatic changes

Their Reference Case assumes that non-fossil fuels will increase their share of primary energy and fulfill 58% of the increase in world energy consumption over that time. Increased global electricity consumption will be met primarily (italics added) by zero-carbon technologies. This is an extraordinary projection. Much of the rich world is dedicated to decarbonizing its power supply and electrifying more of its energy use – such as by shifting to Electric Vehicles (EVs) in the transportation sector. And yet, because of an increasing middle class in poorer regions such as Africa and much of Asia, electricity generation will consume more coal and gas than it does today. Perhaps most disappointingly, CO2 emissions from coal are projected to be the same in 2050 as today. The case for increased use of natural gas has never been stronger.

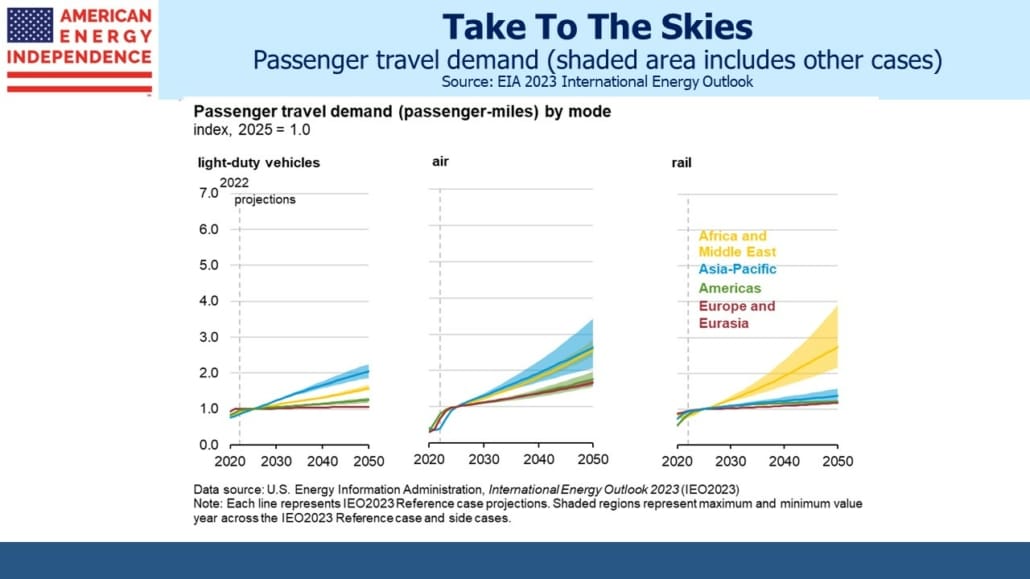

Aviation will more than triple.

The EIA sees EVs reaching 36% of new auto sales by 2050, which would still mean 1.4 billion internal combustion engine cars on the world’s roads. India’s energy consumption per capita will increase by 140%. China’s use of coal in iron and steel production will fall by 70%.

Other long-term forecasts typically see fossil fuel use declining over the next several decades. The International Energy Agency (IEA) in their Stated Policies Case (STEPS) expects fossil fuel consumption to peak within the decade, higher non-fossil fuel composition of primary energy and slower overall demand growth. They expect CO2 emissions to fall, but not by much.

Which brings us to XOM’s acquisition of PXD. Two years ago Engine No 1 criticized the company’s strategy, pushing it to be better prepared for the energy transition by focusing on short-cycle projects and renewables. Since then, XOM has committed $17BN to carbon capture and storage technology, biofuels and hydrogen. Nonetheless, a year ago critics such as Climate Action 100+ were complaining that 73% of their capital allocation was misaligned with the UN’s Zero By 50.

And now they’ve doubled down on the Permian basin in Texas. If production increases, Plains All American should be one of the beneficiaries. XOM also notes that they plan to accelerate PXD’s plans for zero-emission production from the wells they’re acquiring by fifteen years.

XOM’s long term outlook probably has much in common with the EIA.

The IEA’s scenario for reaching the UN’s target sees declining overall energy consumption. That only seems possible with extended slow growth in GDP and/or population.

The increase in M&A activity in the sector shows that boards are becoming comfortable making new long-term commitments to traditional energy. Oneok’s recent acquisition of Magellan Midstream, and Energy Transfer’s pending buy of Crestwood, are two more examples. They’re reaching the same conclusion as the EIA, which is that the world is going to need more of every kind of energy. America is well positioned to be part of the solution, especially with cheap natural gas.

—

Originally Posted October 15, 2023 – Exxon Buys More Of What The World Wants

Important Disclosures

The information provided is for informational purposes only and investors should determine for themselves whether a particular service, security or product is suitable for their investment needs. The information contained herein is not complete, may not be current, is subject to change, and is subject to, and qualified in its entirety by, the more complete disclosures, risk factors and other terms that are contained in the disclosure, prospectus, and offering. Certain information herein has been obtained from third party sources and, although believed to be reliable, has not been independently verified and its accuracy or completeness cannot be guaranteed. No representation is made with respect to the accuracy, completeness or timeliness of this information. Nothing provided on this site constitutes tax advice. Individuals should seek the advice of their own tax advisor for specific information regarding tax consequences of investments. Investments in securities entail risk and are not suitable for all investors. This site is not a recommendation nor an offer to sell (or solicitation of an offer to buy) securities in the United States or in any other jurisdiction.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and do not reflect the deduction of the advisor’s fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase. Indexes and benchmarks may not directly correlate or only partially relate to portfolios managed by SL Advisors as they have different underlying investments and may use different strategies or have different objectives than portfolios managed by SL Advisors (e.g. The Alerian index is a group MLP securities in the oil and gas industries. Portfolios may not include the same investments that are included in the Alerian Index. The S & P Index does not directly relate to investment strategies managed by SL Advisers.)

This site may contain forward-looking statements relating to the objectives, opportunities, and the future performance of the U.S. market generally. Forward-looking statements may be identified by the use of such words as; “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential” and other similar terms. Examples of forward-looking statements include, but are not limited to, estimates with respect to financial condition, results of operations, and success or lack of success of any particular investment strategy. All are subject to various factors, including, but not limited to general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors affecting a portfolio’s operations that could cause actual results to differ materially from projected results. Such statements are forward-looking in nature and involves a number of known and unknown risks, uncertainties and other factors, and accordingly, actual results may differ materially from those reflected or contemplated in such forward-looking statements. Prospective investors are cautioned not to place undue reliance on any forward-looking statements or examples. None of SL Advisors LLC or any of its affiliates or principals nor any other individual or entity assumes any obligation to update any forward-looking statements as a result of new information, subsequent events or any other circumstances. All statements made herein speak only as of the date that they were made. r

Certain hyperlinks or referenced websites on the Site, if any, are for your convenience and forward you to third parties’ websites, which generally are recognized by their top level domain name. Any descriptions of, references to, or links to other products, publications or services does not constitute an endorsement, authorization, sponsorship by or affiliation with SL Advisors LLC with respect to any linked site or its sponsor, unless expressly stated by SL Advisors LLC. Any such information, products or sites have not necessarily been reviewed by SL Advisors LLC and are provided or maintained by third parties over whom SL Advisors LLC exercise no control. SL Advisors LLC expressly disclaim any responsibility for the content, the accuracy of the information, and/or quality of products or services provided by or advertised on these third-party sites.

All investment strategies have the potential for profit or loss. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client’s investment portfolio.

Disclosure: SL Advisors

Please go to following link for important legal disclosures: http://sl-advisors.com/legal-disclosure

SL Advisors is invested in all the components of the American Energy Independence Index via the ETF that seeks to track its performance.

Disclosure: Interactive Brokers

Information posted on IBKR Campus that is provided by third-parties does NOT constitute a recommendation that you should contract for the services of that third party. Third-party participants who contribute to IBKR Campus are independent of Interactive Brokers and Interactive Brokers does not make any representations or warranties concerning the services offered, their past or future performance, or the accuracy of the information provided by the third party. Past performance is no guarantee of future results.

This material is from SL Advisors and is being posted with its permission. The views expressed in this material are solely those of the author and/or SL Advisors and Interactive Brokers is not endorsing or recommending any investment or trading discussed in the material. This material is not and should not be construed as an offer to buy or sell any security. It should not be construed as research or investment advice or a recommendation to buy, sell or hold any security or commodity. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

{kind=link}

{kind=link}

{kind=link}

Join The Conversation

If you have a general question, it may already be covered in our FAQs. If you have an account-specific question or concern, please reach out to Client Services.