There’s a 500-pound gorilla in the markets. Oddly, it’s the same person that I’ve frequently called Goldilocks over recent months.

The world’s central banks offered nearly constant monetary stimuli, which have been a key factor in the rising prices of risk assets over the past decade-plus. To a large extent, investors have become addicted to that liquidity. Now, with the Fed and many of its counterparts actively raising rates and reducing the size of their balance sheets, we now must contend with whether the Fed will withdraw liquidity without disrupting the monetary foundation upon which risk asset prices are based.

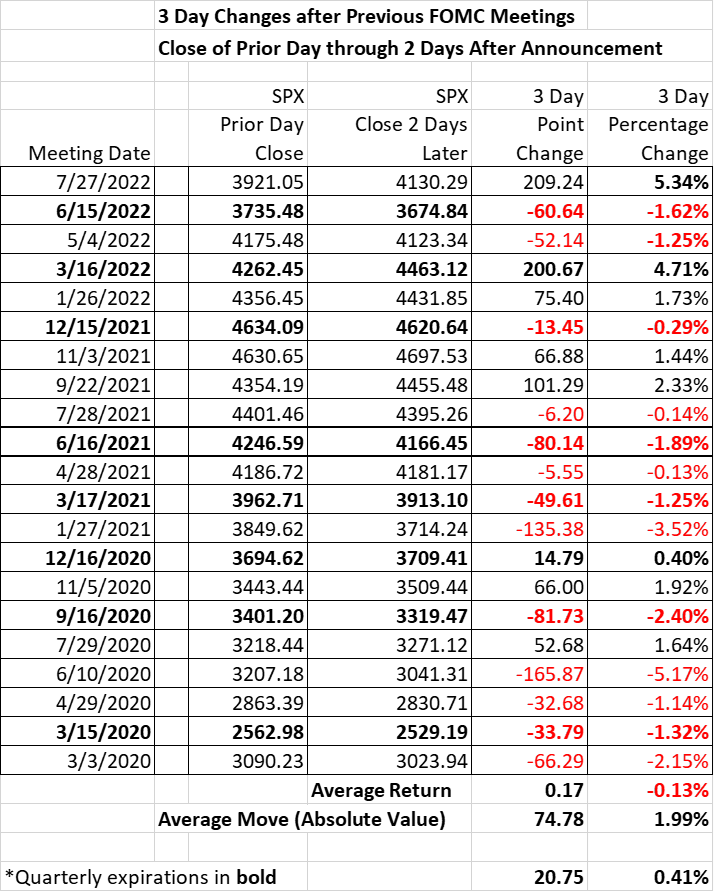

Equity investors loved Federal Reserve Chair Powell’s comments after the last FOMC meeting. The table at the bottom of this piece shows that the S&P 500 rose over 5% in the rest of the week after the meeting. In response to a question, he mentioned that the now-current 2.25-2.5% Fed Funds target was in the range of neutral. That was broadly taken as a sign that the Fed might pivot to lower rates more quickly than expected. We noted at the time that traders focused on the part of his answer that rates would be heading into restrictive territory, and asserted that the pushback from other Fed talking heads would swiftly push back on the neutral comment. That proved to be the case, but investors continued to focus on the potential for a rosy Fed course of action rather than a more realistic one.

At Jackson Hole, Mr. Powell went from Goldilocks to gorilla. He stated tersely and forcefully that the Fed’s goal was to bring inflation back to back to its 2% target level, even if that came at the expense of the broader economy. Equity markets hated hearing that, and were not thrilled when he broadly reiterated that message at a Cato Institute conference.

Thus we have the key question for the week ahead. Although Fed Funds futures are currently pricing in a 17% probability for a full 1% hike, the broad consensus is for a 75 basis point rise. In and of itself, an as-expected hike should be a mild positive, since it would remove the fears of a larger one. But the key will be Mr. Powell’s comments at the press conference. If he continues his recent strident tone, markets will be unimpressed, to say the least. If he reverts to his tendency towards a conciliatory tone, then we might see another enthusiastic period for both low-risk and high-risk assets alike, many of which are oversold. Gorilla or Goldilocks indeed.

- A note about the table that follows. We see that the market’s reaction to FOMC meetings was generally negative while the Fed pumping liquidity during the raging bull market of most of 2020-2021. When the Fed’s rhetoric switched to a more somber tone, we have seen more rallies than selloffs. It appears that traders expected too much from the Fed when they were giving out liquidity, and too little when they discussed withdrawing it.

Disclosure: Interactive Brokers

The analysis in this material is provided for information only and is not and should not be construed as an offer to sell or the solicitation of an offer to buy any security. To the extent that this material discusses general market activity, industry or sector trends or other broad-based economic or political conditions, it should not be construed as research or investment advice. To the extent that it includes references to specific securities, commodities, currencies, or other instruments, those references do not constitute a recommendation by IBKR to buy, sell or hold such investments. This material does not and is not intended to take into account the particular financial conditions, investment objectives or requirements of individual customers. Before acting on this material, you should consider whether it is suitable for your particular circumstances and, as necessary, seek professional advice.

The views and opinions expressed herein are those of the author and do not necessarily reflect the views of Interactive Brokers, its affiliates, or its employees.